Photronics (NASDAQ:PLAB) Reports Weak Q1

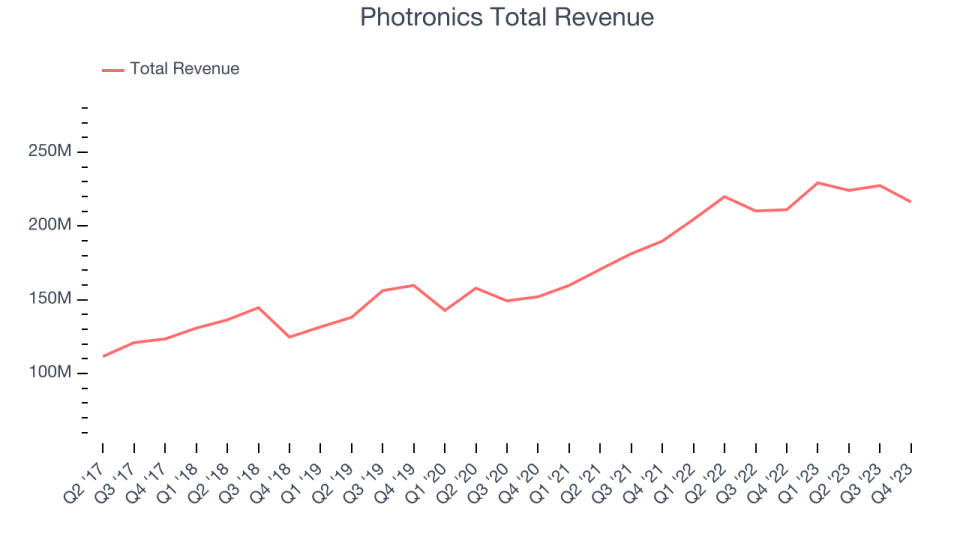

Semiconductor photomask manufacturer Photronics (NASDAQ:PLAB) fell short of analysts' expectations in Q1 FY2024, with revenue up 2.5% year on year to $216.3 million. On the other hand, the company expects next quarter's revenue to be around $231 million, in line with analysts' estimates. It made a GAAP profit of $0.42 per share, improving from its profit of $0.23 per share in the same quarter last year.

Is now the time to buy Photronics? Find out by accessing our full research report, it's free.

Photronics (PLAB) Q1 FY2024 Highlights:

Revenue: $216.3 million vs analyst estimates of $220 million (1.7% miss)

EPS (non-GAAP): $0.48 vs analyst expectations of $0.49 (2% miss)

Revenue Guidance for Q2 2024 is $231 million at the midpoint, roughly in line with what analysts were expecting

Free Cash Flow was -$1.81 million, down from $54.14 million in the previous quarter

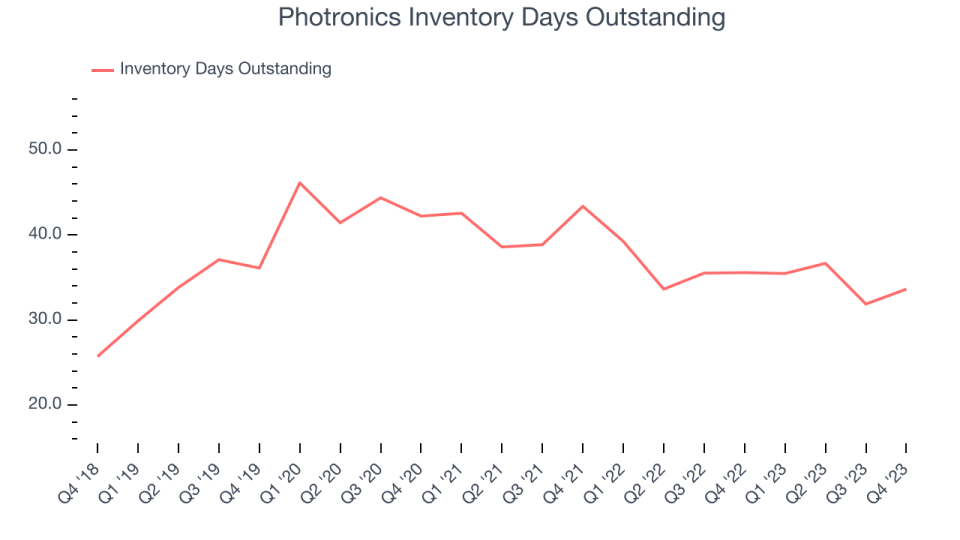

Inventory Days Outstanding: 34, up from 32 in the previous quarter

Gross Margin (GAAP): 36.6%, up from 36% in the same quarter last year

Market Capitalization: $1.95 billion

“First quarter revenue increased year-over-year even though typically lower seasonal demand was weaker than anticipated, especially in the beginning of the quarter. Order rates improved through the quarter, continuing into second quarter,” said Frank Lee, CEO.

Sporting a global footprint of facilities, Photronics (NASDAQ:PLAB) is a manufacturer of photomasks, templates used to transfer patterns onto semiconductor wafers.

Semiconductor Manufacturing

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers, and data storage. The need for technologies like artificial intelligence, 5G networks, and smart cars is also creating the next wave of growth for the industry. Keeping up with this dynamism requires new tools that can design, fabricate, and test chips at ever smaller sizes and more complex architectures, creating a dire need for semiconductor capital manufacturing equipment.

Sales Growth

Photronics's revenue growth over the last three years has been mediocre, averaging 14.6% annually. As you can see below, this was a weaker quarter for the company, with revenue growing from $211.1 million in the same quarter last year to $216.3 million. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

Photronics had a tough quarter as its weak 2.5% year-on-year revenue growth missed analysts' estimates by 1.7%.

Photronics's management team believes its revenue growth will continue, guiding to 0.7% year-on-year growth next quarter. Analysts expect the company to grow its revenue by 5.9% over the next 12 months.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business' capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Photronics's DIO came in at 34, which is 4 days below its five-year average. These numbers show that despite the recent increase, there's no indication of an excessive inventory buildup.

Key Takeaways from Photronics's Q1 Results

We were impressed by Photronics's strong operating margin improvement this quarter, but that's where the good news ends. Its revenue, EBITDA, and EPS unfortunately missed analysts' estimates as demand was weaker than expected. Looking ahead to Q2, its revenue guidance was in line while its EPS outlook fell short. Overall, the results could have been better. The stock is flat after reporting and currently trades at $31.1 per share.

Photronics may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.