Most Shareholders Will Probably Agree With SigmaTron International, Inc.'s (NASDAQ:SGMA) CEO Compensation

Key Insights

SigmaTron International will host its Annual General Meeting on 22nd of September

Total pay for CEO Gary Fairhead includes US$347.7k salary

Total compensation is similar to the industry average

Over the past three years, SigmaTron International's EPS grew by 29% and over the past three years, the total shareholder return was 13%

Performance at SigmaTron International, Inc. (NASDAQ:SGMA) has been reasonably good and CEO Gary Fairhead has done a decent job of steering the company in the right direction. As shareholders go into the upcoming AGM on 22nd of September, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. We present our case of why we think CEO compensation looks fair.

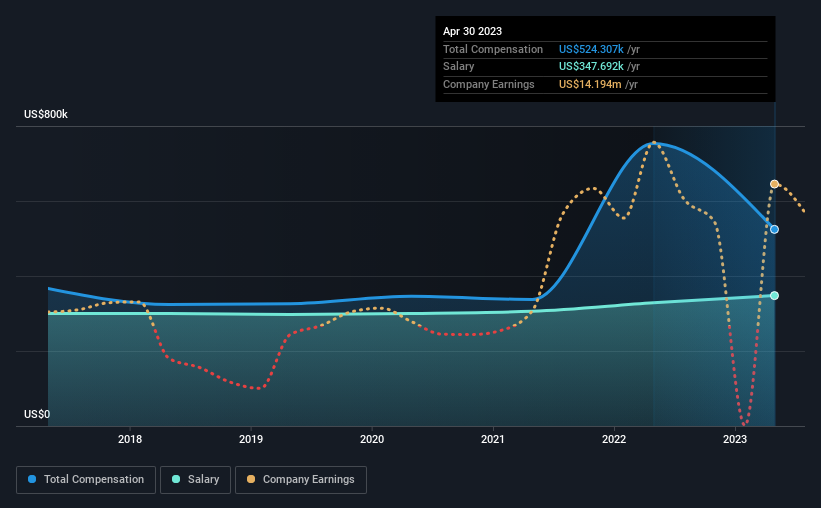

View our latest analysis for SigmaTron International

Comparing SigmaTron International, Inc.'s CEO Compensation With The Industry

Our data indicates that SigmaTron International, Inc. has a market capitalization of US$21m, and total annual CEO compensation was reported as US$524k for the year to April 2023. That's a notable decrease of 30% on last year. Notably, the salary which is US$347.7k, represents most of the total compensation being paid.

In comparison with other companies in the American Electronic industry with market capitalizations under US$200m, the reported median total CEO compensation was US$441k. So it looks like SigmaTron International compensates Gary Fairhead in line with the median for the industry. Moreover, Gary Fairhead also holds US$326k worth of SigmaTron International stock directly under their own name.

Component | 2023 | 2022 | Proportion (2023) |

Salary | US$348k | US$328k | 66% |

Other | US$177k | US$425k | 34% |

Total Compensation | US$524k | US$753k | 100% |

On an industry level, roughly 32% of total compensation represents salary and 68% is other remuneration. SigmaTron International pays out 66% of remuneration in the form of a salary, significantly higher than the industry average. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

SigmaTron International, Inc.'s Growth

Over the past three years, SigmaTron International, Inc. has seen its earnings per share (EPS) grow by 29% per year. In the last year, its revenue is up 2.4%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's nice to see revenue heading northwards, as this is consistent with healthy business conditions. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has SigmaTron International, Inc. Been A Good Investment?

With a total shareholder return of 13% over three years, SigmaTron International, Inc. shareholders would, in general, be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. In saying that, any proposed increase to CEO compensation will still be assessed on how reasonable it is based on performance and industry benchmarks.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. In our study, we found 3 warning signs for SigmaTron International you should be aware of, and 2 of them shouldn't be ignored.

Important note: SigmaTron International is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.