Is Now The Time To Put Intercede Group (LON:IGP) On Your Watchlist?

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Intercede Group (LON:IGP). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

View our latest analysis for Intercede Group

How Quickly Is Intercede Group Increasing Earnings Per Share?

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. That means EPS growth is considered a real positive by most successful long-term investors. Over the last three years, Intercede Group has grown EPS by 4.3% per year. While that sort of growth rate isn't anything to write home about, it does show the business is growing.

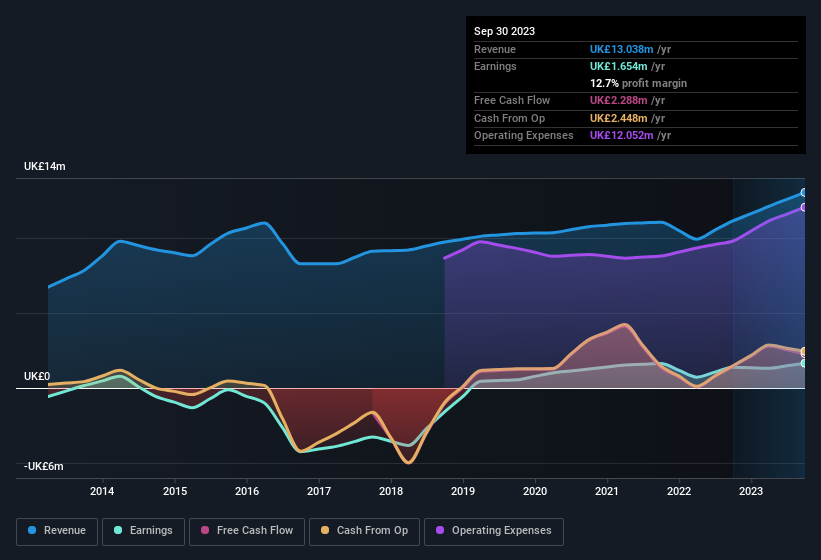

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. EBIT margins for Intercede Group remained fairly unchanged over the last year, however the company should be pleased to report its revenue growth for the period of 17% to UK£13m. That's encouraging news for the company!

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

Intercede Group isn't a huge company, given its market capitalisation of UK£60m. That makes it extra important to check on its balance sheet strength.

Are Intercede Group Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Any way you look at it Intercede Group shareholders can gain quiet confidence from the fact that insiders shelled out UK£168k to buy stock, over the last year. And when you consider that there was no insider selling, you can understand why shareholders might believe that there are brighter days ahead. We also note that it was the Non-Executive Chairman, Royston Hoggarth, who made the biggest single acquisition, paying UK£70k for shares at about UK£0.70 each.

Is Intercede Group Worth Keeping An Eye On?

As previously touched on, Intercede Group is a growing business, which is encouraging. It's not easy for business to grow EPS, but Intercede Group has shown the strengths to do just that. The cherry on top is the insider share purchases, which provide an extra impetus to keep and eye on this stock, at the very least. You should always think about risks though. Case in point, we've spotted 3 warning signs for Intercede Group you should be aware of, and 1 of them makes us a bit uncomfortable.

The good news is that Intercede Group is not the only growth stock with insider buying. Here's a list of growth-focused companies in GB with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.