Penumbra (PEN) Gains on New Launches Amid Currency Headwind

Penumbra PEN is gaining strength in the international markets on strong product uptake. Yet, unfavorable currency movement and rising expenses are major dampeners. The stock carries a Zacks Rank #3 (Hold).

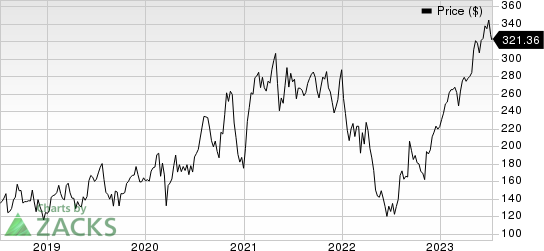

Penumbra has outperformed the industry over the past year. Shares surged 169.5% in this period compared with a 10.9% rise of the industry.

Penumbra exited the first quarter of 2023 with better-than-expected results. The company’s vascular and neuro product categories showed encouraging growth trends. Its robust estimate for 2023 revenues reflects continued demand for its products. Strong uptake following the launch of Lightning Flash during the first quarter accelerated the growth of the Vascular business. Penumbra’s Immersive Healthcare business is also making significant progress.

The company recently established a multiyear collaboration with the Department of Veteran Affairs Office of Healthcare Innovation and Learning to test, co-develop and scale virtual reality solutions for veterans in multiple healthcare settings, including home. Although currency movements continue to adversely impact the top line, the impact is expected to become favorable in the second half of 2023. Moreover, Penumbra’s ability to improve net gross margins and EPS amid ongoing inflationary pressure and supply-chain headwinds buoy optimism.

Penumbra, Inc. Price

Penumbra, Inc. price | Penumbra, Inc. Quote

In the first quarter of 2023, Penumbra’s international revenues registered 8% sequential growth, taking the international business revenue run rate to more than $0.25 billion annually. The company also launched the RED catheter for stroke and the first-generation computer-orchestrated thrombectomy products, Lightning 12 and 7, in Europe.

Penumbra expects to materially increase both revenue and profitability in the company’s international business in the next three years and beyond. During this period, the company expects to bring its franchise products like RED catheters and CAT RX together with all its most advanced products, Lightning Flash, Lightning Bolt 7 and Thunderbolt, to Penumbra global teams.

The company’s global revenue growth rate is expected to accelerate on a year-over-year basis through 2023 to the low 20% range in the second quarter and the mid-to-high 20% range in the second half of 2023.

On the flip side, in the first quarter of 2023, Penumbra’s total revenues were impacted by variability in international distributor region revenues compared to the same period last year. In the first quarter, gross margin was impacted by higher start-up costs associated with multiple new product launches and regional mix. The company also experienced higher seasonality expenditures. Selling, general and administrative expenses rose 11%. Total operating expenses were up 8.8% year over year.

Meanwhile, currency movements continue to adversely impact the top line. We note that a significant portion of Penumbra’s sales and costs is exposed to changes in foreign exchange rates. The company’s operations use multiple foreign currencies, including the euro and Japanese yen. Changes in those currencies relative to the U.S. dollar will impact its sales, cost of sales and expenses, and consequently, net income. In the first quarter, changes in exchange rates affected Penumbra’s revenues by $2.6 million.

Key Picks

Some better-ranked stocks in the overall healthcare sector are Haemonetics HAE, Zimmer Biomet ZBH and SiBone SIBN. While Haemonetics sports a Zacks Rank #1 (Strong Buy), Zimmer Biomet and SiBone each carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Haemonetics stock has risen 29.8% in the past year. The Zacks Consensus Estimate for Haemonetics’ earnings per share (EPS) has increased from $3.55 to $3.56 for fiscal 2024 and remained constant at $3.96 for fiscal 2025 in the past 30 days.

HAE’s earnings beat estimates in the trailing four quarters, the average surprise being 12.21%. In the last reported quarter, the company registered an earnings surprise of 13.24%.

The Zacks Consensus Estimate for Zimmer Biomet’s 2023 EPS has remained constant at $7.45 in the past 30 days. Shares of the company have improved 38.3% in the past year against the industry’s 22.6% decline.

ZBH’s earnings beat estimates in the trailing four quarters, the average surprise being 7.38%. In the last reported quarter, the company recorded an earnings surprise of 13.86%.

The Zacks Consensus Estimate for SiBone’s 2023 loss per share has narrowed from $1.44 to $1.42 in the past 30 days. SIBN shares have improved 103.5% in the past year compared with the industry’s 8.9% growth.

SiBone’s earnings beat estimates in three of the trailing four quarters and missed the same in one, the average surprise being 11.11%. In the last reported quarter, the company recorded an earnings surprise of 21.95%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Haemonetics Corporation (HAE) : Free Stock Analysis Report

Zimmer Biomet Holdings, Inc. (ZBH) : Free Stock Analysis Report

Penumbra, Inc. (PEN) : Free Stock Analysis Report

SiBone (SIBN) : Free Stock Analysis Report