Organic Growth Supports Comerica (CMA), High Expenses Hurt

Comerica Incorporated’s CMA top-line growth has been supported by high rates, increasing net interest income (NII) and a rise in loan balances. Also, decent liquidity ensures sustainable capital distributions. However, escalating expenses and concentrated commercial loan portfolio are major headwinds.

CMA’s income-generation capability has been aided by loan growth over the years. Given the strength in its loan pipeline, the loan balances are expected to improve in the near term. Management estimates average loans to grow 7% in 2023.

Such a rise in loan balances has improved Comerica’s NII over the years, thus aiding its top-line growth. With expectations of Federal Reserve keeping interest rates high in the near term, NII and net interest margin are likely to continue witnessing growth, while a rise in funding costs will weigh on both. The company projects NII to rise 1-2% in 2023.

CMA’s focus on improving operational efficiency led to the introduction of GEAR Up initiatives in mid-2016, which resulted in an improvement in efficiency ratio and return on equity. Also, its efforts in product enhancements, improvement in sales tools and training as well as improved customer analytics bode well for robust revenue growth.

Comerica has a solid liquidity profile given its decent cash levels and $20.3 billion capacity remaining in its discount window compared with the company’s obligations. Hence, capital distributions seem sustainable. This is likely to stoke investors’ confidence in the stock.

However, a rising cost base remains a concern for CMA. The company’s non-interest expenses have been rising over the years on an increase in salaries and benefits expenditure. Such rising costs are likely to hinder bottom-line growth in the upcoming period. Management forecasts expenses to rise 11% in 2023.

Comerica has substantial exposure to commercial and commercial mortgage loans. As of Sep 30, 2023, the company’s exposure to such loans was 80% of total loans. Commercial lending may be impacted by rapid changes in the current macroeconomic backdrop, hurting CMA’s financials if the economic situation worsens.

Also, Comerica has a significant business exposure in California and Michigan where the economic environment has been increasingly challenging over the past few years. Such geographic concentration makes the company vulnerable to potential economic doldrums in the region.

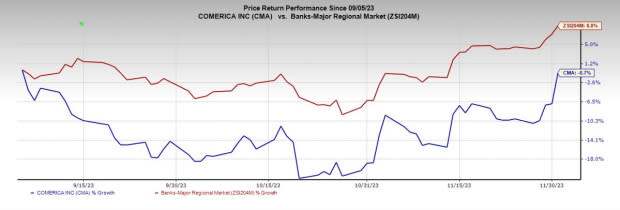

Shares of this Zacks Rank #3 (Hold) bank have lost 0.7% in the past three months against the industry’s growth of 8.8%.

Image Source: Zacks Investment Research

Bank Stocks Worth a Look

A couple of better-ranked stocks from the banking space are JPMorgan Chase & Co. JPM and Park National Corporation PRK. Each stock currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

JPM’s earnings estimate for 2023 has been revised 4.9% upward over the past 60 days. In the past three months, its shares have increased 8%.

The Zacks Consensus Estimate for PRK’s current-year earnings has been revised 6.2% upward over the past 30 days. Its shares have gained 15.7% in the past three months.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

JPMorgan Chase & Co. (JPM) : Free Stock Analysis Report

Comerica Incorporated (CMA) : Free Stock Analysis Report

Park National Corporation (PRK) : Free Stock Analysis Report