Omnicom's (OMC) Q3 Earnings Beat Estimates, Increase Y/Y

Omnicom Group Inc. OMC reported impressive third-quarter 2023 results, wherein both earnings and revenues beat the Zacks Consensus Estimate.

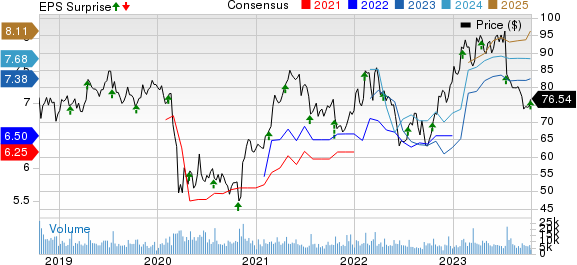

Earnings of $1.86 per share beat the consensus estimate by 0.5% and increased 5.1% year over year. Total revenues of $3.6 billion surpassed the consensus estimate by 0.3% and increased 3.9% year over year.

The increase in the top line resulted from an increase of 3.3% in revenues from organic growth and 1.7% due to foreign currency translations, partially offset by a 1.1% fall in acquisition revenues, net of disposition revenues.

Omnicom shares have gained 10.9% over the past year compared with the 0.3% rise of the industry it belongs to and the 19.8% rally of the Zacks S&P 500 composite.

Omnicom Group Inc. Price, Consensus and EPS Surprise

Omnicom Group Inc. price-consensus-eps-surprise-chart | Omnicom Group Inc. Quote

Organic Growth Across Disciplines and Regions

Across fundamental disciplines, revenues from Advertising & Media were up 6.1% compared with our estimated growth of 5.5%. Precision marketing revenues jumped 4.3% compared with our estimate of 9.3% growth. Experiential revenues improved 9.2%, in line with our expectations.

Public Relations revenues decreased 5.5% against our estimation of 7.8% growth. Healthcare revenues increased 3.8%, organically, year over year compared with our estimated growth of 4.8%. Commerce and Brand Consulting revenues were down 1.7% against our estimated growth of 6%. Execution and support declined 3.6% against our estimated growth of 0.2%.

Across regional markets, year-over-year organic revenue growth was 2.7% in the United States, 4.4% in the U.K., 5.7% in Euro Markets & Other Europe, 19.2% in Latin America and 2.5% in Asia Pacific. Middle East & Africa and Other North America revenues declined 10.8% and 1.7%, respectively.

Margin Performance

EBITA in the quarter came in at $581.1 million, up 2.6% year over year. EBITA margin was 16.2%, down 20 basis points (bps) year over year. Operating profit of $560.8 million increased 2.7% year over year. The operating margin decreased 20 bps to 15.3%.

2023 View

The company expects organic growth to be between 3.5% and 5%. It expects operating margin to be at the top of the 15-15.4% range.

Zacks Rank and Stocks to Consider

Omnicom currently carries a Zacks Rank #3 (Hold).

Investors interested in the Zacks Business Services sector can consider the following better-ranked stocks.

Automatic Data ADP currently has a Zacks Rank of 2 (Buy). It outpaced the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 3.1%. The consensus estimate for fiscal 2023 revenues and earnings implies growth of 6.3% and 11.1%, respectively. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Broadridge BR currently carries a Zacks Rank of 2. It surpassed the Zacks Consensus Estimate in two of the trailing four quarters, missed once and matched on one instance, the average surprise being 0.5%. The consensus estimates for fiscal 2024 revenues and earnings suggest growth of 7.2% and 8.8%, respectively.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Broadridge Financial Solutions, Inc. (BR) : Free Stock Analysis Report

Automatic Data Processing, Inc. (ADP) : Free Stock Analysis Report

Omnicom Group Inc. (OMC) : Free Stock Analysis Report