Organon's Valuation Is Not Expensive

Organon & Co. (NYSE:OGN), one of the largest pharmaceutical companies in the world, formed as a result of a spin-off from Merck (NYSE:MRK) and specializes in the development and commercialization of drugs aimed at preventing pregnancy and combating various women's health issues, cardiovascular diseases, inflammatory autoimmune diseases and respiratory diseases.

Investment thesis

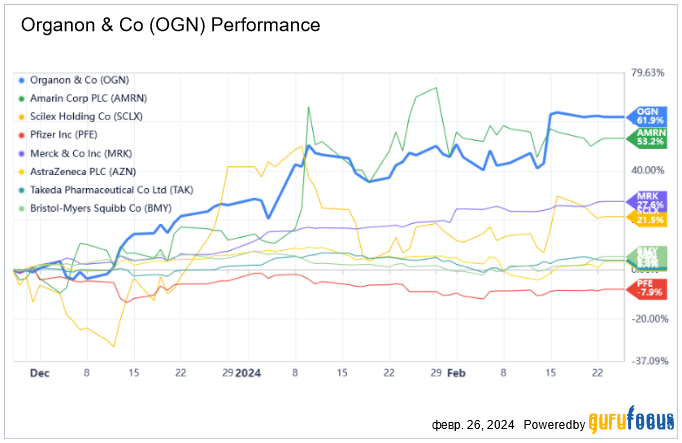

On Feb. 15, the company released fourth-quarter 2023 financial results that exceeded our expectations, causing its share price to rise 13%.

Its earnings per share came in at 88 cents, up 8.60% year over year, primarily due to higher sales of biosimilars. The biosimilar franchise's revenue totaled $199 million for the three months ended Dec. 31, up 48.50% from the fourth quarter of 2022.

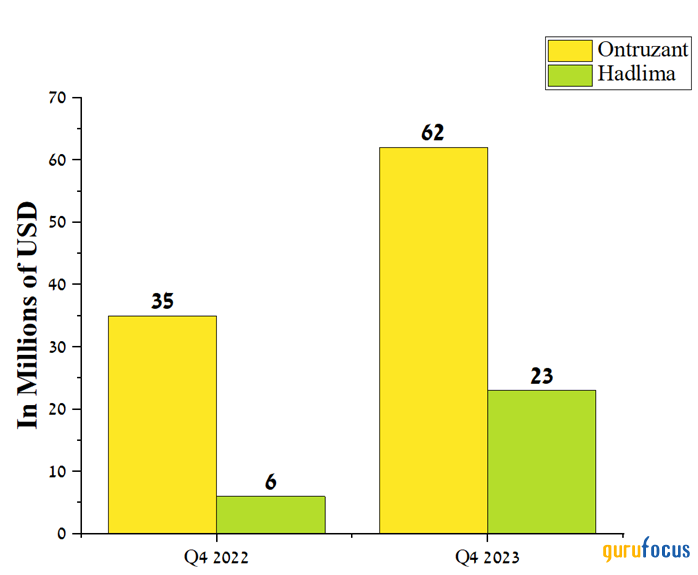

So, sales of Ontruzant (trastuzumab-dttb), which is a biosimilar to Herceptin, were $62 million, while sales of Hadlima were $23 million, a significant increase year over year due to its launch in the United States on July 1.

Source: Author's elaboration, based on quarterly securities reports.

Hadlima (adalimumab-bwwd) is biosimilar to AbbVie's (NYSE:ABBV) Humira, which was developed in partnership with Samsung Bioepis and whose demand continues to snowball despite increased competition in the global autoimmune disease therapeutics market.

