Pool Corp. (POOL) Outruns Industry in a Year: More Room to Run?

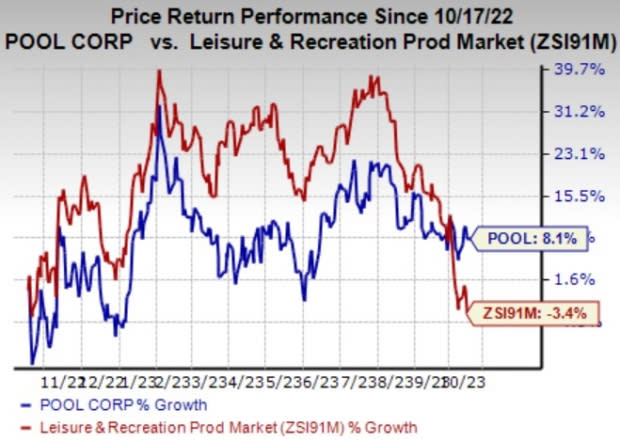

Pool Corporation POOL have gained 8.1% in the past year against the Zacks Leisure and Recreation Products industry’s 3.4% fall. The company has been benefiting from solid base business performance and a large market presence. Also, the emphasis on strategic expansion bodes well.

The Zacks Consensus Estimate for POOL’s 2024 sales and earnings per share (EPS) suggests increases of 6% and 10.6%, respectively, from the year-ago period’s levels. The company also has a long-term earnings growth rate of 5.9%.

Image Source: Zacks Investment Research

Let’s discuss the factors substantiating its Zacks Rank #2 (Buy).

Existing Pools Being Reliable Income Stream: POOL generates most of its earnings from existing pools, with over half of its gross profits coming from pool maintenance and repair products. The rest comes from the construction and installation of pools and landscaping.

The pool industry has been recovering in the last five years thanks to more people renovating and replacing their pools. It believes the rise in working from home will encourage more home improvements. New products like automation and connected pools and the trend of moving away from cities will likely contribute to this growth.

Solid Brand Presence: The company benefits from its leading market position, giving it a cost advantage and higher return on investment compared with smaller competitors. Despite many rivals and low entry barriers, the housing market continues to drive demand for its products.

Moreover, solid demand for swimming pool maintenance supplies, above-ground pools, spas, and automatic pool cleaners, heaters, pumps, lights, chemicals and filters continues to drive the company’s results. Given the products’ importance in repair, replacement, new construction and remodeling activities, the continuation of demand is likely to support top-line growth in the upcoming periods.

Expansion Strategy to Drive Growth: The company is focused on driving revenues. It is entering new geographic areas, expanding existing markets and introducing innovative product categories to increase its market share. To this end, the company is also trying to grow through various acquisitions.

In 2023, the company made several acquisitions. These include acquiring the distribution assets of Pioneer Pool Products, Inc. in Alabama and adding a location in North Dakota through the acquisition of Recreation Supply Company. Additionally, the company expanded its presence in Arizona by acquiring the distribution assets of Pro-Water Irrigation & Landscape Supply, Inc., establishing two new locations. These acquisitions reflect on the company's commitment to expanding its operations and serving diverse customer needs across multiple regions.

Also, the company continues to make progress with organic growth and greenfield expansion. During the second quarter of 2023, the company added five new greenfield distribution locations thereby bringing the total count to eight. The company is on track to open 10 greenfield distribution locations in 2023.

Other Key Picks

Some other top-ranked stocks from the Zacks Consumer Discretionary sector are:

Adtalem Global Education Inc. ATGE currently carries a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here. It has a trailing four-quarter earnings surprise of 22%, on average. The stock has surged 19.3% in the past year.

The Zacks Consensus Estimate for ATGE’s 2023 sales and EPS suggests growth of 3% and 2.4%, respectively, from the year-ago period’s levels.

OneSpaWorld Holdings Limited OSW currently sports a Zacks Rank #2. It has a trailing four-quarter earnings surprise of 42.6%, on average. The stock has gained 21.6% in the past year.

The Zacks Consensus Estimate for OSW’s 2023 sales and EPS indicates growth of 44.5% and 117.9%, respectively, from the year-ago period’s levels.

Hilton Worldwide Holdings Inc. HLT has a Zacks Rank #2. It has a trailing four-quarter earnings surprise of 12.5%, on average. The stock has gained 18.6% in the past year.

The Zacks Consensus Estimate for HLT’s 2023 sales and EPS suggests increases of 14.8% and 23.7%, respectively, from the year-ago period’s levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Pool Corporation (POOL) : Free Stock Analysis Report

Hilton Worldwide Holdings Inc. (HLT) : Free Stock Analysis Report

Adtalem Global Education Inc. (ATGE) : Free Stock Analysis Report

OneSpaWorld Holdings Limited (OSW) : Free Stock Analysis Report