Nu Skin (NUS) Up 6% in a Month: Can It Maintain Momentum?

Nu Skin Enterprises, Inc. NUS, which was in the red zone for quite some time, has seen its shares gain nearly 6% in the past month, outperforming the industry’s growth of 2.2%. The turnaround can be attributable to the company’s solid first-quarter 2019 results, which reflect its constant focus on expanding customer base.

However, Nu Skin continued to battle currency headwinds, which are expected to persist in and weigh on the second-quarter performance. So let’s delve deeper and see if the Zacks Rank #3 (Hold) company can sustain the momentum on the back of its efforts.

Factors Driving Nu Skin

Nu Skin is focused on capturing greater market share and maintaining momentum. In fact, the company’s long-term strategies stand on three key pillars — Products, Programs and Platforms. To this end, the launch of ageLOC LumiSpa has been a success, which is expected to be a growth driver in 2019. Apart from product launches, Nu Skin’s well-knit product strategies have been driving growth in several markets. It has also been working toward expanding sales compensation program, Velocity, across different nations. Management expects Velocity to play a significant role in expanding the company’s business in the future.

Further, Nu Skin operates through a wide network of sales leaders and customers. Notably, the company’s top line has been consistently benefiting from growth in consumer count. In the first quarter of 2019, Nu Skin’s customer base increased 10% to 1,193,206. This followed respective increases of 16%, 9%, 8% and 7% in the fourth, third, second and first quarters of 2018. The company relies much on social media along with well-knit product and marketing programs to widen customer reach.

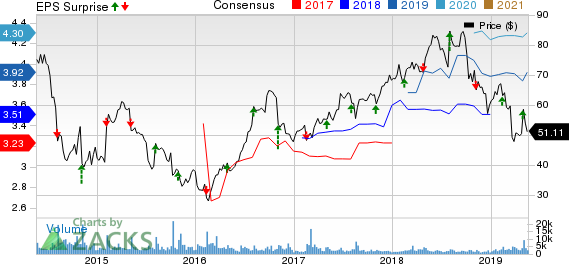

Nu Skin Enterprises, Inc. Price, Consensus and EPS Surprise

Nu Skin Enterprises, Inc. price-consensus-eps-surprise-chart | Nu Skin Enterprises, Inc. Quote

In the first quarter, Nu Skin not only reported better-than-expected numbers but also recorded year-over-year growth in top and bottom lines. This was the second straight quarter of positive earnings surprise and the fifth successive quarter of revenue beat. Results gained from robust performance across most regional segments and enhanced gross margin. The quarter also gained from sustained growth in the customer base, courtesy of effective strategies to widen market reach. Further, the solid performance can be attributed to the company’s technology and business expansion initiatives, customer acquisition, and retention program.

Can Growth Sustain Amid Hurdles?

Nu Skin’s top and bottom lines in the first quarter of 2019 were considerably hurt by foreign currency headwinds. In fact, revenue growth was hit by approximately 6% due to currency headwinds. Moreover, management expects foreign currency fluctuations to negatively impact the company’s top line in the second quarter and 2019 by 4-5% and 2-3%, respectively.

For the second quarter, management anticipates revenues of $660-$680 million, indicating 3-6% decline from the figure reported in the year-ago period. This includes an expected 4-5% negative foreign currency impact. Also, the company highlighted that revenues in the prior-year quarter gained from the introduction of LumiSpa in Mainland China, which generated sales of approximately $95 million, consequently making the year-over-year comparison a bit challenging. Moreover, management pointed out that major product initiatives in this year are slated for the second half.

Nonetheless, focus on expansion of global beauty device systems with product introductions and line extensions, coupled with optimization of Velocity sales compensation program, bodes well. For 2019, management anticipates revenues of $2.76-$2.81 billion, implying 3-5% growth from the figure reported in 2018. Additionally, the company envisions earnings of $3.80-$4.05 per share, up from $3.52 reported in 2018.

3 Cosmetic Stocks You Can’t Miss

Avon Products AVP has long-term earnings per share growth rate of 7.5% and a Zacks Rank #1 (Strong Buy). You can see the completelist of today’s Zacks #1 Rank stocks here.

Estee Lauder EL has a Zacks Rank #2 (Buy) and long-term earnings per share growth rate of 13%.

Helen of Troy HELE has a Zacks Rank #2 and long-term earnings per share growth rate of 5.6%.

This Could Be the Fastest Way to Grow Wealth in 2019

Research indicates one sector is poised to deliver a crop of the best-performing stocks you'll find anywhere in the market. Breaking news in this space frequently creates quick double- and triple-digit profit opportunities.

These companies are changing the world – and owning their stocks could transform your portfolio in 2019 and beyond. Recent trades from this sector have generated +98%, +119% and +164% gains in as little as 1 month.

Click here to see these breakthrough stocks now >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Nu Skin Enterprises, Inc. (NUS) : Free Stock Analysis Report

Helen of Troy Limited (HELE) : Free Stock Analysis Report

The Estee Lauder Companies Inc. (EL) : Free Stock Analysis Report

Avon Products, Inc. (AVP) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research