National Vision (EYE) Plans to Open New Stores Amid Macro Woes

National Vision EYE continues to gain on solid positive comps. The company’s strong focus on opening new stores is also encouraging. Yet, National Vision’s high dependence on a limited number of vendors is a concern. Also, a tough competitive landscape is a threat. The stock carries a Zacks Rank #3 (Hold).

National Vision reported encouraging first-quarter 2023 results, with better-than-expected revenues. Amid an uncertain macro environment, the company delivered positive comparable sales growth in the first quarter, primarily driven by strength in its managed care business. During the reported quarter, the company opened eight new stores. It ended the quarter with 1,357 stores. However, on a year-over-year basis, the company reported a significant decline in its earnings. The contraction of both margins on escalating expenses was discouraging too.

During the quarter, National Vision opened four America's Best and four Eyeglass World stores, and closed five stores. For America's Best and Eyeglass World growth brands combined, unit growth increased 5% over the total store base last year. The company ended the quarter with 1,357 stores.

Further, the company continues to roll out its remote care capabilities, which provide doctors with additional levels of flexibility and expand exam capacity in many areas. Per the company’s first-quarter update, it remains on track with its expansion into at least an additional 200 remote-enabled stores in 2023.

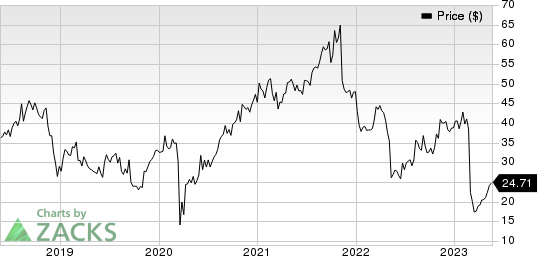

National Vision Holdings, Inc. Price

National Vision Holdings, Inc. price | National Vision Holdings, Inc. Quote

National Vision plans to continue executing its core growth initiatives and further investing in strengthening competitive advantages. In terms of store expansion, the company continues to see a sizable new opportunity with growth for many years to come. Despite many supply chain obstacles, during the first quarter, National Vision opened eight new stores and is on track to open nearly 65 to 70 new stores in 2023. The company noted that the new stores opened over the past 12 months continue to perform well and in line with the company’s expectations.

In 2023, National Vision invested $27.7 million for capital expenditures, primarily focused on new store openings and customer-facing technology investments. In 2023, capex is expected in the range of $115 million to $120 million to support key growth initiatives.

On the flip side, on a year-over-year basis, the company reported a significant decline in its earnings. The company’s gross margin contracted 45 basis points. Selling, general and administrative expenses rose 9.3%. Adjusted operating margin contracted 158 bps year over year. Moreover, the company is facing demand headwinds across its network of stores, given the current macro environment, as well as the supply challenge, in a smaller subgroup of stores, due to the constraints in eye exam capacity.

We note that National Vision operates in a highly competitive optical retail industry. The companies within the industry generally compete based on recognition of the brand name, price, convenience, selection, service and product quality. National Vision competes with national retailers like LensCrafters, Pearle Vision and Visionworks in the broader optical retail industry.

Competition exists in physical retail locations along with e-commerce platforms. The company faces a competitive threat from online sellers of contact lenses and eyewear. A number of firms are focused on selling eyeglasses in the online market like Warby Parker and Zenni Optical.

Key Picks

Some better-ranked stocks in the broader medical space are Addus Homecare Corporation ADUS, Merit Medical Systems, Inc. MMSI and Davita Inc DVA.

The Zacks Consensus Estimate for Addus Homecare’s 2023 earnings indicates 10.9% year-over-year growth. The Zacks Consensus Estimate for ADUS’s 2023 earnings has moved 0.5% north in the past 30 days.

Addus Homecare has a long-term estimated growth rate of 11.8%. The stock carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Merit Medical reported first-quarter 2023 adjusted EPS of 64 cents, beating the Zacks Consensus Estimate by 16.4%. Revenues of $297.6 million surpassed the Zacks Consensus Estimate by 5.9%. It currently carries a Zacks Rank #2.

Merit Medical has a long-term estimated growth rate of 11%. MMSI’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 20.2%.

DaVita, carrying a Zacks Rank #2 at present, has a long-term estimated growth rate of 14.6%. DVA’s earnings surpassed estimates in three of the trailing four quarters and missed in one, the average surprise being 17.3%.

DaVita has lost 1.9% compared with the industry’s 18% decline over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

DaVita Inc. (DVA) : Free Stock Analysis Report

Merit Medical Systems, Inc. (MMSI) : Free Stock Analysis Report

Addus HomeCare Corporation (ADUS) : Free Stock Analysis Report

National Vision Holdings, Inc. (EYE) : Free Stock Analysis Report