MercadoLibre (NASDAQ:MELI) Reports Upbeat Q4 But Stock Drops

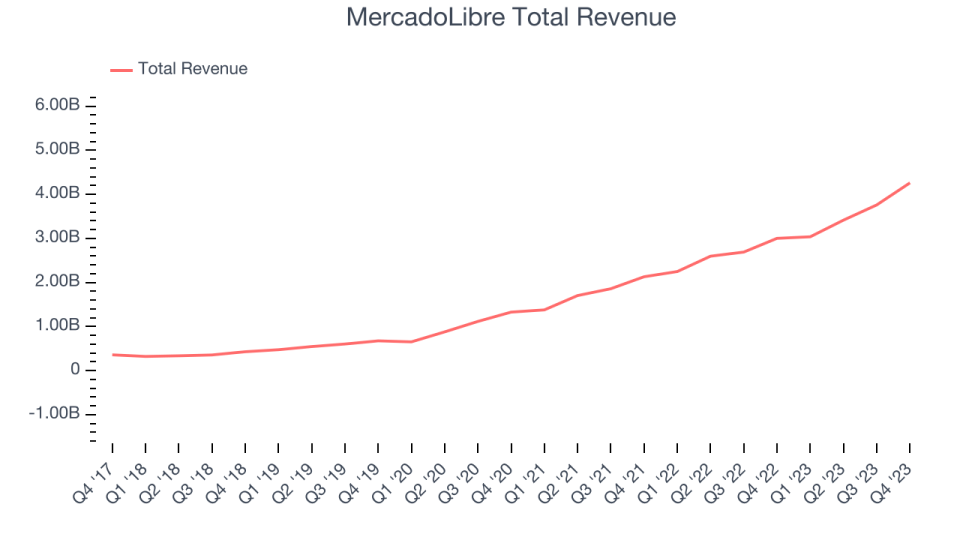

Latin American e-commerce and fintech company MercadoLibre (NASDAQ:MELI) reported results ahead of analysts' expectations in Q4 FY2023, with revenue up 41.9% year on year to $4.26 billion. Its GAAP profit of $3.25 per share was flat year on year.

Is now the time to buy MercadoLibre? Find out by accessing our full research report, it's free.

MercadoLibre (MELI) Q4 FY2023 Highlights:

Revenue: $4.26 billion vs analyst estimates of $4.13 billion (3.2% beat)

EPS: $3.25 vs analyst estimates of $6.96 (53.3% miss)

Free Cash Flow of $1.75 billion, up 114% from the previous quarter

Gross Margin (GAAP): 45.9%, down from 74.9% in the same quarter last year

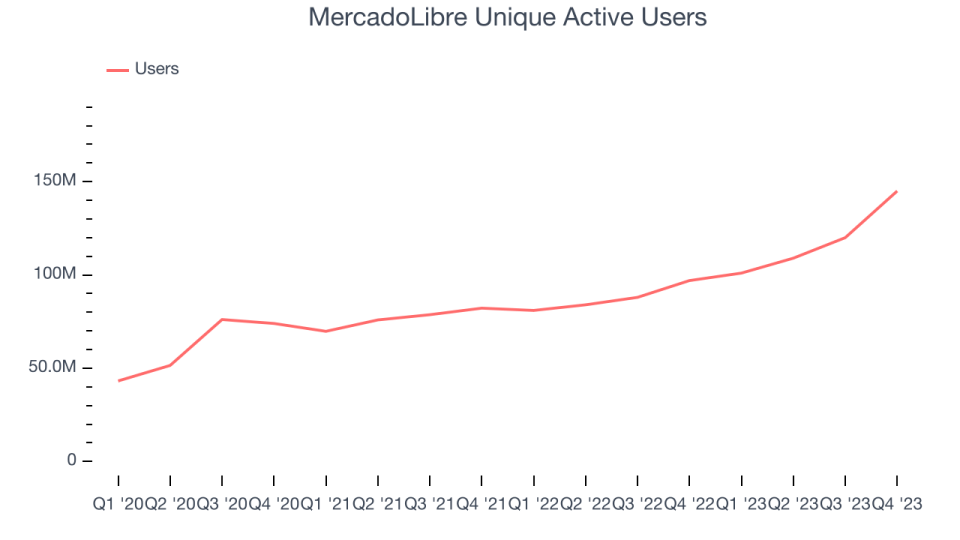

Unique Active Users: 145 million, up 48 million year on year

Market Capitalization: $87.86 billion

Originally started as an online auction platform, MercadoLibre (NASDAQ:MELI) is a one-stop e-commerce marketplace and fintech platform in Latin America.

Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Sales Growth

MercadoLibre's revenue growth over the last three years has been exceptional, averaging 56.8% annually. This quarter, MercadoLibre beat analysts' estimates and reported impressive 41.9% year-on-year revenue growth.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Usage Growth

As an online marketplace, MercadoLibre generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, MercadoLibre's daily active users, a key performance metric for the company, grew 24.6% annually to 145 million. This is fast growth for a consumer internet company.

In Q4, MercadoLibre added 48 million daily active users, translating into 49.5% year-on-year growth.

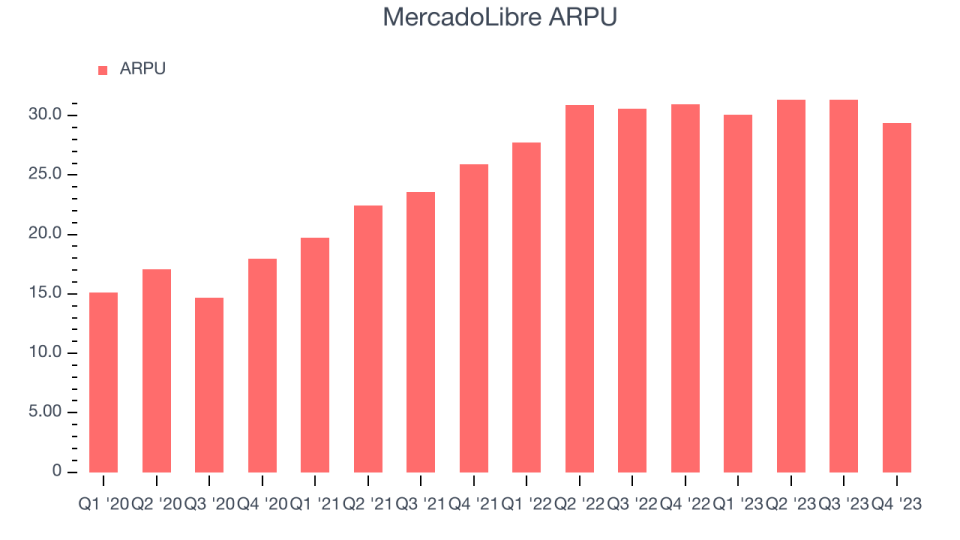

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like MercadoLibre because it measures how much the company earns in transaction fees from each user. Furthermore, ARPU gives us unique insights as it's a function of a user's average order size and MercadoLibre's take rate, or "cut", on each order.

MercadoLibre's ARPU growth has been excellent over the last two years, averaging 16.8%. The company's ability to increase prices while growing its daily active users at such a fast rate reflects the strength of its platform, as its users are spending significantly more than last year. This quarter, ARPU declined 5% year on year to $29.39 per user.

Key Takeaways from MercadoLibre's Q4 Results

We were impressed by MercadoLibre's robust user growth this quarter, enabling it to beat analysts' revenue, total payment volume (TPV), and gross merchandise volume (GMV) estimates (TPV of $56.5 billion vs estimates of $49 billion, GMV of $13.5 billion vs estimates of $12.4 billion). Specifically, the company's new credit card offering for its Brazil and Mexico customers stood out, helping MercadoLibre accelerate its TPV growth to 154% year on year in Q4 vs 63% growth for the full year 2023.

Double-clicking into the commerce side of the business, two segments stood out during the quarter: Logistics and Advertising. On the logistics side, MELI delivered more items per vehicle in 2023 as customers increasingly utilized its loyalty program, MELI+ (similar to Amazon Prime). The increased deliveries per vehicle boosted the company's efficiency, and it ended 2023 having shipped over 50% of all e-commerce orders in Brazil and over 80% of all e-commerce orders in Mexico. On the nascent but rapidly growing advertising side of the business, MercadoLibre added 50,000 new advertisers to its platform in 2023 and grew its advertising revenue by 70% year on year.

We think this was a great quarter that should delight shareholders, but the market is likely spooked by the company's headline numbers as its operating margin and EPS missed analysts' estimates by a wide margin. Looking under the hood, however, we can see that its lower profitability was caused by 1) non-recurring, non-cash expenses of $351 million that are mostly related to outstanding tax liabilities from a 2014 court case it had with the Brazilian federal tax authority, 2) lower Logistics segment margins as it offered more free shipping subsidies to customers in Brazil and Mexico, and 3) faster growth in its 1P commerce business (where it holds the inventory), which has lower margins than its 3P marketplace business (but is still additive to overall profit dollars).

Although the stock is down 8.1% after reporting, our analysis shows the reasons above do not impact the company's fundamentals. MELI is still operating with strength and momentum, and the stock currently trades at $1,673.99 per share.

So should you invest in MercadoLibre right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.