Merck vs Eli Lilly: Which Pharma Stock Is A Better Pick?

The pharmaceutical industry is considered to be more resilient in difficult economic times compared to other industries. However, this time around, the coronavirus-led lockdowns and social distancing restrictions resulted in fewer doctor visits and prescriptions filled, which in turn hurt pharma companies' drug sales. The cancellation and deferral of elective procedures also had an adverse impact on several companies in the healthcare space.

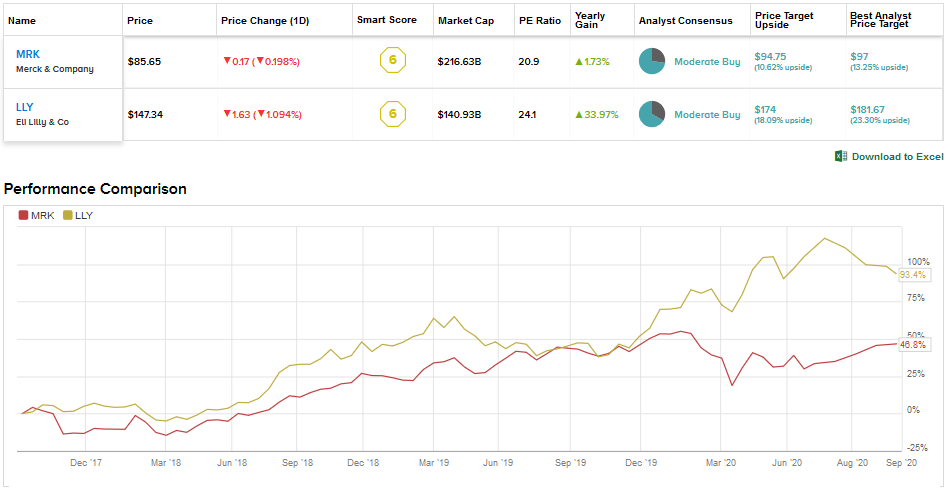

We will analyze the recent performance of two leading pharma companies, Merck and Eli Lilly, using the TipRanks’ Stock Comparison tool, to see which stock offers a more compelling investment opportunity.

Merck (MRK)

The COVID-19 pandemic put a $1.6 billion dent on Merck’s second-quarter sales, leading to a 7.6% decline in overall sales to $10.9 billion. Adjusted EPS grew over 5% to $1.37 despite weak sales due to higher unrealized gains on securities (mainly from investments in Moderna and MGM) and a lower tax rate. What's more, the company beat analysts’ sales and earnings expectations and raised its full-year guidance.

Merck’s blockbuster cancer drug Keytruda delivered sales of $3.39 billion in the second quarter, reflecting 29% growth year-on-year. The cancer drug generated sales of over $11 billion for Merck in 2019. On Aug. 24, Keytruda won two new approvals from the Japan Pharmaceuticals and Medical Devices Agency to treat a type of esophageal cancer and for use in a six-week dosing schedule.

In addition, Merck is spinning off its women’s health, biosimilars and legacy products business into a company called Organon & Co. The spin-off, which is expected to be completed in the first half of 2021, will help Merck focus on key growth areas like Keytruda and other cancer drugs, vaccines and animal health. In total, Merck has a pipeline, which includes 24 phase 3 trials.

On the COVID-19 front, Merck announced two vaccine development efforts in the second quarter. One vaccine development is in collaboration with IAVI (International AIDS Vaccine Initiative) and the other through the June acquisition of Austrian vaccine maker Themis Bioscience. Merck has also teamed up with Ridgeback Biotherapeutics to develop an oral antiviral candidate for COVID-19. This compound is in a Phase 2 clinical trial.

