Moelis & Company's (MC) Organic Growth Aids Amid Cost Woes

Moelis & Company MC is well poised with its organic growth initiatives, global expansion efforts, decent capital deployments and its diverse operations across sectors and industries. However, elevated operating expenses, along with geopolitical and macroeconomic headwinds, are likely to hamper the company's profitability.

Moelis & Company’s growth continues to be driven by strong organic performance. The company’s revenues witnessed a compound annual growth rate (CAGR) of 7.6% over the last five years (2017-2022). The growth was mainly driven by its geographical expansion efforts and an increase in average fees earned per completed transaction. Though our estimates project total revenues (adjusted) to decline 15.9% this year, the metric is expected to rebound and grow 36.2% and 31.6% in 2024 and 2025, respectively.

Moelis & Company’s business is significantly diversified across various sectors and geographically, with no significant client concentration. Thus, global expansion and diversification are expected to continue supporting its profitability.

MC’s capital deployment activities also look solid. Since 2014, the company has announced ten dividend hikes. Also, in 2021, it announced an increase in its share repurchase authorization by $100 million. As of Mar 31, 2023, $62.5 million worth of authorization remained. With no debt and a strong balance sheet position, the company’s capital deployment actions look sustainable.

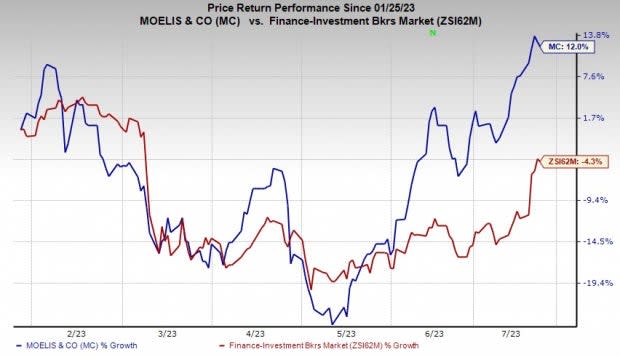

Over the past six months, shares of this Zacks Rank #3 (Hold) company have rallied 12% against the industry’s fall of 4.3%.

Image Source: Zacks Investment Research

However, Moelis & Company has been witnessing a persistent rise in expenses. It witnessed a CAGR of 8.1% over the last five years (2017-2022). As it expands operations into sectors and products, overall costs are anticipated to remain elevated. Our estimates for total expenses (GAAP) reflect a CAGR of 13.6% by 2025.

Moelis & Company is a geographically diversified company with presence in almost all the major global markets. It derives almost 22% of its total revenues (GAAP) from international operations. We estimate this to be around 21% by 2025. A plethora of risks stemming from the regulatory and political environment, foreign exchange fluctuations and the performance of the regional economy can affect prospects.

Stocks Worth Considering

A couple of better-ranked finance stocks worth considering are T. Rowe Price TROW and Virtus Investment Partners VRTS, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for T. Rowe Price’s current-year earnings has been revised marginally upward over the last seven days. In the past six months, TROW shares have rallied 2.6%.

Earnings estimates for Virtus Investment Partners for 2023 have been revised marginally upward over the last seven days. In the past six months, VRTS shares have lost 2.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

T. Rowe Price Group, Inc. (TROW) : Free Stock Analysis Report

Virtus Investment Partners, Inc. (VRTS) : Free Stock Analysis Report

Moelis & Company (MC) : Free Stock Analysis Report