‘Load Up,’ Says Raymond James About These 2 ‘Strong Buy’ Stocks

In recent weeks, the market sentiment has undergone a noticeable shift. According to a recent survey conducted by the American Association of Individual Investors (AAII), bullish sentiment has reached ~45%, marking its highest level since November 2021.

That has been reflected in the market action, with more than 55% of stocks in the S&P 500 currently trading above their 50- and 200-day moving averages.

Larry Adam, the Chief Investment Officer of Raymond James, adds his perspective, stating, “Given the improving earnings outlook in the second half of 2023 and the economy defying recession expectations, it comes as no surprise that both the NASDAQ and S&P 500 have officially entered a new bull market.”

However, Adam advises investors not to get overly excited. “While history is on the market’s side – the S&P 500 historically rallies over 40% in the first year of a bull market and is up ~14% one year after the Fed ends its tightening cycle – the surge in bullish sentiment and ‘overbought’ conditions suggest caution may be warranted in the near term,” he went on to add.

Nevertheless, that doesn’t necessarily apply to all stocks. Raymond James analysts are still pointing out the names primed to push higher from here – they have identified two equities as Strong Buys in the current environment. We ran these tickers through the TipRanks platform to also see how they fare amongst other Wall Street stock experts. Let’s check the details.

Disc Medicine (IRON)

The first Raymond James-backed name we’ll look at is Disc Medicine, a biotech company focused on discovering and developing novel therapies for hematologic diseases. Disc Medicine is dedicated to addressing the significant unmet medical needs of patients with serious blood disorders by targeting the biology of the disc-shaped red blood cells.

The company’s strategic approach centers around targeting pathways that have a direct influence on the development of red blood cells, also known as erythropoiesis. The programs are specifically designed to regulate two essential processes crucial for the proper functioning of red blood cells: heme biosynthesis and iron metabolism. Through the manipulation of these fundamental components of erythropoiesis, Disc Medicine’s programs have the potential to tackle a broad spectrum of hematologic diseases.

Meanwhile, the company continues to make progress with its pipeline and provided an update earlier this month. Disc Medicine presented preliminary data from the ongoing Phase 2 open-label BEACON study, which evaluates bitopertin, an orally administered glycine transporter 1 (GlyT1) inhibitor indicated for the treatment of patients with erythropoietic protoporphyria (EPP) and X-linked protoporphyria (XLP). The data obtained thus far demonstrates consistent reductions in PPIX levels, notable improvements in reported tolerance to sunlight, and positive advancements in measures assessing the quality of life for patients.

The drug might need to still show it works on a bigger scale, but Raymond James analyst Danielle Brill thinks the results so far are very promising.

“While the dataset is small, we think it provides compelling evidence of bitopertin’s disease modifying potential in EPP,” she said. “Importantly, bitopertin demonstrated (1) dose dependent PPIX reductions (>30% in both doses), (2) significantly increased light tolerance vs baseline, and (3) clean safety, with no notable reductions observed in Hb levels vs baseline… In our view, the findings thus far check all the boxes, and provide solid proof-of-concept for bitopertin as a functional cure for EPP.”

“Given our conviction that the Ph 2 RCT dataset (expected early next year) will provide definitive evidence of biopertin’s disease modifying effects in EPP, we are changing our rating to Strong Buy,” Brill further added.

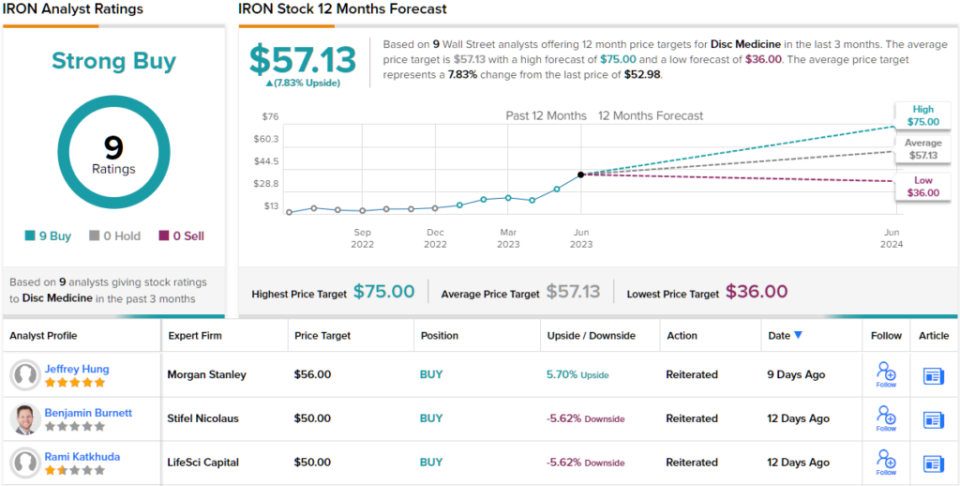

That is an upgrade from the prior Outperform (i.e. Buy) rating, and with the price target now at $75 (an increase from the prior $50), Brill sees the shares delivering returns of ~42% over the coming year. (To watch Brill’s track record, click here)

