Is OTAQ (LON:OTAQ) Using Too Much Debt?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies OTAQ plc (LON:OTAQ) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for OTAQ

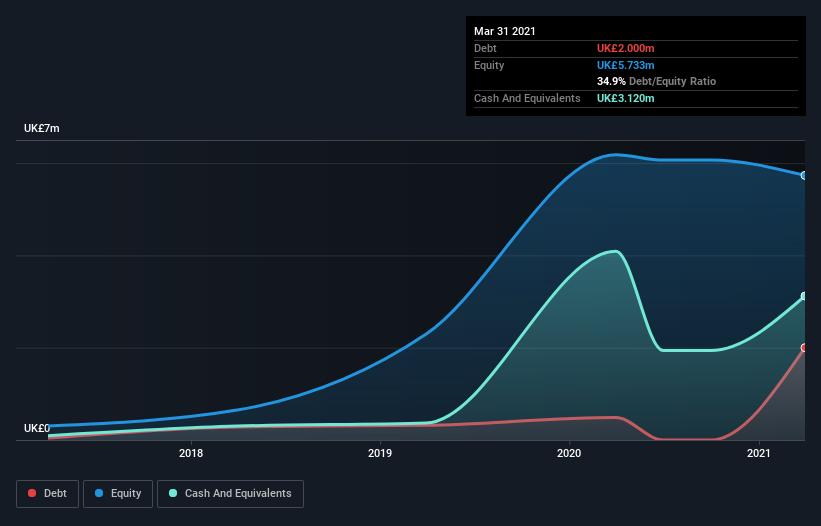

What Is OTAQ's Net Debt?

As you can see below, at the end of March 2021, OTAQ had UK£2.00m of debt, up from UK£486.0k a year ago. Click the image for more detail. But on the other hand it also has UK£3.12m in cash, leading to a UK£1.12m net cash position.

How Strong Is OTAQ's Balance Sheet?

According to the last reported balance sheet, OTAQ had liabilities of UK£2.46m due within 12 months, and liabilities of UK£2.30m due beyond 12 months. Offsetting these obligations, it had cash of UK£3.12m as well as receivables valued at UK£939.0k due within 12 months. So its liabilities total UK£699.0k more than the combination of its cash and short-term receivables.

Of course, OTAQ has a market capitalization of UK£9.70m, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, OTAQ boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since OTAQ will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year OTAQ wasn't profitable at an EBIT level, but managed to grow its revenue by 19%, to UK£4.1m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is OTAQ?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year OTAQ had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of UK£1.6m and booked a UK£534k accounting loss. With only UK£1.12m on the balance sheet, it would appear that its going to need to raise capital again soon. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that OTAQ is showing 2 warning signs in our investment analysis , and 1 of those is concerning...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.