LLY, ABT, CVS: Which Healthcare Stock Do Analysts Prefer?

The healthcare space is an intriguing place to be in these days, with incredible innovations such as GLP-1 drugs (weight-loss drugs like Ozempic and Wegovy) that are rich with growth potential. Additionally, the defensive traits of healthcare stocks make them terrific plays ahead of a potential bout of economic turbulence. Therefore, in this piece, we’ll check in with TipRanks’ Comparison Tool to see which of the following Strong-Buy-rated healthcare stocks analysts prefer for the coming year.

Eli Lilly (NYSE:LLY)

Eli Lilly is one of the best healthcare players in the market right now, with shares blasting off more than 87% in the past year alone. Over the past two years, shares have rocketed around 162%. That impressive performance was enough to cause Mad Money host Jim Cramer to consider the $612 billion healthcare behemoth as a potential member of the Magnificent Seven.

With hype building over the company’s skin in the GLP-1 drug game (with Mounjaro), it’s hard not to stay bullish on the stock as it looks to keep hitting new highs in 2024.

The last two years may have been remarkable for LLY shareholders. That said, zooming back to the past five years is when the returns get really impressive. Over the span, LLY stock has returned more than 433%. That’s impressive long-term momentum that seems to be showing no signs of slowing down.

Undoubtedly, Mounjaro and Zepbound have been the stars of the show for LLY lately. Moving ahead, we’ll get a gauge of just how powerful its weight-loss drugs are and how they stack up against competitors hungry to capture a potentially massive market. Add weight-loss drug insurance coverage into the equation, and Lilly’s offerings start looking more like a home run.

What Is the Price Target for LLY Stock?

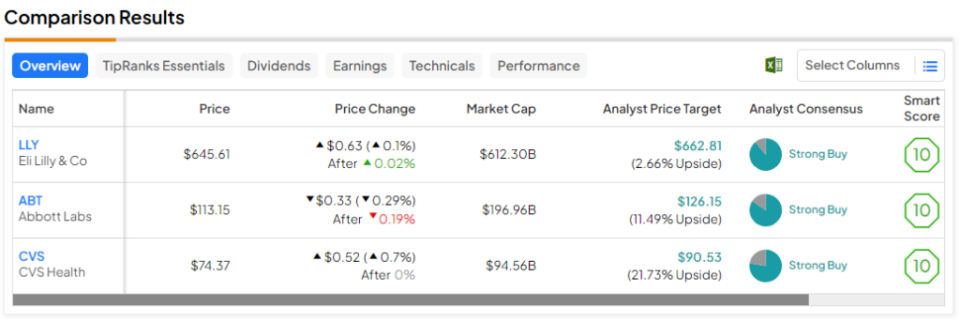

LLY stock is a Strong Buy, according to analysts, with 16 Buys and two Holds assigned in the past three months. The average LLY stock price target of $662.81 implies 2.7% upside potential.

Abbott Labs (NYSE:ABT)

Abbott Labs hasn’t been nearly as hot as Eli Lilly in recent years, with shares still attempting to stage a comeback after a brutal 2022 of losses. Down just 20% from its 2021 all-time highs, Abbott seems to have all the drivers in place to complete its comeback in 2024.

While the latest quarterly numbers (Q4) were pretty solid (with adjusted earnings per share (EPS) of $1.19, hitting the consensus spot-on), investors seemed discouraged by guidance (calling for 2024 adjusted EPS in the $4.50-4.70 range). Despite the light forecast, I remain bullish as its product pipeline looks to pay dividends in the new year.

CEO Robert Ford sounded really confident in the company’s “highly productive pipeline,” which he viewed as a source of “growth in 2024 and beyond.” Could it be that Wall Street is discounting the potential of Abbott’s pipeline?

Possibly. All the hype has surrounded the potential of GLP-1 drugs to disrupt the diabetes market. As a major vendor of diabetic devices (including FreeStyle Libre), Abbott stands out as one of the firms that could have something to lose as people shed pounds while under such drugs.

Even if GLP-1 acts as a potential medium-term headwind, I find it quite alarming that waist sizes may stand to rebound once one gets off the drugs. Until we learn more about the long-term effects of GLP-1 drugs, I wouldn’t count Abbott out of the game quite yet. I don’t think you can conclude that GLP-1 is the one magic shot to end diabetes as we know it. Wouldn’t that be nice, though?

What Is the Price Target for ABT Stock?

Abbott Labs stock is a Strong Buy, according to analysts, with 11 Buys and two Holds assigned in the past three months. The average ABT stock price target of $126.15 implies 11.5% upside potential.

CVS Health (NYSE:CVS)

Finally, we have drugstore and managed care provider play CVS, which may have put in a bottom in 2023. Though the stock remains down around 32% from its 2022 highs, I can’t help but be bullish due to its modest valuation (11.3 times trailing price-to-earnings versus the 18.5 times of the healthcare plan industry average) and plan to overcome last year’s headwinds.

Aetna, CVS’ health insurer, saw its medical benefits ratio (medical expenses over premiums) — a lower figure is better — on track to come in a tad worse than the original projection for 2023. Indeed, you can’t really blame Aetna for coming in short. The entire managed care scene has been under pressure, after all.

Over the medium term, GLP-1 drugs could have a positive effect as obesity rates fall in conjunction with health issues. In any case, it’ll be interesting to see how the drugs effect medical benefits ratios in the new year. Either way, Wall Street stands by CVS as one of the most intriguing value options in the healthcare space right now.

What Is the Price Target for CVS Stock?

CVS stock is a Strong Buy, according to analysts, with 14 Buys and four Holds assigned in the past three months. The average CVS stock price target of $90.53 implies 21.7% upside potential.

The Takeaway

Healthcare plays look very interesting as GLP-1 drugs look to impact almost every corner of the industry, from insurers to diabetes device makers to the firms that actually have their own offerings. Nonetheless, for the new year, analysts expect more upside from CVS stock (21.7%).