PLMR or AXS: Which P&C Insurance Stock is Better Positioned?

The Zacks Property and Casualty (P&C) Insurance industry has been benefiting from higher retention, streamlined operations, global presence, better pricing, solid underwriting, an improving rate environment and a strong capital position. With the ongoing economic expansion, insurers remain well-poised for growth. However, catastrophe losses might have weighed on P&C insurers.

The industry has risen 32.3% in the past year, outperforming the Zacks S&P 500 Composite’s increase of 28.6% and the Finance sector’s 24.3% growth.

Image Source: Zacks Investment Research

Here we focus on two property and casualty insurers, namely Palomar Holdings, Inc. PLMR and Axis Capital Holdings Limited AXS.

Palomar Holdings, with a market capitalization of $2 billion, offers personal and commercial specialty property insurance products to residential and businesses in the United States. Axis Capital, with a market capitalization of $5.3 billion, provides various specialty insurance and reinsurance products worldwide. PLMR and AXS sport a Zacks Rank #1 (Strong Buy) each at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Global commercial insurance prices rose for 25 straight quarters, per Marsh Global Insurance Market Index.

Better pricing, operational strength, higher retention and strong renewal should drive higher premiums. Per Deloitte Insights, gross premiums are estimated to increase six-fold to $722 billion by 2030. Analysts at Swiss Re Institute predict premiums to grow 5.5% in 2024.

Per Aon, total economic losses were $380 billion, while insured losses were $118 million in 2023.

Per AM Best, total net underwriting loss was $38 billion in 2023, a 10-year high, largely attributable to weather-related losses, high inflation, as well as reinsurance pricing pressure. The combined ratio was 103.7 for the same time frame per the credit rating giant, to which catastrophe losses added 780 basis points (bps). AM Best also estimates cat loss to contribute 680 bps to the expected combined ratio of 100.7 in 2024.

Exposure growth, improved pricing, prudent underwriting, favorable reserve development and a sturdy capital position will help absorb catastrophe losses. Also, frequent occurrences of natural disasters should accelerate the policy renewal rate.

The insurance industry is rate-sensitive. The Fed made four hikes in 2023, taking the tally to 11 since March 2022. An improving rate environment is a boon for insurers, especially long-tail insurers. The Fed has held interest rates unchanged at 5.25-5.5% at the December FOMC meeting.

A solid capital level supports insurers in pursuing strategic mergers and acquisitions to gain market share, expand in niche areas and diversify operations into new business lines and geography, as well as increase dividends, pay special dividends and buy back shares.

Simultaneously, the use of real-time data is making premium calculation easier and reducing risk. Increased automation is expected to drive premium growth and boost efficiency. Accelerated digitization, robotic process automation, cognitive intelligence and blockchain should help life insurers curb operational costs and aid margin expansion.

Let’s delve deeper into specific parameters to ascertain which P&C insurer is better positioned at the moment.

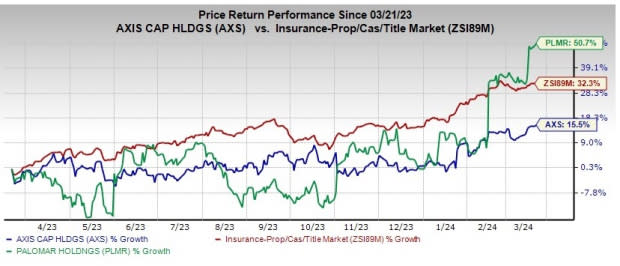

Price Performance

Palomar Holdings has gained 50.7% in the past year, outperforming Axis Capital’s rise of 15.5% and industry’s growth of 32.3%.

Image Source: Zacks Investment Research

Return on Equity (ROE)

Palomar Holdings, with a ROE of 19.3%, exceeds Axis Capital’s ROE of 19.2% and the industry average of 7.3%.

Image Source: Zacks Investment Research

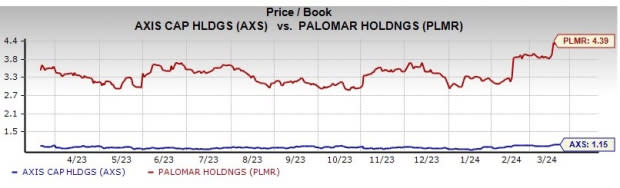

Valuation

The price-to-book value is the best multiple used for valuing insurers. Compared with Palomar Holdings’s P/B ratio of 4.39, Axis Capital is cheaper, with a reading of 1.15. The P&C insurance industry’s P/B ratio is 1.53.

Image Source: Zacks Investment Research

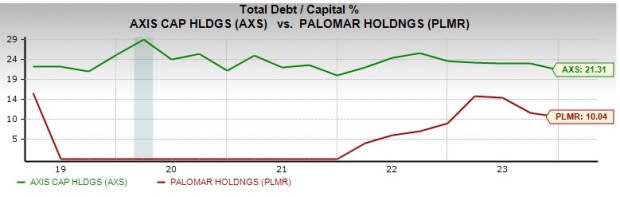

Debt-to-Capital

Axis Capital’s debt-to-capital ratio of 21.3 is higher than the industry average of 18.8 and Palomar Holdings’s reading of 10. Therefore, PLMR has an advantage over AXS on this front.

Image Source: Zacks Investment Research

Growth Projection

The Zacks Consensus Estimate for 2024 earnings indicates 3% growth from the year-ago reported figure for Axis Capital, while the same for Palomar Holdings indicates an increase of 16.3%.

Combined Ratio

AXS’ combined ratio was 99.9% in 2023, whereas that of PLMR was 76.6% in the said time frame. Thus, the combined ratio of Palomar Holdings is better than that of Axis Capital.

Revenue Estimates

The Zacks Consensus Estimate for Palomar Holdings' and Axis Capital's 2024 revenues implies a year-over-year increase of 24.5% and 3.6%, respectively.

Therefore, PLMR is at an advantage on this front.

To Conclude

Our comparative analysis shows that Palomar Holdings is better positioned than Axis Capital with respect to price, return on equity, leverage, growth projection, combined ratio and revenue estimates. Meanwhile, Axis Capital scores higher only in terms of valuation. With the scale majorly tilted toward Palomar Holdings, the stock appears to be better poised.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Axis Capital Holdings Limited (AXS) : Free Stock Analysis Report

Palomar Holdings, Inc. (PLMR) : Free Stock Analysis Report