Match Group's (NASDAQ:MTCH) Q4 Earnings Results: Revenue In Line With Expectations But Quarterly Guidance Underwhelms

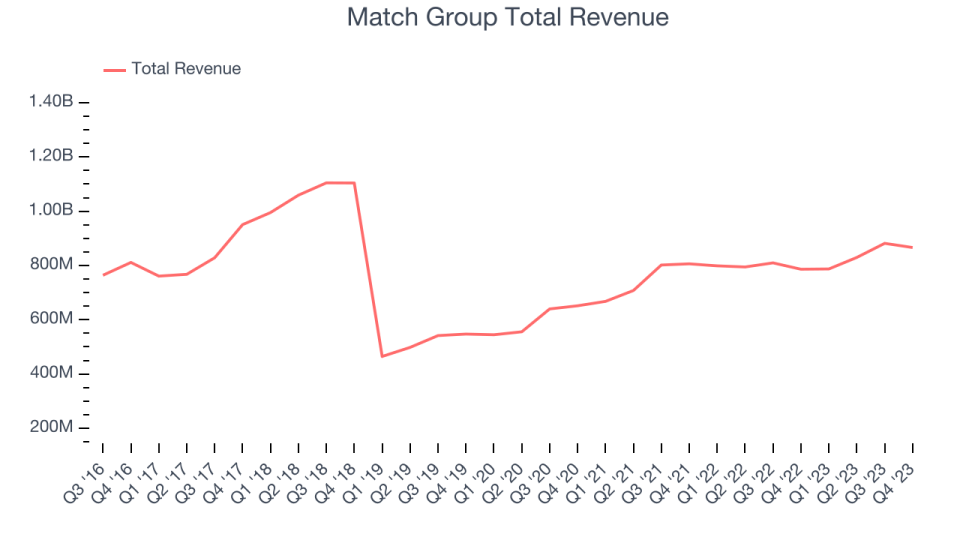

Dating app company Match (NASDAQ:MTCH) reported results in line with analysts' expectations in Q4 FY2023, with revenue up 10.2% year on year to $866.2 million. On the other hand, next quarter's revenue guidance of $855 million was less impressive, coming in 1.4% below analysts' estimates. It made a GAAP profit of $0.81 per share, improving from its profit of $0.29 per share in the same quarter last year.

Is now the time to buy Match Group? Find out by accessing our full research report, it's free.

Match Group (MTCH) Q4 FY2023 Highlights:

Market Capitalization: $10.43 billion

Revenue: $866.2 million vs analyst estimates of $861.3 million (small beat)

EPS: $0.81 vs analyst estimates of $0.49 (64.2% beat)

Revenue Guidance for Q1 2024 is $855 million at the midpoint, below analyst estimates of $867 million

Free Cash Flow of $258.7 million, similar to the previous quarter

Gross Margin (GAAP): 76%, up from 70% in the same quarter last year

Payers: 15.2 million, down 5% year on year

RPP: $18.67, up 17% year on year

Originally started as a dial-up service before widespread internet adoption, Match (NASDAQ:MTCH) was an early innovator in online dating and today has a portfolio of apps including Tinder, Hinge, Archer, and OkCupid.

Consumer Subscription

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

Sales Growth

Match Group's revenue growth over the last three years has been unremarkable, averaging 12.6% annually. This quarter, Match Group reported mediocre 10.2% year-on-year revenue growth, in line with what analysts were expecting.

Guidance for the next quarter indicates Match Group is expecting revenue to grow 8.6% year on year to $855 million, improving on the 1.4% year-on-year decline it recorded in the same quarter last year.

Our recent pick has been a big winner, and the stock is up more than 2,000% since the IPO a decade ago. If you didn’t buy then, you have another chance today. The business is much less risky now than it was in the years after going public. The company is a clear market leader in a huge, growing $200 billion market. Its $7 billion of revenue only scratches the surface. Its products are mission critical. Virtually no customers ever left the company. You can find it on our platform for free.

Usage Growth

As a subscription-based app, Match Group generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Over the last two years, Match Group's users, a key performance metric for the company, grew 4.9% annually to 15.2 million. This growth lags behind the hottest consumer internet apps.

Unfortunately, Match Group's users decreased by 900,000 in Q4, a 5.6% drop since last year.

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like Match Group because it measures how much the average user spends. ARPU is also a key indicator of how valuable its users are (and can be over time).

Match Group's ARPU growth has been mediocre over the last two years, averaging 3%. However, the company's ability to continue increasing prices while growing its users shows that users still find value in its platform. This quarter, ARPU grew 16.7% year on year to $56.99 per user.

Key Takeaways from Match Group's Q4 Results

It was great to see Match beat analysts' operating margin and EPS estimates. Although its user base fell (driven by softness at Tinder), its average price increase of 17% across its apps enabled the company to narrowly top expectations. Hinge was a bright spot this quarter as its revenue growth accelerated to 50%+, setting the stage for $1 billion of Hinge revenue in the coming years. On the other hand, its revenue guidance for next quarter missed Wall Street's estimates as it expects Tinder subscribers to decline. That anticipated drop, however, will be offset by continued price increases at Tinder, whose pricing is playing catching up with its peers (the app's services have been underpriced for years).

In terms of leadership changes, Match appointed Faye Iosotaluno as its Tinder CEO. Faye was the Group’s former Chief Strategy Officer and has spent the last 18 months as COO of Tinder. Bernard Kim, previously CEO of both Tinder and the parent entity, will remain closely involved as CEO of Match Group.

Lastly, with the stock trading cheaply, the Board authorized a new $1.0 billion share repurchase program. The company used more than half of its free cash flow to repurchase its shares in 2023 and has stated it intends to do the same in 2024 and possibly even more.

Overall, the results could have been better, but we remain constructive and will look for subscribers to stabilize in Q1 2024 when it will have easier base-year comps and lap its one-time, 60%+ price increases that happened at the start of 2023. The stock is flat after reporting and currently trades at $37.48 per share.

Match Group may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.