Source: Organon

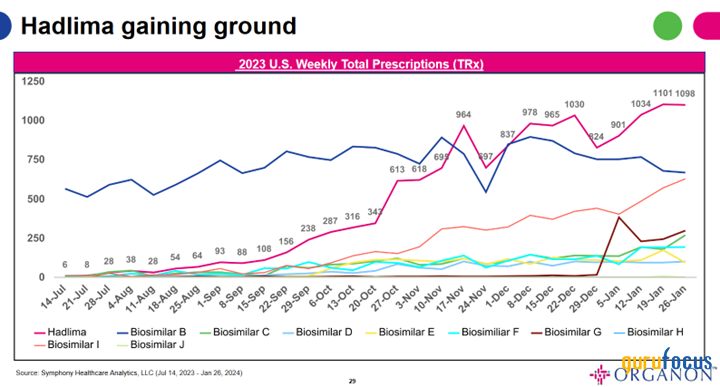

Moreover, on Feb. 20, the company announced the U.S. Department of Veterans Affairs had selected Hadlima to replace Humira. We believe this event will not only increase demand for one of the company's key products, but will also contribute to an increase in its free cash flow in the first half of this year.

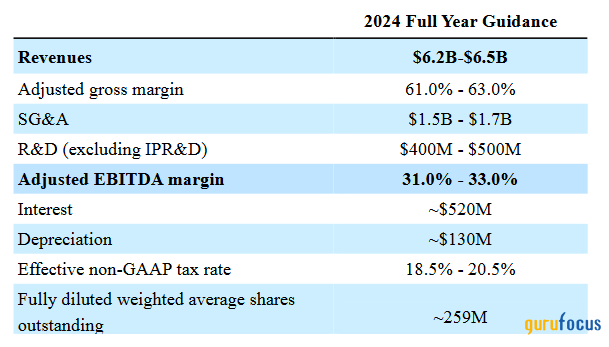

Organon also revealed financial guidance for 2024, which exceeded analysts' consensus expectations. So its revenue is expected to range from $6.20 billion to $6.50 billion. At the same time, its gross margin will be 61% to 63%, which is higher than that of Teva Pharmaceutical (NYSE:TEVA) and Viatris (NASDAQ:VTRS), which also focus on developing biosimilars.

Source: Organon

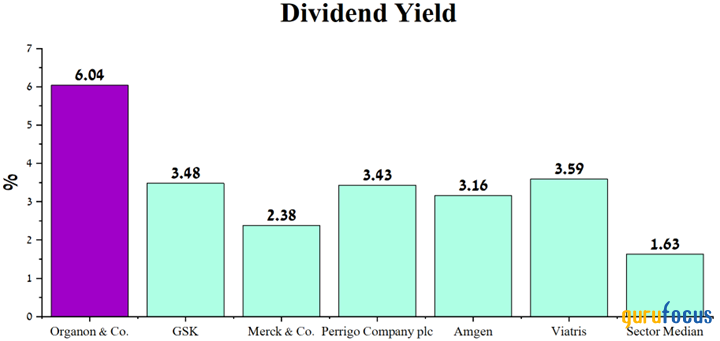

An additional investment thesis we highlight is Organon's dividend yield, which is around 6%, significantly higher than the health care sector's median and higher than U.S. inflation.

Source: Author's elaboration, based on GuruFocus data.

We initiate our coverage of Organon with an outperform rating for the next 12 months.

Organon's fourth-quarter financial results and outlook for 2024

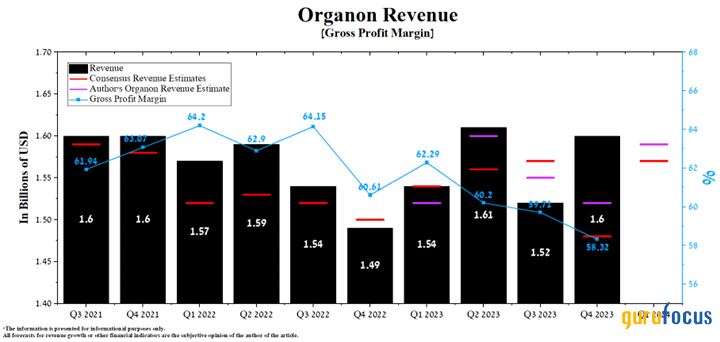

Organon's revenue for the fourth quarter of 2023 was about $1.6 billion, exceeding our expectations by about $80 million and, importantly, growing 7.40% year over year.

