Midstream Positions for Ballooning U.S. LNG Exports

This article was originally published on ETFTrends.com.

Summary

U.S. LNG export capacity set to increase by 80% to 24.9 billion cubic feet per day (Bcf/d) over the next few years based on projects already under construction.

Several more projects are signing long-term offtake agreements with a view to starting construction this year.

Midstream companies are positioning for growing LNG exports by investing in natural gas infrastructure along the Gulf Coast, including through acquisitions.

Global demand for liquefied natural gas (LNG) -- natural gas that is supercooled into liquid form in order to be transported by ship -- is expected to grow considerably. As the world’s largest producer of natural gas, the U.S. will play a significant role in meeting that demand. This note provides an update on U.S. LNG projects and how midstream companies are positioning to benefit from growing U.S. LNG exports.

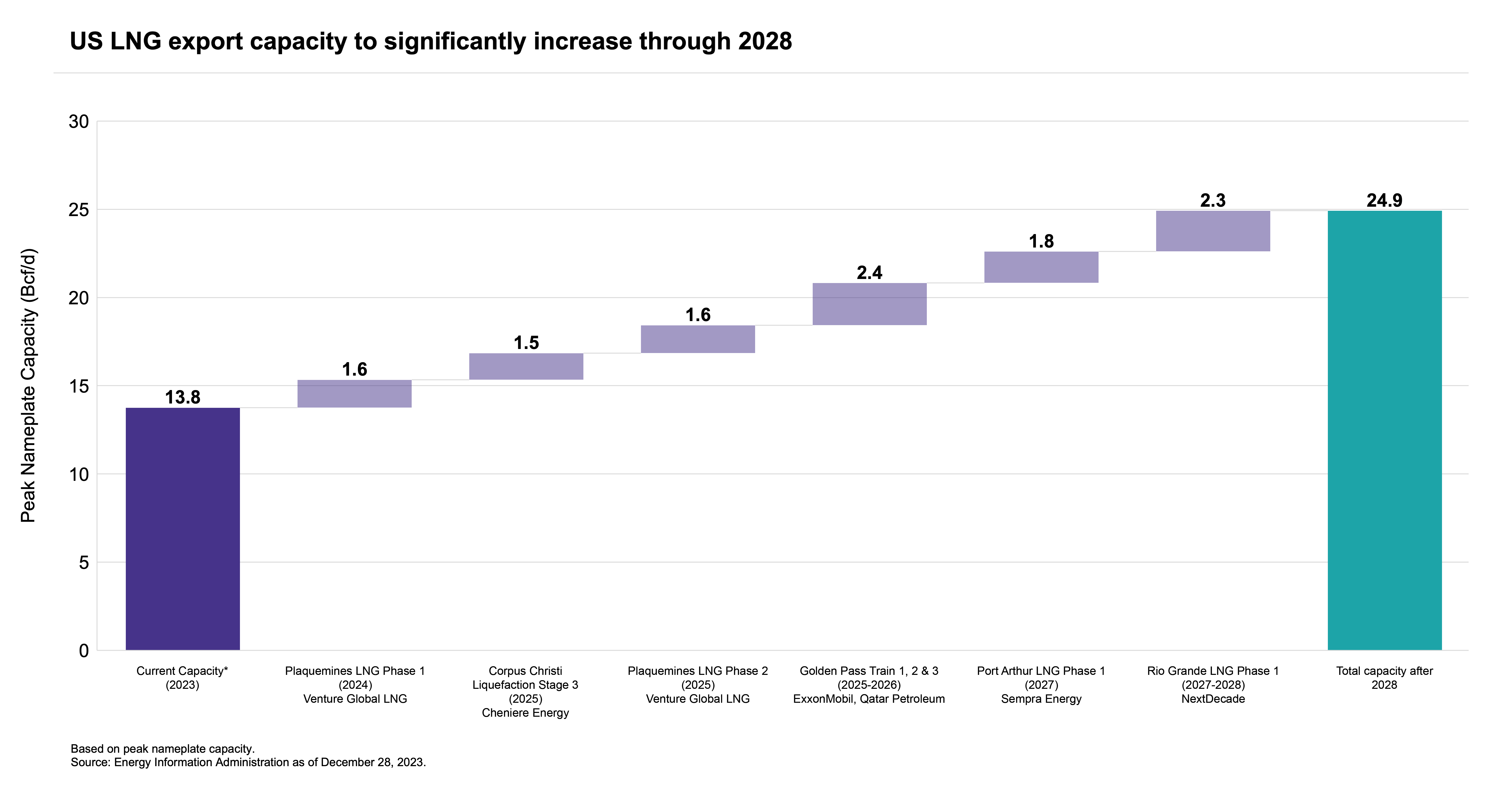

US LNG Export Capacity Will Ramp in Late 2024 and Into 2025

In 2023, the U.S. became the world’s largest LNG exporter, surpassing Australia and Qatar for the first time. With ample natural gas reserves and an easy path to production growth, U.S. LNG export capacity is poised to increase substantially over the next few years.

