McKesson (MCK) Hits 52-Week High: What's Driving the Stock?

Shares of McKesson Corporation MCK scaled a new 52-week high of $485.22 on Jan 3, 2024, before closing the session slightly lower at $480.34.

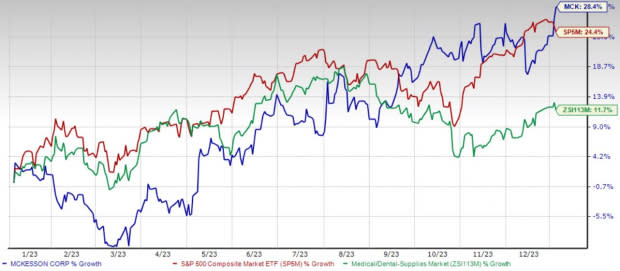

Over the past year, this Zacks Rank #3 (Hold) stock has gained 28.4% compared with 11.7% growth of the industry and a 24.4% rise of the S&P 500 Composite.

Over the past five years, the company registered earnings growth of 15.4% compared with the industry’s 9.1% rise. The company’s long-term expected growth rate of 10.5% compares with the industry’s growth projection of 11.9%. McKesson’s earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 8.9%.

McKesson is witnessing an upward trend in its stock price, prompted by its robust Biologics business. The optimism led by a solid second-quarter fiscal 2024 performance and its strategic deals are expected to contribute further. However, stiff competition and weaker generic pharmaceutical pricing trends persist.

Image Source: Zacks Investment Research

Let’s delve deeper.

Key Growth Drivers

Strength in Biologics: Investors are optimistic about McKesson’s robust Biologics business. Independent specialty pharmacy, Biologics by McKesson, has been making impressive progress lately. Last month, Novartis selected the pharmacy as a specialty pharmacy provider for FABHALTA (iptacopan).

The same month, the pharmacy was selected by SpringWorks Therapeutics as a limited distribution specialty pharmacy for OGSIVEO (nirogacestat).

Strategic Deals: McKesson continues to actively pursue deals, divestitures and acquisitions to drive growth, raising our optimism. In August 2023, the company extended its relationship with Genpact. The extension was aimed at bringing continued efficiency and automation capabilities to McKesson’s finance operations, utilizing automation and AI solutions.

Strong Q2 Results: McKesson’s robust second-quarter fiscal 2024 results buoy optimism. The company recorded a robust uptick in its overall top line. The revenue uptick was primarily driven by growth in the U.S. Pharmaceutical segment, resulting from increased prescription volumes, including higher volumes from retail national account customers, specialty products, and GLP-1 medications.

Downsides

Weak Trends: McKesson distributes generic pharmaceuticals, which are subject to price fluctuation. The Distribution Solutions segment continues to experience weaker generic pharmaceutical pricing trends. Continued volatility, unfavorable pricing trends, reimbursement of generic drugs and significant fluctuations in the nature, frequency and magnitude of generic pharmaceutical launches could have a material adverse impact on McKesson.

Stiff Competition: Distribution Solutions faces stiff competition both in terms of price and service from various full-line, short-line and specialty wholesalers, service merchandisers, self-warehousing chains, manufacturers engaged in direct distribution, third-party logistics companies and large-payer organizations. Moreover, the company depends on fewer suppliers for its products. As a result, it is not in a position to negotiate pricing.

Key Picks

Some better-ranked stocks in the broader medical space are DaVita Inc. DVA, Merit Medical Systems, Inc. MMSI and Integer Holdings Corporation ITGR.

DaVita, sporting a Zacks Rank #1 (Strong Buy), has an estimated long-term growth rate of 17.3%. DVA’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 36.6%. You can see the complete list of today’s Zacks #1 Rank stocks here.

DaVita’s shares have gained 34.1% compared with the industry’s 9.1% rise in the past year.

Merit Medical, carrying a Zacks Rank of 2 (Buy) at present, has an estimated long-term growth rate of 11.5%. MMSI’s earnings surpassed estimates in each of the trailing four quarters, with the average being 14.4%.

Merit Medical has gained 6.2% compared with the industry’s 11.7% rise in the past year.

Integer Holdings, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 15.8%. ITGR’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 11.9%.

Integer Holdings’ shares have rallied 41.2% against the industry’s 0.5% decline in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

DaVita Inc. (DVA) : Free Stock Analysis Report

McKesson Corporation (MCK) : Free Stock Analysis Report

Merit Medical Systems, Inc. (MMSI) : Free Stock Analysis Report

Integer Holdings Corporation (ITGR) : Free Stock Analysis Report