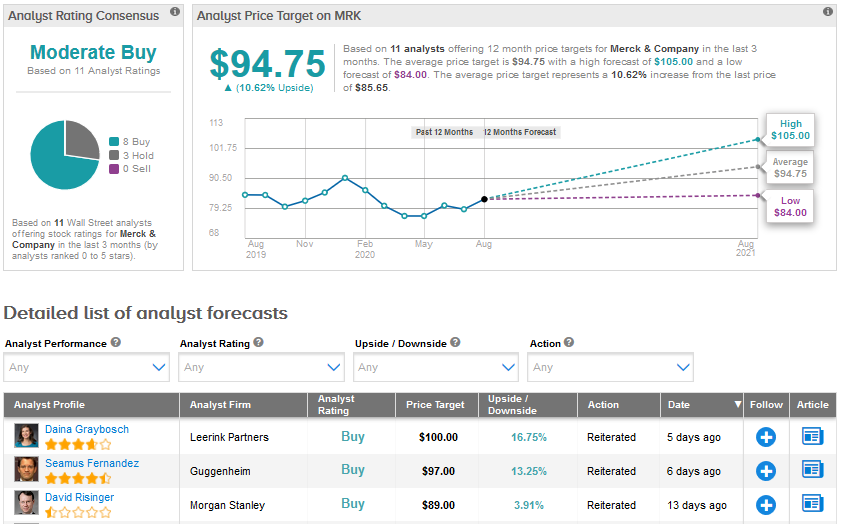

Following second-quarter results, Mizuho Securities analyst Mara Goldstein reiterated a Buy rating on the stock with a $100 price target. Highlighting the company’s efforts in developing a COVID-19 treatment, the analyst said, “MRK's vaccine efforts are becoming more visible and this, in our view, is upside.”

Goldstein added, “MRK's Covid-19 drugs lag competitors but the company is positioning itself with multiple vaccines that may address a variety of patient populations, including older more vulnerable populations with cardiovascular disease.” (See MRK stock analysis on TipRanks)

The Street has a Moderate Buy analyst consensus for Merck based on 8 Buys, 3 Holds and no Sells. The stock has declined 5.8% so far in 2020. Looking ahead, the average analyst price target of $94.75 indicates upside potential of about 11% over the next 12-months.

Eli Lilly (LLY)

Eli Lilly is considered one of the leading players in the diabetes space with drugs like Trulicity, Humalog, Humulin, and Basaglar. Notably, Trulicity alone contributed over $4 billion to sales in 2019. The drugmaker's results in the first quarter benefited from patients and consumers stockpiling on their products amid the pandemic lockdown. Meanwhile, Eli Lilly’s second-quarter revenue lagged analysts’ forecast and declined 2.4% Y/Y to $5.50 billion.

Aside from Trulicity, which delivered revenue of $1.23 billion (20% Y/Y growth), other drugs that performed well in the second quarter included Taltz, Jardiance, Cyramza, Verzenio, Olumiant, Emgality and Tyvyt. Second-quarter adjusted EPS was ahead of the Street consensus and rose 26% to $1.89 driven by higher other income from favorable mark-to-market adjustments on investment securities.

Eli Lilly raised its full-year EPS guidance citing "expectations of lower marketing, selling and administrative expenses, higher other income and a lower effective tax rate". However, the company maintained its revenue outlook.

As of the end of July, Eli Lilly’s pipeline included 18 drugs in Phase 3 trials. Beyond the company’s strong diabetes portfolio, the company is gaining traction in oncology. Cancer drugs Alimta and Cyramza contributed $2.1 billion and $925 million respectively to sales last year.

In June, the company announced positive Phase 3 data for Verzenio, an early breast cancer treatment, which will open up a new growth market for the drug. Eli Lilly plans to submit the data to regulatory authorities by the end of this year. Verzenio is already approved for metastatic breast cancer and advanced breast cancer. Its sales increased 56% in the second quarter to about $209 million.

On Aug. 18, Eli Lilly announced the global expansion of its collaboration with Innovent Biologics for immuno-oncology drug Tyvyt. The two companies currently co-commercialize the drug in China. The extended alliance will give the drugmaker an exclusive license to Tyvyt in markets outside of China.

Eli Lilly’s COVID-19 efforts include two potential antibodies called LY-CoV555 (began Phase 3 trial in early August) and JS016, as well as the rheumatoid arthritis drug Olumiant, which is now being studied for treating hospitalized cases of COVID-19.

Barclays analyst Carter Gould believes that the stock sell-off following Eli Lilly's second-quarter results and due to the lack of incremental disclosures about COVID-19 efforts and the discontinuation of the company’s KRAS G12C inhibitor was a "meaningful over-reaction".

Gould raised his price target to $170 from $160 and maintained a Buy rating saying that Eli Lilly shares are the "most attractive they've been in two plus months". Moreover, the analyst noted that the "further de-risking of twin growth pillars," Verzenio and tirzepatide along with "optionality" from multiple other readouts "should warrant further multiple expansion from here". (See LLY stock analysis on TipRanks)

Eli Lilly stock has advanced about 12% year-to-date. Shares are poised to appreciate another 18.1% as indicated by the average analyst price target of $174. A Moderate Buy consensus for the stock breaks down into 6 Buys, 3 Holds and no Sell ratings.

Merck or Eli Lilly?

About 73% of analysts covering Merck stock have a Buy rating compared to 67% in the case of Eli Lilly. Both Merck and Eli Lilly have strong growth prospects over the long-term. However, Merck’s blockbuster oncology drug Keytruda, its lower valuation compared to Eli Lilly, and a higher dividend yield (2.9% against Eli Lilly’s 2%) make it a better pharma pick in the current scenario.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment