What You Must Know About Knoll Inc’s (NYSE:KNL) Financial Strength

Knoll Inc (NYSE:KNL) is a small-cap stock with a market capitalization of $1.02B. While investors primarily focus on the growth potential and competitive landscape of the small-cap companies, they end up ignoring a key aspect, which could be the biggest threat to its existence: its financial health. Why is it important? Assessing first and foremost the financial health is crucial, since poor capital management may bring about bankruptcies, which occur at a higher rate for small-caps. Here are few basic financial health checks you should consider before taking the plunge. However, given that I have not delve into the company-specifics, I’d encourage you to dig deeper yourself into KNL here.

How does KNL’s operating cash flow stack up against its debt?

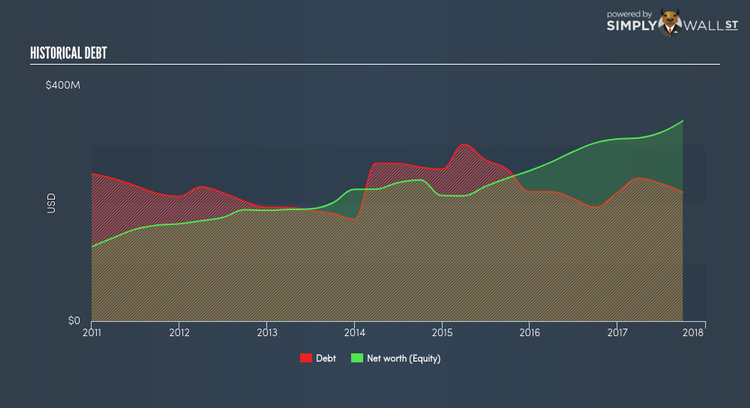

KNL has sustained its debt level by about $218.4M over the last 12 months – this includes both the current and long-term debt. At this constant level of debt, KNL currently has $9.9M remaining in cash and short-term investments for investing into the business. On top of this, KNL has generated cash from operations of $104.3M during the same period of time, leading to an operating cash to total debt ratio of 0.48x, signalling that KNL’s current level of operating cash is high enough to cover debt. This ratio can also be interpreted as a measure of efficiency as an alternative to return on assets. In KNL’s case, it is able to generate 0.48x cash from its debt capital.

Can KNL pay its short-term liabilities?

With current liabilities at $222.4M liabilities, it seems that the business has maintained a safe level of current assets to meet its obligations, with the current ratio last standing at 1.24x. Usually, for commercial services companies, this is a suitable ratio since there’s sufficient cash cushion without leaving too much capital idle or in low-earning investments.

Is KNL’s level of debt at an acceptable level?

With a debt-to-equity ratio of 64.36%, KNL can be considered as an above-average leveraged company. This is not uncommon for a small-cap company given that debt tends to be lower-cost and at times, more accessible. No matter how high the company’s debt, if it can easily cover the interest payments, it’s considered to be efficient with its use of excess leverage. A company generating earnings after interest and tax at least three times its net interest payments is considered financially sound. In KNL’s case, the ratio of 16.74x suggests that interest is excessively covered, which means that lenders may be less hesitant to lend out more funding as KNL’s high interest coverage is seen as responsible and safe practice.

Next Steps:

Are you a shareholder? KNL’s high cash coverage means that, although its debt levels are high, the company is able to utilise its borrowings efficiently in order to generate cash flow. This may mean this is an optimal capital structure for the business, given that it is also meeting its short-term commitment. Going forward, its financial position may change. You should always be keeping abreast of market expectations for KNL’s future growth on our free analysis platform.

Are you a potential investor? KNL’s high debt level shouldn’t scare off investors just yet. Its operating cash flow seems adequate to meet obligations which means its debt is being put to good use. In addition to this, the company will be able to pay all of its upcoming liabilities from its current short-term assets. In order to build your confidence in the stock, you need to further examine the company’s track record. I encourage you to continue your research by taking a look at KNL’s past performance analysis on our free platform in order to determine for yourself whether its debt position is justified.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.