Ollie's (NASDAQ:OLLI) Posts Q4 Sales In Line With Estimates, Guidance Disappoints

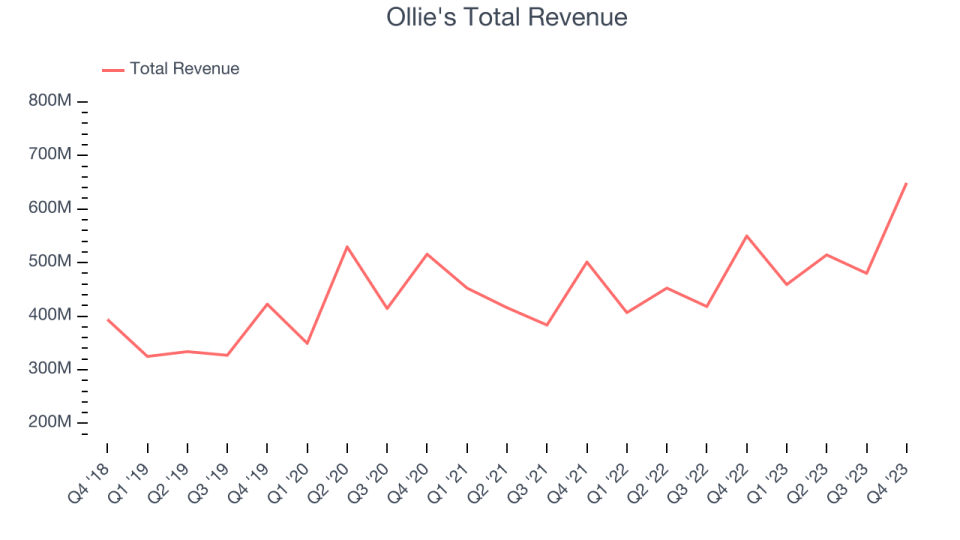

Discount retail company Ollie’s Bargain Outlet (NASDAQ:OLLI) reported results in line with analysts' expectations in Q4 CY2023, with revenue up 18% year on year to $648.9 million. On the other hand, the company's full-year revenue guidance of $2.26 billion at the midpoint came in 1.5% below analysts' estimates. It made a non-GAAP profit of $1.23 per share, improving from its profit of $0.84 per share in the same quarter last year.

Is now the time to buy Ollie's? Find out by accessing our full research report, it's free.

Ollie's (OLLI) Q4 CY2023 Highlights:

Revenue: $648.9 million vs analyst estimates of $649.2 million (small miss)

EPS (non-GAAP): $1.23 vs analyst estimates of $1.16 (6% beat)

Management's revenue guidance for the upcoming financial year 2024 is $2.26 billion at the midpoint, missing analyst estimates by 1.5% and implying 7.5% growth (vs 14.9% in FY2023) (EPS guidance for the same period was also below expectations)

Gross Margin (GAAP): 40.5%, up from 37.6% in the same quarter last year

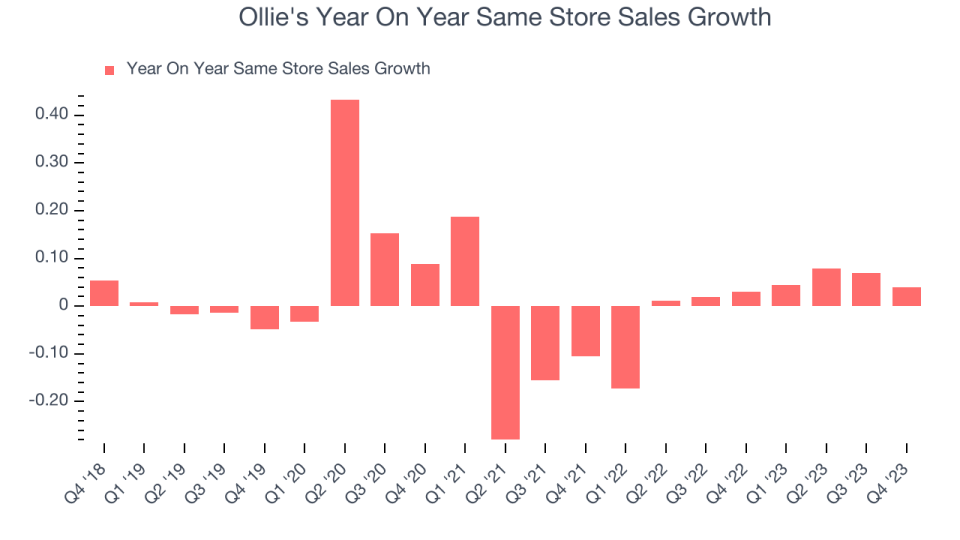

Same-Store Sales were up 3.9% year on year (beat vs. expectations of up 3.3% year on year)

Store Locations: 512 at quarter end, increasing by 44 over the last 12 months

Market Capitalization: $4.64 billion

“Our record fourth quarter capped off a great year for Ollie’s. For the full fiscal year 2023, we generated record revenues, increased gross margin 370 basis points, and grew adjusted earnings per share by 80%. In addition to our strong financial performance, we also opened our 500th store, entered our 30th state, added a record 3.6 million new Ollie’s Army members, and returned to a pattern of consistent execution and growth,” said John Swygert, President and Chief Executive Officer.

Often located in suburban or semi-rural shopping centers, Ollie’s Bargain Outlet (NASDAQ:OLLI) is a discount retailer that acquires excess inventory then sells at meaningful discounts.

Discount General Merchandise Retailer

Broadline discount retailers understand that many shoppers love a good deal, and they focus on providing excellent value to shoppers by selling general merchandise at major discounts. They can do this because of unique purchasing, procurement, and pricing strategies that involve scouring the market for trendy goods or buying excess inventory from manufacturers and other retailers. They then turn around and sell these snacks, paper towels, toys, and myriad other products at highly enticing prices. Despite the unique draw and lure of discounts, these discount retailers must also contend with the secular headwinds of online shopping and challenged retail foot traffic in places like suburban strip malls.

Sales Growth

Ollie's is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale.

As you can see below, the company's annualized revenue growth rate of 10.5% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was decent as it opened new stores and grew sales at existing, established stores.

This quarter, Ollie's revenue grew 18% year on year to $648.9 million, falling short of Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 9.4% over the next 12 months, a deceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Same-Store Sales

A company's same-store sales growth shows the year-on-year change in sales for its brick-and-mortar stores that have been open for at least a year, give or take, and e-commerce platform. This is a key performance indicator for retailers because it measures organic growth and demand.

Ollie's demand within its existing stores has been relatively stable over the last eight quarters but fallen behind the broader consumer retail sector. On average, the company's same-store sales have grown by 1.5% year on year. With positive same-store sales growth amid an increasing physical footprint of stores, Ollie's is reaching more customers and growing sales.

In the latest quarter, Ollie's same-store sales rose 3.9% year on year. This performance was more or less in line with the same quarter last year.

Key Takeaways from Ollie's Q4 Results

While same store sales and EPS outperformed Wall Street's estimates, revenue missed and full-year guidance for both sales and earnings were below Wall Street's estimates. Overall, this was a mediocre quarter for Ollie's. The company is down 4.1% on the results and currently trades at $72.3 per share.

So should you invest in Ollie's right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.