News Corp (NASDAQ:NWSA) Surprises With Q2 Sales

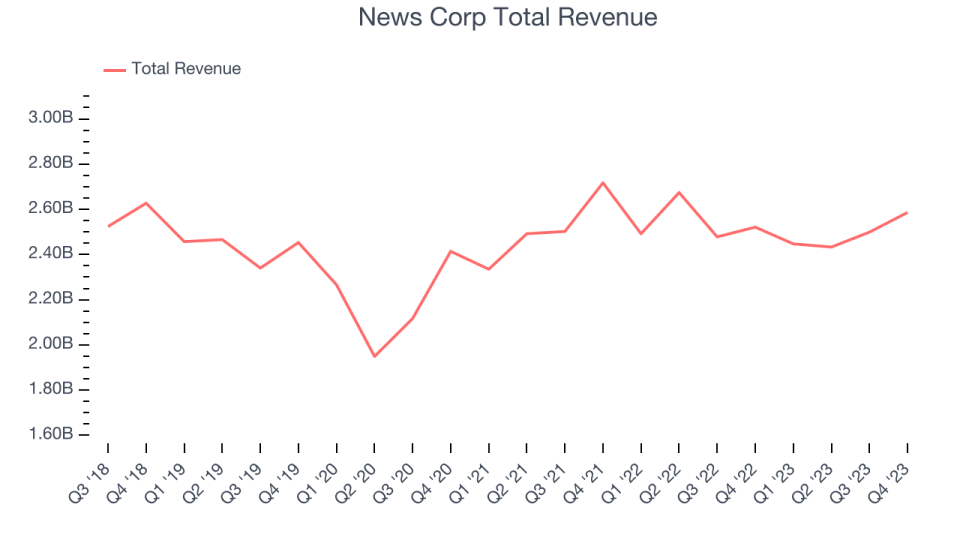

Global media and publishing company News Corp (NASDAQ:NWSA) reported results ahead of analysts' expectations in Q2 FY2024, with revenue up 2.6% year on year to $2.59 billion. It made a GAAP profit of $0.27 per share, improving from its profit of $0.14 per share in the same quarter last year.

Is now the time to buy News Corp? Find out by accessing our full research report, it's free.

News Corp (NWSA) Q2 FY2024 Highlights:

Revenue: $2.59 billion vs analyst estimates of $2.56 billion (0.9% beat)

EPS: $0.27 vs analyst estimates of $0.18 (46.8% beat)

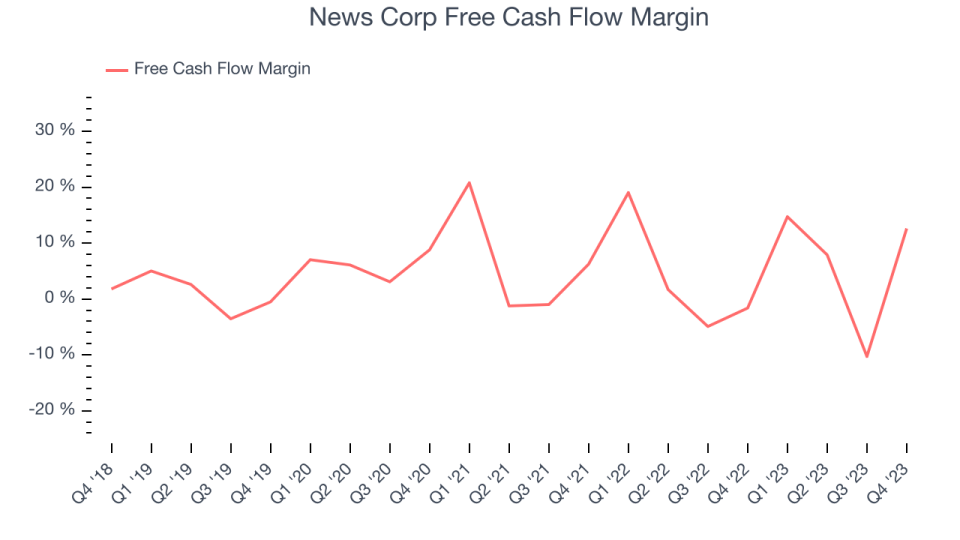

Free Cash Flow of $326 million is up from -$257 million in the previous quarter

Gross Margin (GAAP): 50.5%, up from 48.7% in the same quarter last year

Market Capitalization: $23.67 billion

Established in 2013 after a restructuring, News Corp (NASDAQ:NWSA) is a multinational conglomerate known for its news publishing, broadcasting, digital media, and book publishing.

Publishing

Publishing companies have been facing secular headwinds in the form of consumers abandoning traditional media in favor of streaming services. As a result, many publishing companies have evolved into hybrid or purely digital platforms. Those who garner growing audiences will benefit from the fact that dollars follow eyeballs, but others may not see worthwhile returns on investment.

Sales Growth

A company’s long-term performance can give signals about its business quality. Any business can put up a good quarter or two, but many enduring ones muster years of growth. News Corp's revenue was flat over the last 5 years.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Just like its 5-year revenue trend, News Corp's revenue over the last 2 years has been flat, suggesting the company is in a slump.

This quarter, News Corp reported reasonable year-on-year revenue growth of 2.6%, and its $2.59 billion of revenue topped Wall Street's estimates by 0.9%. Looking ahead, Wall Street expects sales to grow 3.5% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, News Corp has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 4.9%, subpar for a consumer discretionary business.

News Corp's free cash flow came in at $326 million in Q2, equivalent to a 12.6% margin. This result was great for the business as it flipped from cash flow negative in the same quarter last year to positive this quarter.

Key Takeaways from News Corp's Q2 Results

We were impressed by how significantly News Corp blew past analysts' EPS expectations this quarter, driven by a convincing beat on the EBITDA line. We were also happy its revenue narrowly outperformed Wall Street's estimates. On the other hand, free cash flow missed. Zooming out, we think this was a solid quarter that should have shareholders cheering. The stock is flat after reporting and currently trades at $24.27 per share.

News Corp may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.