Brill’s take gets the full support of her colleagues. Based on Buys only – 9, in total – the stock claims a Strong Buy consensus rating. However, the shares have put in a big rally recently, and having soared by 166% year-to-date, the $57.13 average target makes room for further upside of just 8%. (See Disc Medicine stock forecast)

Dish Network (DISH)

Let’s now shift our focus to an entirely different industry for our next Raymond James pick. DISH Network is a major player in the field of digital television entertainment services. Based in Englewood, Colorado, this company occupies a prominent position as one of the largest providers of pay-TV in the United States, thanks to its direct-to-home (DTH) offering. Beyond its satellite provider Dish and streaming service Sling TV, DISH Network boasts substantial spectrum holdings and has actively been constructing a groundbreaking nationwide 5G network. Notably, it is the first-ever 5G Standalone (SA) network based on an open Radio Access Network (RAN).

Per a recent update, the 5G service is now available to more than 70% of the US’s population. That is a big milestone for the company, as it was required by the FCC to reach this target as part of the deal that allowed T-Mobile to purchase Sprint.

That said, it has not all been plain sailing recently. Dish’s recent Q1 performance left a lot to be desired. On the back of subscriber losses, revenue fell by 8.5% year-over-year to $3.96 billion, whilst also missing the consensus estimate by $100 million. Likewise at the other end of the scale, EPS dropped from $0.68 in the same period a year ago to $0.35, falling short of the $0.39 expected on the Street.

Despite the overall market performance being positive in 2023, DISH has experienced a significant decline of 53% since the turn of the year. As noted by Raymond James analyst Ric Prentiss, there are other issues the company must deal with. Nevertheless, the fact that it has achieved that aforementioned 5G milestone is a big deal and could lead to a shift in sentiment.

“Given the dramatic downturn in DISH’s debt and equity year-to-date, along with a significant increase in interest rates in 2022 and 2023, any financing will likely be very expensive for the company. But we feel that the achievement of the 70% deadline, along with a pause in the buildout capex and an expected significant stepdown in the transition services agreement (TSA) with T-Mobile, should meaningfully reduce the burn rate, improve the near-term cash flow profile and hopefully help lower the company’s cost of capital,” Prentiss noted.

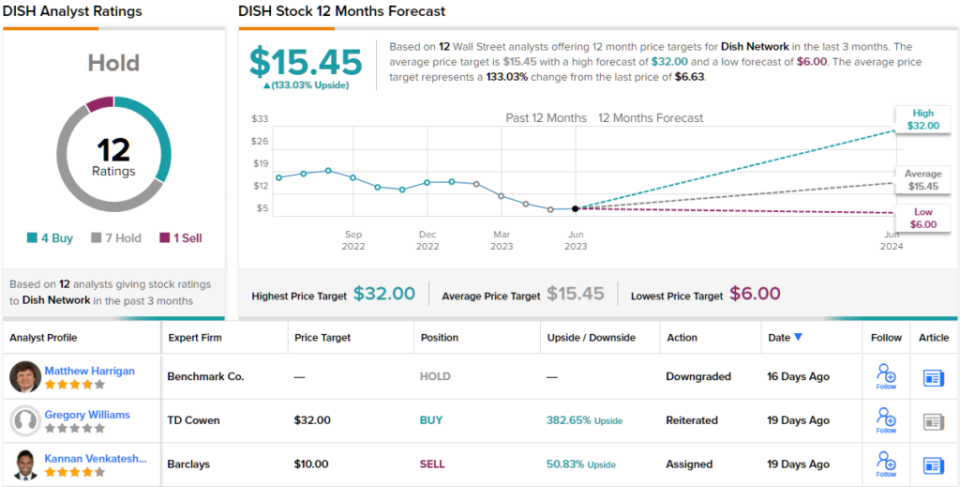

To this end, Prentiss rates DISH stock a Strong Buy, backed by a $21 price target. This implies shares will climb a whopping 217% over the coming months. (To watch Prentiss’s track record, click here)

Overall, the Street’s take shows conflicting signals. On the one hand, the stock only claims a Hold consensus rating, based on 7 Holds, 4 Buys and 1 Sell. That said, most seem to think the shares are significantly undervalued; at $15.45, the average target makes room for one-year returns of 133%. (See DISH stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.