As a result, its trailing 12-month price-sales ratio was 0.75, which is not only 25.80% lower than the average over the past five years but also significantly lower than its crucial health care rivals such as Merck, Pfizer (NYSE:PFE) and AstraZeneca (NASDAQ:AZN). As a result, this is one of the factors indicating the company continues to remain undervalued by investors and traders despite the enormous progress made by its management aimed at returning Organon to the path of growth and prosperity after its spinoff from Merck.

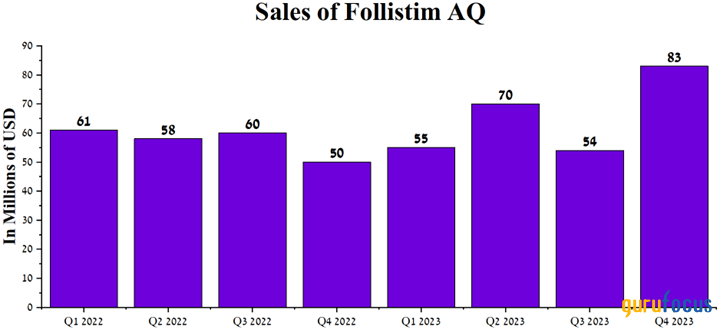

In addition to the company's biosimilar franchise, one of its key medicines is Follistim AQ (follitropin beta injection), which has been approved by regulatory authorities worldwide for the treatment of infertility. Its mechanism of action is based on the induction of phosphorylation and also leads to the activation of the PI3K signaling pathway, which ultimately helps stimulate sperm production in men, while when taken by women, there is a significant stimulation of follicle development.

Follistim sales were $83 million for the three months ended Dec. 31, 2023, up 66% year over year due to increased demand in the U.S. as well as the return of fertility patients to clinics in China as restrictions related to the Covid-19 pandemic eased.

Source: Author's elaboration, based on quarterly securities reports.

The American pharmaceutical company is expected to release financial results for the first quarter of 2024 on May 3. Organon's revenue for the quarter is anticipated to be in the range of $1.53 billion to $1.61 billion, up 6.10% from analysts' expectations for the previous quarter.

Source: Author's elaboration, based on GuruFocus data.

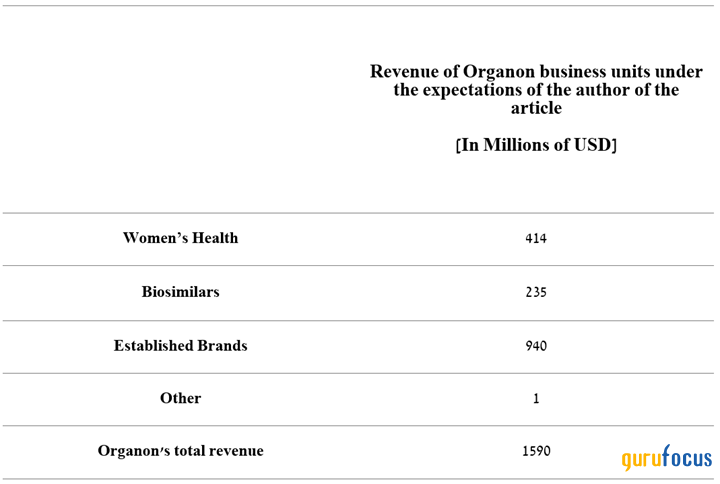

At the same time, under our model, Organon's total revenue will be $20 million above the median of this range and reach $1.59 billion. The company's year-over-year revenue growth will be driven primarily by increased demand for its women's health products as well as double-digit growth in sales of its biosimilars Atozet, Singulair and Nasonex.

Source: Created by author.

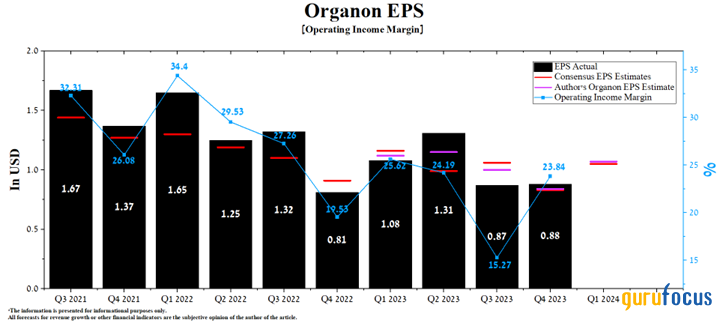

Organon's operating income margin was 23.84% in the fourth quarter, up 4.31% year over year as sales of some of its key products recovered despite increased competition in the global cardiovascular drugs market.

