Loan Growth Aids Bank of Hawaii (BOH) Despite Increasing Costs

Bank of Hawaii Corporation BOH enjoys solid loan and deposit balances, which, along with high rates, are expected to keep supporting financials. However, elevated expenses and challenges in improving fee income are major headwinds. Also, the company’s liquidity position is quite fragile.

The company’s deposit base saw a five-year (2018-2022) compound annual growth rate (CAGR) of 8.2%, while net loans and leases witnessed a CAGR of 6.9% during the same time frame. Strong deposit balances will also help the company generate higher loans and pursue other general business purposes.

With the Federal Reserve expected to keep interest rates high in the near term, Bank of Hawaii’s net interest income (NII) and net interest margin (NIM) are expected to be decent. With an asset-sensitive balance sheet and solid demand for both consumer and commercial loans, the bank’s NII is expected to increase, thereby driving top-line growth.

We remain encouraged by the Bank of Hawaii’s efforts to enhance shareholder value through its capital-deployment activities. In July 2021, the company hiked its quarterly dividend by 4.5% to 70 cents per share. It also has a share repurchase plan in place. The company's board of directors announced an additional share buyback authorization of $100 million. As of Jan 20, 2023, $135.9 million remained available under the program.

The company’s strong capital levels and income-generation capacity will enable it to continue capital deployment activities. Its debt/equity ratio compares favorably with that of the broader industry, reflecting that such activities are sustainable in the future.

However, mounting expenses are concerning. As the company continues to make investments in technology and innovation, its cost base is likely to be elevated. This will likely keep the bottom line under pressure in the near term.

Unimpressive fee income growth is a major headwind for Bank of Hawaii. Over the six years ended 2022, fee income decreased, seeing a CAGR of 3.2%. The company witnessed a declining trend in mortgage banking income, and a fluctuation in trust and assets management income in the past few quarters.

As of Dec 31, 2022, the company’s borrowings, consisting of securities sold under agreements to repurchase and other debt, aggregated to $1.14 billion, up sequentially. The company’s cash and due from banks was $316.7 million as of the same date. Amid a challenging operating backdrop and fears of a mild recession in the near term, the company's fragile liquidity position and high debt levels are concerning.

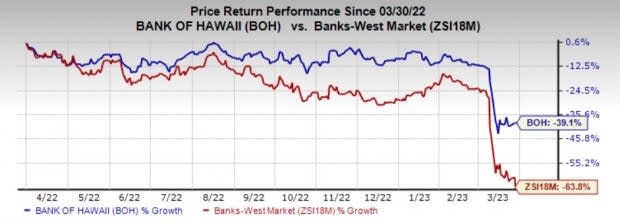

Shares of this Zacks Rank #3 (Hold) company have plunged 39.1% compared with a 63.8% decline recorded by the industry over the past year.

Image Source: Zacks Investment Research

Stocks Worth a Look

A couple of better-ranked stocks from the finance space are S&T Bancorp, Inc. STBA and Bank First National BFC. STBA currently sports a Zacks Rank #1 (Strong Buy) and BFC carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

S&T Bancorp’s 2023 earnings estimates have been revised 3.3% upward over the past 30 days. STBA’s shares have risen 9.5% over the past six months.

The consensus estimate for BFC’s 2023 earnings has been unchanged over the past month. Over the past six months, FULT’s share price has decreased 3.4%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bank of Hawaii Corporation (BOH) : Free Stock Analysis Report

S&T Bancorp, Inc. (STBA) : Free Stock Analysis Report

Bank First National Corporation (BFC) : Free Stock Analysis Report