As shown in the chart below, the U.S. currently has ~13.8 billion cubic feet per day (Bcf/d) of operational liquefaction capacity. Another 11.2 Bcf/d is under construction. The projects under construction represent an 81% increase in U.S. LNG capacity by 2028. They are underpinned by long-term offtake agreements that typically extend for up to 20 years. This is a significant step change in capacity. Yet more LNG projects are likely to start construction this year.

More Projects Awaiting Green Light Continue to Strike Deals

Global LNG demand is expected to grow by upward of 60% through 2040 (read more). Customers are actively signing long-term offtake contracts or sales and purchase agreements (SPAs) with U.S. LNG projects under development. These agreements are critical for projects to reach a final investment decision (FID). That is the point at which a company commits to move forward with a project and starts construction. Reaching FID depends on securing financing and signing sufficient offtake agreements.

Several LNG projects are inking deals today that extend into the 2040’s in pursuit of FID. The largest of these projects is Energy Transfer’s (ET) 2.2 Bcf/d Lake Charles LNG project in Louisiana. Lake Charles has signed SPAs and heads of agreement for about half of its capacity. As discussed on the 3Q23 earnings call, ET is currently looking for equity partners with plans to retain an approximate 20% interest in the project. Last week, Japanese utility Kyushu Electric Power was reported to be in talks with ET to buy a 10% stake in Lake Charles alongside a 20-year offtake agreement. Beyond securing partners and SPAs, Lake Charles LNG has faced some regulatory hurdles. And it is waiting on an update from the Department of Energy (DOE) regarding its export license.

Other projects include Delfin LNG, a proposed 1.6 Bcf/d facility off the coast of Louisiana consisting of up to four floating LNG (FLNG) vessels. As of November, Delfin LNG was in the final phase toward reaching FID on three of its four FLNG vessels. NextDecade’s (NEXT) Rio Grande LNG project is targeting a positive FID for additional capacity in 2H24. An expansion at Sempra’s (SRE) Cameron LNG of 0.9 Bcf/d is also expected to move forward. Glenfarne’s Texas LNG in Brownsville is also expected to start construction this year.

These projects have received approval from the DOE and Federal Energy Regulatory Commission. In the case of Delfin, approval has been made by the Maritime Administration. According to recent media reports, the Biden Administration is considering incorporating climate impacts into new LNG project approvals when determining if a project is in the national interest. However, details remain vague.

Though earlier stage, Cheniere (LNG) and Cheniere Energy Partners (CQP) have announced both SPAs and integrated production marketing (IPM) agreements in support of a proposed expansion of Sabine Pass. Under an IPM, a natural gas producer, in this case, ARC Resources (ARX CN), sells gas to Cheniere based on a global LNG price less a fixed liquefaction fee, shipping costs, and regasification fee.

These projects could add meaningful capacity above and beyond the growth shown in the chart above. Among the public companies developing incremental LNG export capacity, LNG, NEXT, and SRE are included in the Alerian Liquefied Natural Gas Index (ALNGX).

Midstream Investing to Support LNG Export Growth

The Gulf Coast is home to all of the LNG export projects listed above. The natural gas supplies for these facilities will largely come from Texas and Louisiana, including the Permian (read more) and Haynesville (read more), respectively. The need to transport natural gas to LNG export facilities has created growth opportunities for midstream companies. These companies tend to see lengthy pipeline contracts (~20 years) with liquefaction customers. Growing demand from LNG facilities has underpinned newbuild projects or expansions of existing pipelines, while also motivating asset-level acquisitions.

In 4Q23, Kinder Morgan (KMI) announced it was acquiring STX Midstream, a pipeline system which includes gas pipelines from West Texas to the Gulf Coast, for $1.8 billion. The acquisition is expected to help KMI capitalize on LNG-related opportunities alongside servicing other customers. Similarly, Williams (WMB) acquired natural gas storage and pipeline assets in Louisiana and Mississippi for ~$2 billion as they look to satisfy growing LNG and power generation demand. Several of the constituents in the Alerian Midstream Energy Select Index (AMEI) are positioning to benefit from growing LNG exports, including ET, KMI, LNG, NEXT, and WMB.

Bottom Line

With a constructive long-term outlook for global demand, U.S. LNG projects have continued to advance supported by significant customer commitments into the 2040s. Midstream companies are investing in natural gas infrastructure to benefit from the ongoing growth in US LNG exports.

Related Research

Global LNG Market Poised for Long-Term Growth

U.S. LNG Projects Advance Even as Global Prices Slump

LNG Has Haynesville Humming – Benefits Midstream/MLPs

Canadian LNG Projects Advance to Meet Asian Demand

Stifel Analyst on the LNG Market and Overlooked Investment Opportunities

ALNGX is the underlying index for the Roundhill Alerian LNG ETF (LNGG). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX).

Vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for LNGG, ENFR, and ALEFX, for which it receives an index licensing fee. However, LNGG, ENFR, and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of LNGG, ENFR, and ALEFX.

For more news, information, and strategy, visit the Energy Infrastructure Channel.

POPULAR ARTICLES AND RESOURCES FROM ETFTRENDS.COM