Oxford Industries (NYSE:OXM) Misses Q4 Revenue Estimates, Stock Drops

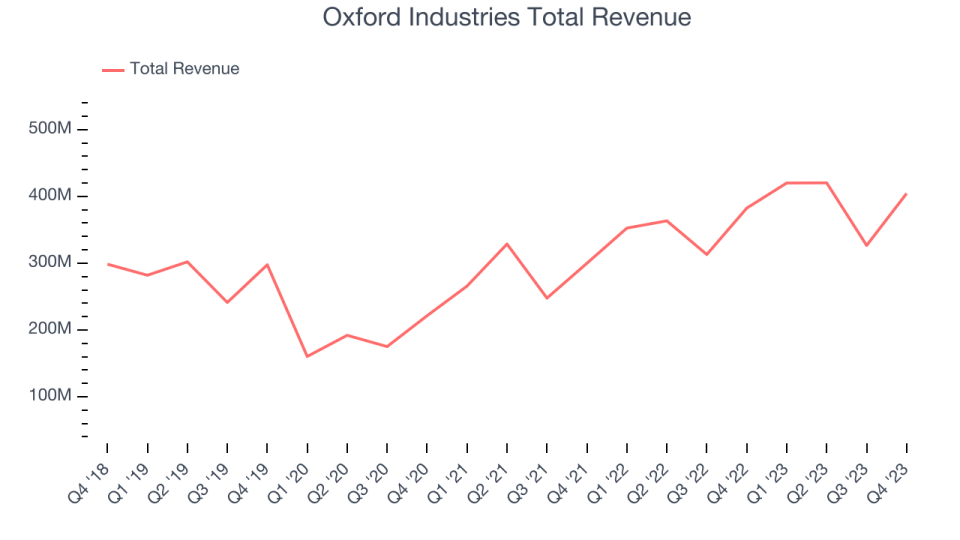

Fashion conglomerate Oxford Industries (NYSE:OXM) fell short of analysts' expectations in Q4 CY2023, with revenue up 5.7% year on year to $404.4 million. Next quarter's revenue guidance of $405 million also underwhelmed, coming in 2.1% below analysts' estimates. It made a non-GAAP profit of $1.90 per share, down from its profit of $2.28 per share in the same quarter last year.

Is now the time to buy Oxford Industries? Find out by accessing our full research report, it's free.

Oxford Industries (OXM) Q4 CY2023 Highlights:

Revenue: $404.4 million vs analyst estimates of $408.3 million (0.9% miss)

EPS (non-GAAP): $1.90 vs analyst expectations of $1.95 (2.4% miss)

Revenue Guidance for Q1 CY2024 is $405 million at the midpoint, below analyst estimates of $413.9 million

EPS (non-GAAP) Guidance for Q1 CY2024 is $2.70 at the midpoint, below analyst estimates of $3.48

Management's revenue guidance for the upcoming financial year 2024 is $1.65 billion at the midpoint, beating analyst estimates by 2.1% and implying 5% growth (vs 11.2% in FY2023)

Gross Margin (GAAP): 60.9%, up from 59.4% in the same quarter last year

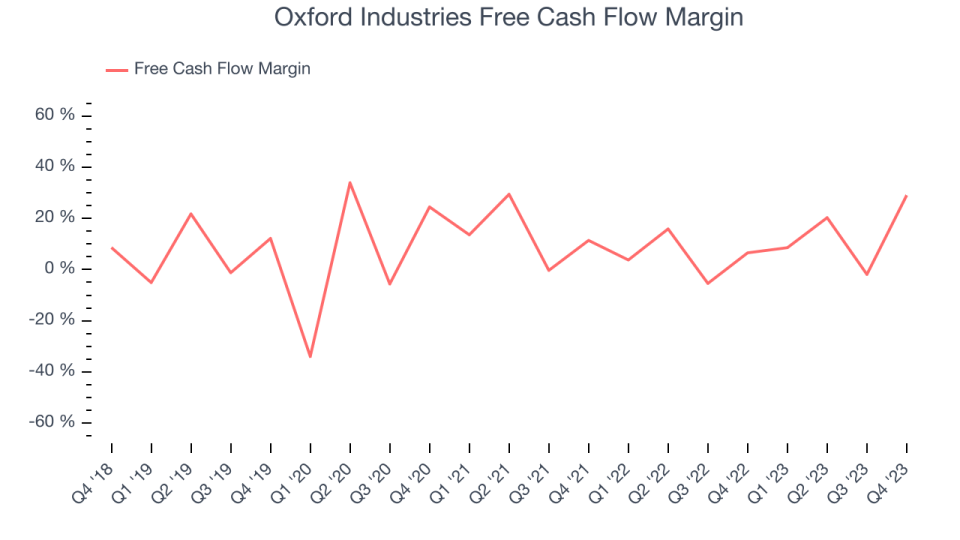

Free Cash Flow of $117.4 million is up from -$6.19 million in the previous quarter

Market Capitalization: $1.76 billion

Tom Chubb, Chairman and CEO, commented, “Fiscal 2023 was highlighted by the second strongest earnings year in our 82-year history and concluded a five-year period during which we delivered compound annual adjusted EPS growth exceeding 18 percent. This strong performance included generating $244 million in cash flow from operations in fiscal 2023, allowing us to invest in both organic growth and acquisitions, return capital to our shareholders via our quarterly dividend and opportunistic share repurchases, and pay down almost all our outstanding debt.

The parent company of Tommy Bahama, Oxford Industries (NYSE:OXM) is a lifestyle fashion conglomerate with brands that embody outdoor happiness.

Apparel, Accessories and Luxury Goods

Within apparel and accessories, not only do styles change more frequently today than decades past as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel, accessories, and luxury goods companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

A company's long-term performance can indicate its business quality. Any business can enjoy short-lived success, but best-in-class ones sustain growth over many years. Oxford Industries's annualized revenue growth rate of 7.2% over the last five years was weak for a consumer discretionary business.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Oxford Industries's annualized revenue growth of 17.3% over the last two years is above its five-year trend, suggesting some bright spots.

This quarter, Oxford Industries's revenue grew 5.7% year on year to $404.4 million, missing Wall Street's estimates. The company is guiding for a 3.6% year-on-year revenue decline next quarter to $405 million, a reversal from the 19.1% year-on-year increase it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 1.7% over the next 12 months, a deceleration from this quarter.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, Oxford Industries has shown decent cash profitability, giving it some reinvestment opportunities. The company's free cash flow margin has averaged 10.4%, slightly better than the broader consumer discretionary sector.

Oxford Industries's free cash flow came in at $117.4 million in Q4, equivalent to a 29% margin and up 369% year on year.

Key Takeaways from Oxford Industries's Q4 Results

Revenue and EPS missed this quarter. The company's earnings guidance for next quarter fell short of Wall Street's estimates. Overall, this was a weaker quarter for Oxford Industries. The company is down 6.6% on the results and currently trades at $105 per share.

Oxford Industries may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.