The Market Doesn't Like What It Sees From Dragonfly Energy Holdings Corp.'s (NASDAQ:DFLI) Revenues Yet As Shares Tumble 60%

Unfortunately for some shareholders, the Dragonfly Energy Holdings Corp. (NASDAQ:DFLI) share price has dived 60% in the last thirty days, prolonging recent pain. For any long-term shareholders, the last month ends a year to forget by locking in a 93% share price decline.

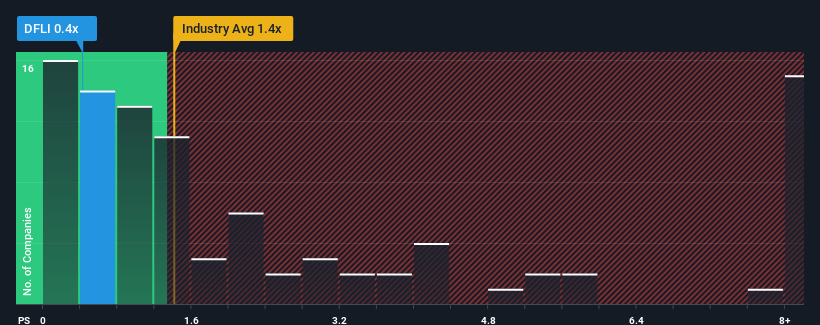

After such a large drop in price, Dragonfly Energy Holdings' price-to-sales (or "P/S") ratio of 0.4x might make it look like a buy right now compared to the Electrical industry in the United States, where around half of the companies have P/S ratios above 1.4x and even P/S above 4x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

View our latest analysis for Dragonfly Energy Holdings

What Does Dragonfly Energy Holdings' P/S Mean For Shareholders?

While the industry has experienced revenue growth lately, Dragonfly Energy Holdings' revenue has gone into reverse gear, which is not great. Perhaps the P/S remains low as investors think the prospects of strong revenue growth aren't on the horizon. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Want the full picture on analyst estimates for the company? Then our free report on Dragonfly Energy Holdings will help you uncover what's on the horizon.

What Are Revenue Growth Metrics Telling Us About The Low P/S?

In order to justify its P/S ratio, Dragonfly Energy Holdings would need to produce sluggish growth that's trailing the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 14%. Still, the latest three year period has seen an excellent 57% overall rise in revenue, in spite of its unsatisfying short-term performance. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Turning to the outlook, the next three years should generate growth of 32% per year as estimated by the four analysts watching the company. With the industry predicted to deliver 58% growth per annum, the company is positioned for a weaker revenue result.

In light of this, it's understandable that Dragonfly Energy Holdings' P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

Dragonfly Energy Holdings' P/S has taken a dip along with its share price. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Dragonfly Energy Holdings' analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. The company will need a change of fortune to justify the P/S rising higher in the future.

It is also worth noting that we have found 5 warning signs for Dragonfly Energy Holdings (1 is concerning!) that you need to take into consideration.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.