Loan Growth & Cost Control Aid Navient (NAVI), High Debt Ails

Navient Corporation’s NAVI recurring revenue business model and focus on in-school originations will aid its top-line growth. Also, cost-control initiatives have been improving operational efficiency. However, limited servicing fee growth opportunities, unmanageable debt levels and unsustainable capital distributions are woes.

NAVI is aiming in-school originations to drive loan volumes in 2023. The company’s in-school origination channel was enhanced when Earnest acquired Going Merry, a financial aid platform in 2021. In 2017, NAVI had acquired Earnest, a financial technology and education-finance company serving consumers unable to get finance from traditional banks.

Navient believes loan growth and loan refinancing opportunities is likely to support its top line growth. It is an eminent portfolio holder of Private Education Loans and education loans insured or guaranteed under Federal Family Education Loan Program (FFELP).

High interest rates, several extensions of federal loan payment holiday, loan forgiveness proposals and programs are anticipated to create uncertainty and limit refinance loan origination volume in the near term. Nonetheless, in the long term, demand for refinancing loans should rebound once direct federal loan repayments begins.

Navient’s recurring revenue business model also boosts its top line. In fact, the company’s education loan portfolio generates significant cash flows. Projected cash flows from private education loans and FFELP loans are $6.7 billion and $6.6 billion, respectively, in the next 20 years.

Apart from concentrating on revenue growth, NAVI has been undertaking cost-control efforts to improve operating efficiency through data-driven approaches, simplification and automation. Over the years, the company has been witnessing a downtrend in expenses. The declining trend is likely to continue in the near term and aid NAVI’s bottom-line growth.

Navient’s business-risk reduction and simplification efforts bode well. Transferring all its Department of Education (ED) servicing contracts to Maximus in October 2021, it eliminated an operationally-risky business and amplified its focus on domains outside government student-loan servicing.

However, Navient’s top line is under pressure given its limited growth opportunities. After the transfer of ED servicing contract, it lost a major portion of its servicing revenues. Also, failure to acquire new loans, and develop and expand alternative sources to enhance declining revenues from FFELP loan portfolio are likely to affect its financials in the upcoming period.

As of Jun 30, NAVI’s long-term borrowings of $56.93 billion exceeded its cash and cash equivalents of $1.31 billion. Given such high debt burden, the company does not seem to be well positioned in terms of its liquidity profile. Also, an unfavorable debt/equity ratio compared with its industry’s average indicate that Navient’scapital distribution activities might not be sustainable in the long term.

Further, Navient is exposed to repricing risks related to its loans. Interest earned on FFELP loans are indexed to 1-month LIBOR rates and private education loans are indexed either to 1-month LIBOR rates or 1-month Prime rate. Cost of funds is primarily indexed to 3-month LIBOR rates. Relatively high interest rates are likely to lower Navient’s floor income, affect margins and reduce refinance loan origination volumes.

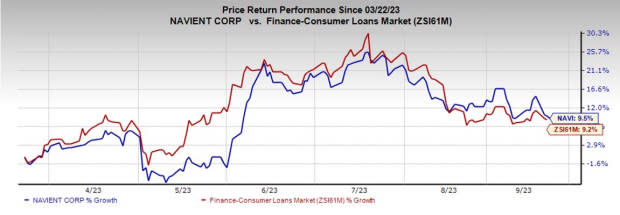

Shares of this Zacks Rank #3 (Hold) company have gained 9.5% compared with 9.2% growth of its industry over the past six months.

Image Source: Zacks Investment Research

Finance Stocks Worth Considering

A couple of top-ranked stocks from the finance space are BBVA USA Bancshares, Inc. BBVA and HSBC Holdings’ HSBC.

BBVA’s current-year earnings estimate has been revised 4.4% upward over the past 30 days. BBVA’s shares have improved 7.7% over the past three months. The stock currently sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for HSBC’s current-year earnings has been revised marginally upward over the past week. Over the past three months, HSBC’s share price has increased 1.1%. The stock currently flaunts a Zacks Rank of 1.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Banco Bilbao Viscaya Argentaria S.A. (BBVA) : Free Stock Analysis Report

HSBC Holdings plc (HSBC) : Free Stock Analysis Report

Navient Corporation (NAVI) : Free Stock Analysis Report