Americans continue to worry about their finances, according to a new survey by Bank of America, and student debt is particularly stressful.

The survey analyzed responses from 1,000 Americans throughout the U.S. and found that 51% are worried about their finances over the next few years. Respondents were particularly concerned about not having enough savings, the possibility of a looming recession, as well as their ability to cope with debt.

And the expert behind the report singled out student loans as the big issue.

“Student debt is probably leading the way,” Aron Levine, Head of Consumer Banking at Bank of America, told Yahoo Finance’s The Ticker (video above). “That is absolutely one of the No.1 major concerns. Whether it’s the actual student who took on the debt, parents, grandparents who have co-signed for the debt… That’s a huge one.”

Excluding their mortgages, 73% of respondents were found to be carrying some sort of debt: 43% credit card debt, 36% auto loan debt, 20% student debt, and 15% in other personal loans. Nearly half of that number owed more than $20,000 in debt overall.

Over the past few years, outstanding student debt has ballooned to $1.49 trillion in the first quarter of 2019. Borrowers are increasingly unable to meet repayment deadlines, with delinquency rates rising steadily from 9.08% in the last quarter in 2018 to 9.54% in Q1 2019, according to data from the New York Fed.

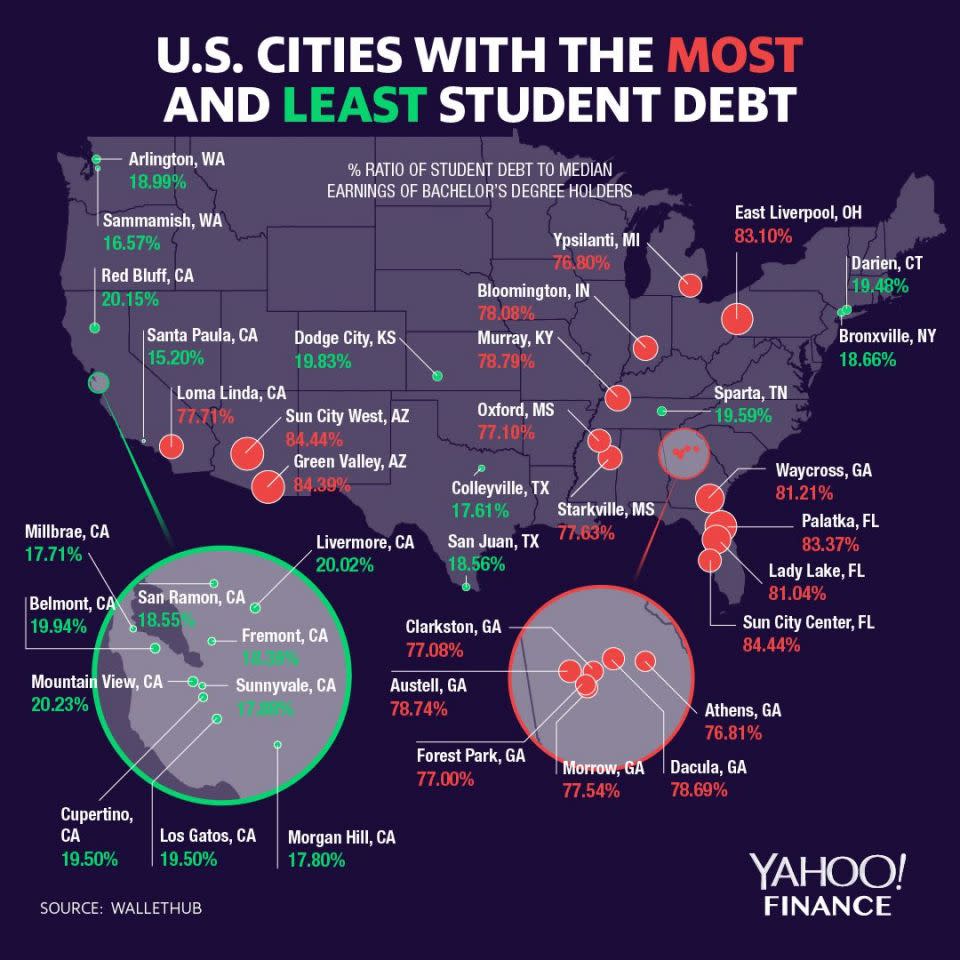

Student loan burdens are particularly tough in the South, where some cities are seeing 70% or more of their annual income owed in student debt.

Spreading the burden around

And graduates aren’t the only one feeling the pain.

Parents, and as Levine mentioned, even grandparents are going into debt to pay for their children’s and grandchildren’s education. Last year, while 69% of college students took out loans of around $29,800 on average, 14% of their parents took out $35,600, according to Student Loan Hero.

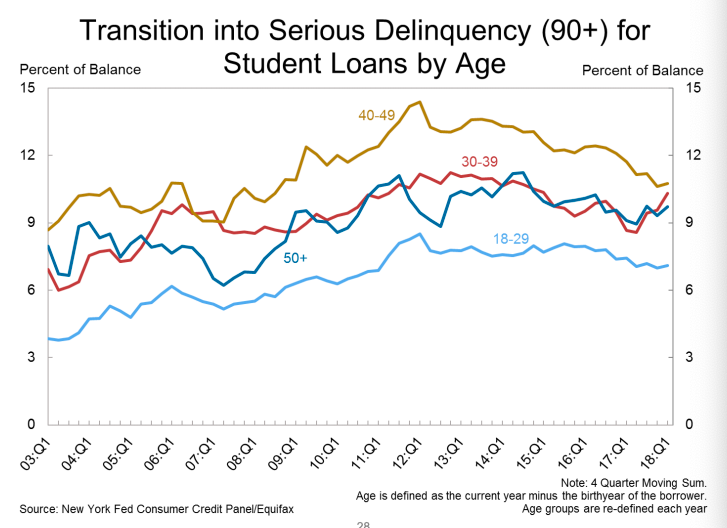

In the graph below, data from the New York Fed illustrates how the outstanding student loans taken out by the 40 to 49 age group ranks highest in terms of debt that’s transitioning into serious delinquency.

Those above 50 are also finding it increasingly hard to pay back their — or their children’s — student loans.

Student debt crisis is ‘crushing millions’

Responding to these numbers, Democratic presidential candidate and Massachusetts Senator Elizabeth Warren — who has promised mass student cancellations as part of her election campaign — has now accelerated the push to alleviate borrowers’ burdens by introducing legislation in the Senate and House to eliminate up to $50,000 in student debt for 42 million Americans.

“The student debt crisis is real and it’s crushing millions of people -- especially people of color,” Warren said in a press release. “It’s time to decide: Are we going to be a country that only helps the rich and powerful get richer and more powerful, or are we going to be a country that invests in its future?”

—

Aarthi is a writer for Yahoo Finance. Follow her on Twitter @aarthiswami.

Read more:

Over half of parents willing to go into debt to pay children’s college tuition

Household debt hits $13.6 trillion as student loan and credit card delinquencies rise

Elizabeth Warren unveils 'broad cancellation plan' for student debt

'The clock is ticking' on U.S. consumer loans — and that could mean a slowdown, Deutsche Bank warns

Read the latest financial and business news from Yahoo Finance

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.