What Makes Steelcase Inc. (NYSE:SCS) A Great Dividend Stock?

Today we'll take a closer look at Steelcase Inc. (NYSE:SCS) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. If you are hoping to live on your dividends, it's important to be more stringent with your investments than the average punter. Regular readers know we like to apply the same approach to each dividend stock, and we hope you'll find our analysis useful.

In this case, Steelcase likely looks attractive to investors, given its 3.0% dividend yield and a payment history of over ten years. We'd guess that plenty of investors have purchased it for the income. Some simple research can reduce the risk of buying Steelcase for its dividend - read on to learn more.

Explore this interactive chart for our latest analysis on Steelcase!

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. In the last year, Steelcase paid out 44% of its profit as dividends. This is a medium payout level that leaves enough capital in the business to fund opportunities that might arise, while also rewarding shareholders. Besides, if reinvestment opportunities dry up, the company has room to increase the dividend.

In addition to comparing dividends against profits, we should inspect whether the company generated enough cash to pay its dividend. Of the free cash flow it generated last year, Steelcase paid out 29% as dividends, suggesting the dividend is affordable. It's positive to see that Steelcase's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

We update our data on Steelcase every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

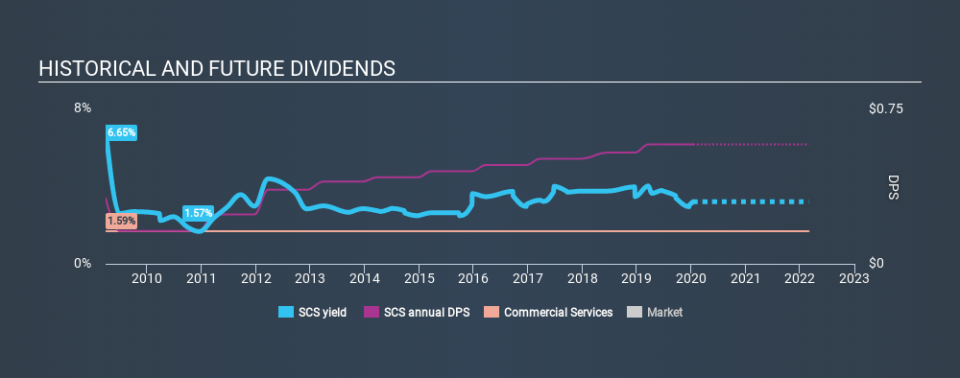

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. For the purpose of this article, we only scrutinise the last decade of Steelcase's dividend payments. The dividend has been cut on at least one occasion historically. During the past ten-year period, the first annual payment was US$0.32 in 2010, compared to US$0.58 last year. Dividends per share have grown at approximately 6.1% per year over this time. Steelcase's dividend payments have fluctuated, so it hasn't grown 6.1% every year, but the CAGR is a useful rule of thumb for approximating the historical growth.

It's good to see the dividend growing at a decent rate, but the dividend has been cut at least once in the past. Steelcase might have put its house in order since then, but we remain cautious.

Dividend Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. It's good to see Steelcase has been growing its earnings per share at 13% a year over the past five years. Earnings per share have been growing at a good rate, and the company is paying less than half its earnings as dividends. We generally think this is an attractive combination, as it permits further reinvestment in the business.

Conclusion

Dividend investors should always want to know if a) a company's dividends are affordable, b) if there is a track record of consistent payments, and c) if the dividend is capable of growing. It's great to see that Steelcase is paying out a low percentage of its earnings and cash flow. We were also glad to see it growing earnings, but it was concerning to see the dividend has been cut at least once in the past. Steelcase performs highly under this analysis, although it falls slightly short of our exacting standards. At the right valuation, it could be a solid dividend prospect.

See if management have their own wealth at stake, by checking insider shareholdings in Steelcase stock.

We have also put together a list of global stocks with a market capitalisation above $1bn and yielding more 3%.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.