Merit Medical (MMSI) Expands Suite via Buyouts, Revises FY23 View

Merit Medical Systems, Inc. MMSI completed the acquisition of a portfolio of dialysis catheter products and the BioSentry Biopsy Tract Sealant System from AngioDynamics, Inc. ANGO. This follows Merit Medical’s recent acquisition of the Surfacer Inside-Out Access Catheter System from Bluegrass Vascular Technologies, Inc.

Management believes that these acquisitions will likely strengthen its position in the dialysis and biopsy markets, besides expanding its growing specialty dialysis device offering (which includes WRAPSODY Cell-Impermeable Endoprosthesis, HeRO Graft and the Surfacer System devices).

These latest buyouts are a significant stepping stone for Merit Medical toward solidifying its foothold in the global dialysis space.

Rationale Behind the Acquisitions

Merit Medical’s acquired dialysis catheter portfolio includes the BioFlo DuraMax Dialysis Catheter with Endexo Technology, a proprietary material more resistant to thrombus (blood clot) accumulation, in vitro, unlike conventional non-coated dialysis catheters. Per the company, thrombus formation can block blood flow through a catheter, thus preventing adequate dialysis treatment.

AngioDynamics’ BioSentry Biopsy Tract Sealant System, designed specifically to reduce the incidence of biopsy-related pneumothorax (collapsed lung), is expected to complement Merit Medical’s comprehensive biopsy portfolio. Per Merit Medical’s estimates, pneumothorax, a potentially life-threatening complication that can extend hospitalization, occurs in approximately one-quarter of patients undergoing lung biopsy.

The Surfacer, a device designed to obtain right-sided central venous access in patients with venous obstructions, is expected to provide this population with access to life saving therapies, including hemodialysis and chemotherapy.

Per Merit Medical’s management, these selective investments are expected to expand its product portfolio in key strategic markets that leverage the company’s existing commercial footprint. Management also feels that since many dialysis patients rely on these solutions to receive vital therapies, thus combining this broad portfolio of interventional solutions within Merit Medical will allow it to leverage its physician relationships and commercial infrastructure to serve more patients.

Financial Implications

The acquired assets are expected to contribute revenues from the closing date through Dec 31, 2023, and dilute Merit Medical’s previously-guided GAAP gross and operating margin forecasts. The acquisitions are expected to be slightly dilutive to its full-year 2023 non-GAAP net income and non-GAAP earnings per share (EPS).

The acquisitions are expected to be accretive to non-GAAP net income and EPS in the first full-year post-close but dilutive to GAAP net income and EPS for that period. The acquisitions are expected to be accretive to non-GAAP gross and operating margins, non-GAAP net income and non-GAAP EPS in the second full-year post-close but dilutive to GAAP gross and operating margins, net income and EPS for that period.

Guidance

Merit Medical has revised its outlook for 2023, including the impacts of acquisitions of AngioDynamics’ dialysis catheter portfolio and BioSentry Biopsy Tract Sealant System, and the Surfacer Inside-Out Access Catheter System.

Net revenues for 2023 are now projected to be between $1.230 billion and $1.244 billion, reflecting an increase of approximately 7-8% over the comparable reported figures of 2022. This is up from the earlier guidance of $1.217 billion-$1.229 billion, reflecting an increase of approximately 6-7% over the comparable reported figures of 2022. The Zacks Consensus Estimate for the same stands at $1.24 billion.

Net revenues from the cardiovascular segment are now expected to be in the range of $1.192 billion-$1.206 billion, representing an increase of approximately 7-8% over the comparable reported figures of 2022. This is up from the prior outlook of $1.179 billion-$1.191 billion, representing an increase of approximately 5-6% over the comparable reported figures of 2022.

The endoscopy segment’s net revenues are continued to be projected between $37.8 million and $38.1 million, representing an increase of approximately 15-16% over the comparable reported figures of 2022. This is up from the prior outlook of $37.5 million-$37.8 million, representing an increase of approximately 14-16% over the comparable reported figures of 2022.

Adjusted EPS for 2023 is now projected to be within $2.81-$2.92, down from the earlier projection of $2.83-$2.93. The Zacks Consensus Estimate for the same stands at $2.89.

Industry Prospects

Per a report by Allied Market Research, the global dialysis market was valued at $91,205.0 million in 2020 and is projected to reach $129,756.8 million by 2028 at a CAGR of 4.7%. Factors like the increase in number of diabetic and hypertension patients, a rise in the number of end stage renal disease patients and a preference over kidney transplantation are likely to drive the market.

Given the market potential, the latest buyouts are expected to provide a significant boost to Merit Medical’s business in the niche space.

Notable Developments

In April, Merit Medical announced its first-quarter 2023 results, wherein it registered a solid year-over-year uptick in the top and bottom lines. The company saw revenue growth in both its segments and across all the product categories within its Cardiovascular unit. Robust performances in the United States and outside were also recorded.

In March, Merit Medical announced the expansion of its SwiftNINJA Steerable Microcatheter product line, which belongs to its delivery systems portfolio. The new sizes include a low-profile 2.4F distal diameter option in 125-cm and new longer 150-cm lengths.

In February, Merit Medical announced the FDA’s grant of Breakthrough Device Designation for the SCOUT MD Surgical Guidance System.

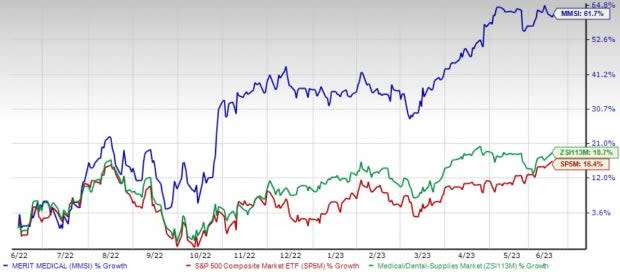

Price Performance

Merit Medical stock has gained 61.7% over the past year compared with the industry’s 18.6% rise and the S&P 500's 16.4% growth.

Image Source: Zacks Investment Research

Zacks Rank & Other Key Picks

Currently, Merit Medical carries a Zacks Rank #2 (Buy).

A couple of other top-ranked stocks in the broader medical space are Hologic, Inc. HOLX and Masimo Corporation MASI.

Hologic, carrying a Zacks Rank #2 at present, has an estimated growth rate of 5.1% for fiscal 2024. HOLX’s earnings surpassed estimates in all the trailing four quarters, the average being 27.3%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Hologic has gained 15.7% compared with the industry’s 14.3% rise in the past year.

Masimo, carrying a Zacks Rank #2 at present, has an estimated growth rate of 3.7% for 2023. MASI’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 9.9%.

Masimo has gained 28.3% compared with the industry’s 14.3% rise over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AngioDynamics, Inc. (ANGO) : Free Stock Analysis Report

Hologic, Inc. (HOLX) : Free Stock Analysis Report

Masimo Corporation (MASI) : Free Stock Analysis Report

Merit Medical Systems, Inc. (MMSI) : Free Stock Analysis Report