PENN Entertainment (NASDAQ:PENN) Reports Sales Below Analyst Estimates In Q4 Earnings

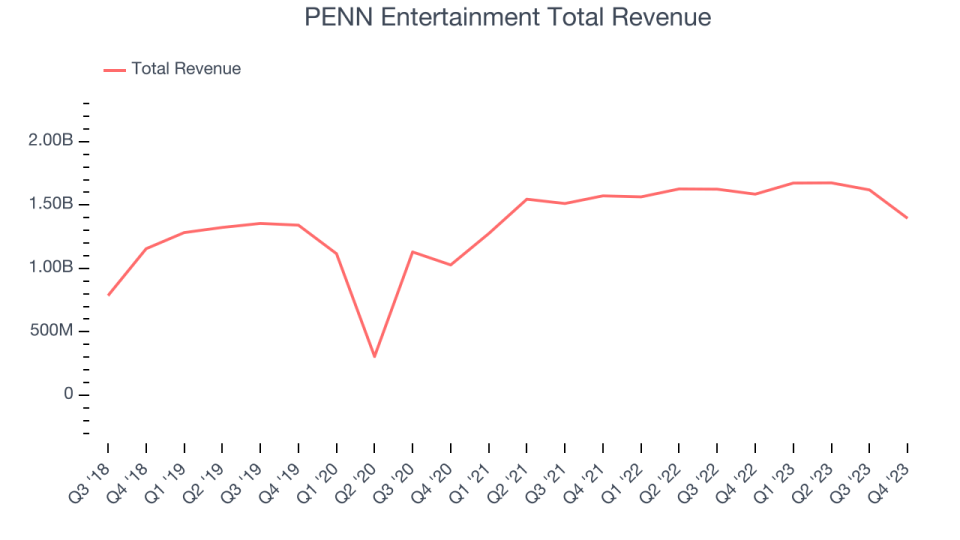

Casino, sports betting and entertainment operator PENN Entertainment (NASDAQ:PENN) fell short of analysts' expectations in Q4 FY2023, with revenue down 12% year on year to $1.40 billion. It made a GAAP loss of $2.37 per share, down from its profit of $0.13 per share in the same quarter last year.

Is now the time to buy PENN Entertainment? Find out by accessing our full research report, it's free.

PENN Entertainment (PENN) Q4 FY2023 Highlights:

Revenue: $1.40 billion vs analyst estimates of $1.53 billion (9% miss)

Adjusted EBITDAR: $112.5 million vs analyst estimates of $268.1 million (58% miss)

EPS: -$2.37 vs analyst estimates of -$0.53 (-$1.84 miss)

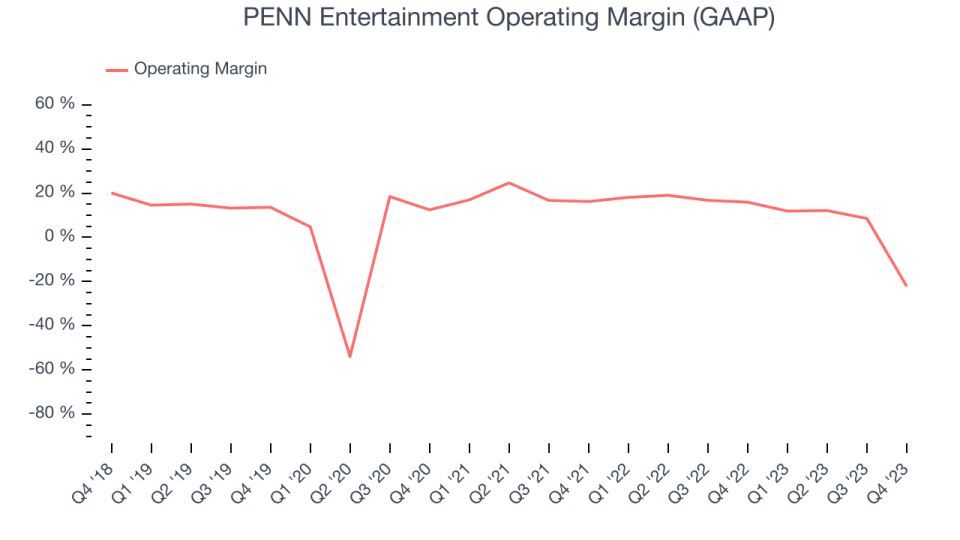

Gross Margin (GAAP): 22.7%, down from 58.1% in the same quarter last year

Market Capitalization: $3.36 billion

Jay Snowden, Chief Executive Officer and President, said: “PENN delivered another quarter of solid property level performance while continuing to invest in our high growth digital business, which we believe will create significant long term shareholder value. Our retail results reflect strong customer demand and well-executed strategies across our portfolio. In our Interactive segment, ESPN BET attracted significantly more first-time depositors (FTDs) than we anticipated, which drove higher than expected promotional expense. Our successful launch led to substantial expansion in key performance indicators (KPIs) including monthly active users (MAUs), handle, and cash handle. Importantly, strong early retention and consistent user acquisition have led to steady month-over-month increases in cash handle as our promotional expense has started to normalize entering 2024. ESPN BET has also attracted the mass market sports fan, highlighting the potential to expand the appeal of sports betting and grow the overall market. This foundation sets the stage for continued growth and market share gains as we introduce further product enhancements and deeper integrations into the ESPN media ecosystem.

Established in 1982, PENN Entertainment (NASDAQ:PENN) is a diversified American operator of casinos, sports betting, and entertainment venues.

Casinos and Gaming

Casino and gaming companies that offer slot machines, Texas Hold ‘Em, Blackjack and the like can enjoy limited competition because gambling is a highly regulated industry. These companies can also enjoy healthy margins and profits-have you ever heard the phrase ‘the house always wins’? Regulation cuts both ways, however, and casino and gaming companies may face stroke-of-the-pen risk that suddenly limits what they do or where they can do it. Furthermore, digitization is changing the game, pun intended. Whether it’s online poker or sports betting on your smartphone, innovation is forcing casino and gaming companies to adapt to keep up with changing consumer preferences such as being able to wager anywhere on demand.

Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. PENN Entertainment's annualized revenue growth rate of 9.2% over the last five years was weak for a consumer discretionary business.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. PENN Entertainment's recent history shows the business has slowed, as its annualized revenue growth of 3.8% over the last two years is below its five-year trend.

This quarter, PENN Entertainment missed Wall Street's estimates and reported a rather uninspiring 12% year-on-year revenue decline, generating $1.40 billion of revenue. Looking ahead, Wall Street expects sales to grow 4.8% over the next 12 months, an acceleration from this quarter.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

PENN Entertainment has done a decent job managing its expenses over the last eight quarters. The company has produced an average operating margin of 10.6%, higher than the broader consumer discretionary sector.

This quarter, PENN Entertainment generated an operating profit margin of negative 22.1%, down 38.1 percentage points year on year.

Over the next 12 months, Wall Street expects PENN Entertainment to become more profitable. Analysts are expecting the company’s LTM operating margin of 3.6% to rise to 7.2%.

Key Takeaways from PENN Entertainment's Q4 Results

We struggled to find many strong positives in these results. Its revenue unfortunately missed and its operating margin fell short of Wall Street's estimates. Overall, this was a mediocre quarter for PENN Entertainment. The company highlighted that it is excited about and continuing to invest in its digital business. The stock is down 3.9% on the results and currently trades at $21.61 per share.

PENN Entertainment may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.