Omnicell (OMCL) Gains From Innovation Amid Cost Pressure

Omnicell OMCL is gaining from its recent acquisitions, expansion of advanced services solutions and prudent cost management. Persistent inflationary pressures pose a threat to the company’s cost-saving actions. The stock carries a Zacks Rank #3 (Hold) at present.

Omnicell is progressing well with its three-legged strategy that covers market expansion through the delivery of differentiated, innovative solutions, expansion into new markets, primarily outside the United States, and expansion through strategic partnerships and the acquisition of new technologies.

In this line, the company earlier expanded its autonomous pharmacy portfolio with the strategic and accretive acquisition of PSG's 340B Link business, now called Omnicell 340B. Notably, 340B is a significant part of an increasingly complex pharmacy supply chain, requiring solutions designed to help providers manage compliance and reporting while capturing drug cost savings.

Omnicell has also accelerated a shift to cloud-based solutions and tech-enabled services through the launches of Inventory Optimization Service (formerly Omnicell One) and Central Pharmacy Dispensing Services. In the third quarter of 2023, several of the company’s health system partners extended their sole-source agreements, including a Florida-based health system that plans to replace its existing point-of-care footprint with Omnicell XT systems. One of Georgia's largest healthcare networks has contracted for OMCL’s inventory optimization service to help strengthen its pharmacy supply chain.

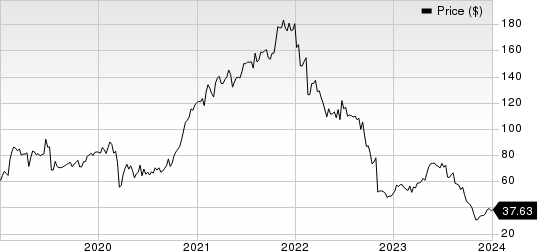

Omnicell, Inc. Price

Omnicell, Inc. price | Omnicell, Inc. Quote

Earlier in 2023, a major southern health system customer expanded the service to nearly 20 hospitals across its health system for increased digitization, visibility and insights. Omnicell’s recently-acquired ReCept has been rebranded as Omnicell specialty pharmacy services and was introduced to the market in late 2022. The company plans to focus on integrating customer success functions into its broader organizational structure.

In terms of its 2025 financial roadmap, Omnicell is targeting to reach 1.9 billion to 2 billion of revenue by 2025 — a 14% to 15% compounded total annual revenue growth rate from 2021 to 2025. Over the same period of time, it is also targeting an expansion of non-GAAP EBITDA margin from 21% in 2021 to 25% by 2025, representing a margin expansion of approximately 400 basis points (bps).

The company is well-positioned to deliver on the 2025 total revenue growth targets, driven by factors like growing its tech services revenues, benefits from long-term sole source customer partnerships, multi-year co-development plans and increased average deal sizes.

For the full year of 2022, the company delivered a non-GAAP EBITDA of $193 million, which was above the previous guidance range of $177-$183 million, as announced during the third quarter of 2022 earnings call. In the third quarter, both non-GAAP EBITDA and non-GAAP earnings per share exceeded the pre-announced guidance, led by strong cost management.

On the flip side, similar to its healthcare system partners, the company’s operations continue to be affected by persisting labor shortages as well as increased inflationary costs related to components’ raw materials and freight.

In the third quarter of 2023, gross profit declined 17.1%, resulting in a year-over-year contraction in the gross margin of 152 basis points. The operating profit also decreased 79.9% compared with the third quarter of 2022. For full-year 2023, management anticipates the cost-savings measures to be partially offset by year-over-year increases in compensation and vendor price increases.

Omnicell’s operations are subjected to continued and increased competition from current and future competitors in the medication management automation solutions market and the medication adherence solutions market, including price competition, industry and competitor consolidation, competitor brand recognition and in terms of relationships with the suppliers and current and potential customers. This increased competition could result in pricing pressure and a reduced margin, which would have an adverse impact on the company’s performance.

Over the past year, shares of OMCL declined 25.4% against the industry’s 26.5% growth.

Key Picks

Some better-ranked stocks in the broader medical space are Insulet PODD, Haemonetics HAE and DexCom DXCM. While Insulet sports a Zacks Rank #1 (Strong Buy), Haemonetics and DexCom carry a Zacks Rank #2 (Buy) each at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Estimates for Insulet’s 2023 earnings per share have remained constant at $1.91 in the past 30 days. Shares of the company have dropped 26.3% in the past year against the industry’s rise of 3.7%.

PODD’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 105.1%. In the last reported quarter, it delivered an average earnings surprise of 77.4%.

Shares of Haemoneticshave gained 8.7% in the past year. Earnings estimates for Haemoneticshave remained constant at $3.89 in 2023 and at $4.15 in 2024 in the past 30 days.

HAE’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 16.1%. In the last reported quarter, it posted an earnings surprise of 5.3%.

Estimates for DexCom’s 2023 earnings per share have increased from $1.43 to $1.44 in the past 30 days. Shares of the company have gained 9.6% in the past year compared with the industry’s 3.8% rise.

DXCM’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 36.4%. In the last reported quarter, it delivered an average earnings surprise of 47.1%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Omnicell, Inc. (OMCL) : Free Stock Analysis Report

Haemonetics Corporation (HAE) : Free Stock Analysis Report

DexCom, Inc. (DXCM) : Free Stock Analysis Report

Insulet Corporation (PODD) : Free Stock Analysis Report