We estimate this financial indicator will increase to 24.60% in 2024, primarily due to sales of its biosimilar franchise, lower costs of raw materials needed to produce its medications, optimization of its administrative and general expenses and expansion of its drug portfolio.

On Nov. 7, Organon announced the Food and Drug Administration accepted its supplemental biologics license application for the interchangeability designation for Hadlima, which is a biosimilar of Humira. We expect the FDA to approve Hadlima's label expansion, which will be critical for continued sales growth as pharmacists will be able to prescribe this adalimumab biosimilar instead of Humira without consulting a prescriber.

Organon's earnings per share for the first quarter of 2023 is expected to be in the range of 90 cents to $1.17. In contrast, we expect earnings to be higher at $1.07, down only marginally from the prior year.

Source: Author's elaboration, based on GuruFocus data.

Furthermore, Organon's trailing 12-month non-GAAP price-earnings ratio is 4.47, 76.4% lower than the sector average. Moreover, the forward non-GAAP price-earnings ratio is 4.30, which is one of the factors indicating the company is significantly undervalued by financial market participants, even despite the high growth rate of revenue in its biosimilar portfolio, improved margins in recent quarters and the development of product candidates that have blockbuster potential.

More globally, Organon's operating profit growth is expected to push its price-earnings ratio down to 3.70 by 2027, which we estimate is an attractive value for long-term investors.

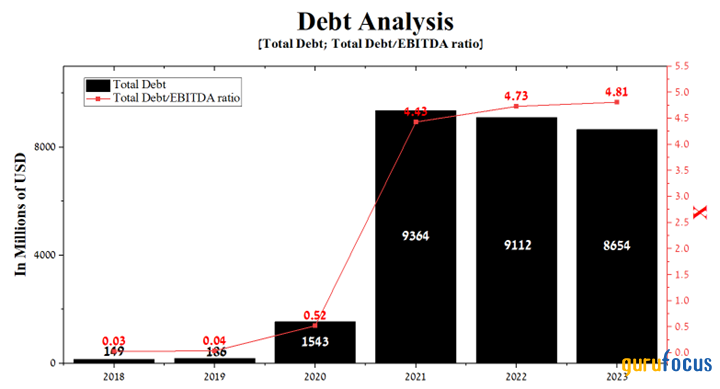

On the other hand, it is equally important to discuss the company's debt, which has remained at extremely high levels over the past three years. So its total debt amounted to $8.65 billion at the end of 2023, decreasing by $458 million compared to the previous year.

However, due to the fall in Ebitda, the total debt/Ebitda ratio continues to grow at a low pace and amounts to about 4.81 as of Dec. 31. As a result, we believe that maintaining this multiple above 3 discourages some conservative investors from considering Organon as a long-term investment.

Source: Author's elaboration, based on GuruFocus data.

However, we do not expect the company's management to have difficulty servicing its debt in the coming quarters, mainly due to its stable cash flow. Nevertheless, the need to repay notes with a maturity date of 2028 to 2031 limits the company's ability to increase dividend payments or authorize a share repurchase program.

Conclusion

Despite a slight year-over-year decline in Nexplanon/Implanon NXT sales, higher U.S. inflation relative to Wall Street expectations and more points of Biden's Inflation Reduction Act taking effect, Organon's share price has continued to rise in recent months.

We expect the bullish trend to continue into 2024, driven by solid growth in the company's biosimilar sales, an extremely high dividend yield of over 6%, a continued trend of improving margins and relatively low multiples, indicating it is trading at a significant discount to its health care peers.

We initiate our coverage of Organon with an outperform rating for the next 12 months.

This article first appeared on GuruFocus.