Mondelez (MDLZ) Gains on Buyouts, Emerging Market Strength

Mondelez International, Inc. MDLZ has been benefiting from its solid brands, which can be attributed to the company’s prudent buyouts as well as innovation. Apart from this, the strength in emerging markets has been working well for Mondelez. Saving and pricing efforts are also helping the company amid increased cost inflation.

These factors were witnessed when the company reported fourth-quarter 2021 results recently, wherein the top and bottom lines increased year over year and the former cruised past the Zacks Consensus Estimate. The company continued to benefit from its strategic efforts, with a volume-induced top line, robust profit, higher investments in brands and capacities and a solid free cash flow generation.

On its fourth-quarter 2021 call, management said that it expects at-home consumption to remain elevated, given the recent spike in Omicron cases. This, along with consumers’ increased indulgence of comfort foods, bodes well for the company’s core biscuits and chocolate categories. For 2022, management expects organic net revenues of more than 3% and a high single-digit increase in adjusted earnings per share or EPS at constant currency or cc. These projections go in tandem with the company’s long-term algorithms. Pricing and volumes are likely to be major top-line drivers. Let’s delve deeper.

Mondelez International, Inc. Price, Consensus and EPS Surprise

Mondelez International, Inc. price-consensus-eps-surprise-chart | Mondelez International, Inc. Quote

Factors Backing Mondelez Growth

Mondelez has always been keen on expanding its business through acquisitions and alliances. In January 2022, the company acquired Chipita S.A., which is a major producer of sweet and salty snacks in Central and Eastern Europe. In 2021, MDLZ took over a renowned sports performance and active nutrition brand, Grenade. Grenade’s on-trend and tasty products position Mondelez to grow in the United Kingdom as well as other markets. Further, the company acquired the Australia-based food company — Gourmet Food Holdings — which operates in the premium biscuit and cracker category. Mondelez completed the acquisition of Hu Master Holdings, the parent company of Hu Products on Jan 4, 2021. The acquisition of Hu provides further growth opportunities in chocolates and cross-category potential in crackers for Mondelez. Hu, Grenade and Gourmet Food buyouts contributed to the company’s top line in the fourth quarter of 2021.

Moving on, the company remains encouraged by the underlying emerging market strength. In the fourth quarter of 2021, revenues from emerging markets increased 8.8% to $2,692 million while rising 11.1% on an organic basis. The company saw strength in most countries, particularly the BRICS. The company is boosting its presence in emerging markets as evident from the addition of its distribution in 300,000 and 200,000 more respective stores in China and India in 2021. Management remains optimistic about the emerging markets outlook for the near and long term despite some pandemic-related hurdles in a few countries.

Apart from this, MDLZ has been undertaking some major steps to enhance savings, which fuel margins and cash flow. Further, robust pricing actions have been aiding the company. During the fourth quarter of 2021, pricing actions boosted organic net revenues and offered a partial respite to the company’s adjusted gross profit margin and adjusted operating margin, which were otherwise hurt by cost inflation and an adverse mix. Mondelez is on track with its Revenue Growth Management activities and more investments in people, markets as well as capabilities. The company is undertaking pricing actions to counter inflationary pressure.

Image Source: Zacks Investment Research

Will Cost Woes be Countered?

In the fourth quarter of 2021, Mondelez’s adjusted gross profit margin contracted 200 basis points (bps) to 37.2% due to increased raw material and transportation costs as well as an unfavorable mix. Also, the adjusted operating income margin contracted 90 bps to 15.4% due to the same factors.

Management stated that the company is seeing cost inflation globally, especially for transportation, packaging, edible oils and dairy. The company is also navigating through supply-chain bottlenecks due to labor shortages at third parties.

On its fourth-quarter 2021 earnings call, management guided for another year of material cost inflation, which is likely to rise in the high single digits. Though the company is undertaking robust pricing efforts, some margin pressure is still expected in the first quarter and partially in the second quarter. Management specifically expects greater supply-chain hurdles in North America in the first quarter associated with third parties and lower inventory stemming from the last year’s strike.

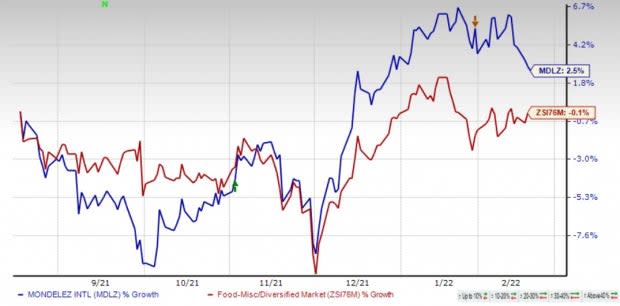

Shares of this Zacks Rank #3 (Hold) company have risen 2.5% in the past six months against the industry’s decline of 0.1%.

Looking for Solid Consumer Staple Stocks? Check These

Some top-ranked stocks are Helen of Troy HELE, Flowers Foods FLO and Medifast, Inc. MED

Helen of Troy, a designer, developer, marketer, importer and distributor, carries a Zacks Rank #1 (Strong Buy) at present. Shares of Helen of Troy have dipped 12.5% in the past six months. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Helen of Troy’s current financial-year sales and EPS suggests growth of 0.8% and 0.6%, respectively, from the year-ago reported number. HELE has a trailing four-quarter earnings surprise of 19.1%, on average.

Flowers Foods, which produces and markets packaged bakery products, carries a Zacks Rank #2 (Buy). Shares of Flowers Foods have moved up 10.9% in the past six months.

The Zacks Consensus Estimate for Flowers Foods' current financial-year sales and EPS suggests growth of 7.2% and 2.2%, respectively, from the year-ago reported number. FLO has a trailing four-quarter earnings surprise of 9%, on average.

Medifast, the manufacturer and distributor of weight loss, weight management, healthy living products, and other consumable health and nutritional products, currently carries a Zacks Rank #2. Shares of Medifast have dropped 16% in the past six months.

The Zacks Consensus Estimate for Medifast’s current financial-year sales and EPS suggests growth of about 63% and 49.3%, respectively, from the year-ago reported figure. MED has a trailing four-quarter earnings surprise of 17.3%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Flowers Foods, Inc. (FLO) : Free Stock Analysis Report

Helen of Troy Limited (HELE) : Free Stock Analysis Report

Mondelez International, Inc. (MDLZ) : Free Stock Analysis Report

MEDIFAST INC (MED) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research