Post Holdings (POST) Appears Well-Positioned for Growth in 2024

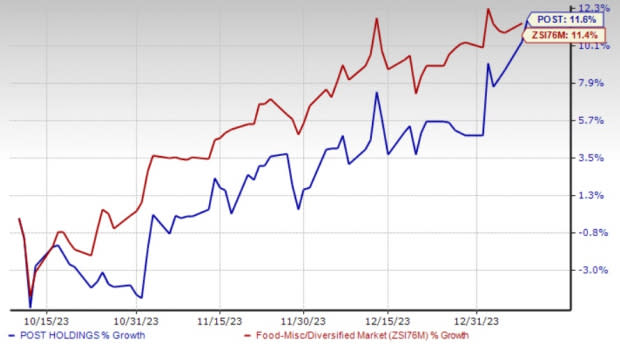

Post Holdings, Inc. POST appears well-placed for 2024 with its strategic pricing and focus on acquisitions. Buyouts have been helping this consumer packaged goods holding company strengthen its customer base. Shares of POST have rallied 11.6% in the past three months compared with the industry’s growth of 11.4%.

These upsides are likely to continue working well for this Zacks Rank #3 (Hold) company amid elevated SG&A costs and supply-chain headwinds. The Zacks Consensus Estimate for fiscal 2024 earnings per share (EPS) has increased 1.2% to $4.88 over the past 30 days.

Adding Leaves to the Growth Story

Buyouts have been a key driver for Post Holdings. The company concluded the acquisition of Perfection Pet Foods on Dec 1, 2023, which is a major producer and packager of private-label and co-manufactured pet food and baked treat products. This strategic move aligns with Post Holdings' wider objectives in the pet food industry.

This was also demonstrated by the company’s previous acquisition of various pet food brands and the private-label pet food business from The J.M. Smucker Co. in April 2023. These acquisitions help diversify the company's product portfolio and create growth opportunities in the pet food industry. The company’s fourth-quarter sales included $404.5 million from its latest Pet Food acquisition.

Some other notable acquisitions in the past few years include Lacka Foods Limited (April 2022), which is a U.K.-based marketer of UFIT high-protein shakes. In June 2021 and February 2021, the company acquired TreeHouse Foods' RTE Cereal Business and Almark Foods, respectively. In the same year, it purchased the Peter Pan peanut butter brand and partnered with the plant-based meat company Hungry Planet.

Apart from this, the company has been on track to optimize its network to serve its customers and consumers better. The company recently unveiled plans to shut down the Post Consumer Brands cereal production unit in Lancaster, Ohio. The move reflects the company’s requirement to lower its capacity in the cereal production network.

Image Source: Zacks Investment Research

Navigating the Hurdles

Post Holdings has been seeing a rise in SG&A costs for a while. In the fourth quarter of fiscal 2023, SG&A expenses escalated 38.3% year over year to $309.5 million due to the company’s targeted marketing investments in its retail businesses as well as higher employee incentives. SG&A expenses, as a percentage of sales, came in at 15.9%, up from 14.2% reported in the year-ago quarter. The persistence of this headwind is a concern.

The company has long been bearing the brunt of supply-chain bottlenecks. On its fourth-quarter fiscal 2023 earnings call, management stated that although the supply-chain scenario and customer order fill rates have been improving, there is still significant room for enhancement in both areas. Cost inflation is another hurdle, although it is moderating. Markedly, gains from pricing actions have been helping the company counter inflation, as witnessed in the fourth quarter as well.

Looking Ahead

On concluding the buyout of Perfection Pet Foods, Post Holdings updated its adjusted EBITDA guidance for fiscal 2024 to include 10 months of contribution from the acquisition. Management expects adjusted EBITDA in the range of $1,220-$1,280 million for fiscal 2024 compared with the $1,200-$1,260 million range guided in the fourth-quarter fiscal 2023 earnings release. In fiscal 2023, POST’s adjusted EBITDA came in at $1,233.4 million.

3 Promising Food Bets

Sysco Corporation SYY, a food and related product company, currently carries a Zacks Rank #2 (Buy). SYY delivered a back-to-back positive earnings surprise in the past two quarters. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Sysco’s current fiscal-year sales and earnings suggests growth of 4.1% and nearly 8%, respectively, from the year-ago reported numbers.

Ingredion Incorporated INGR, which produces and sells sweeteners, starches, nutrition ingredients and biomaterial solutions, holds a Zacks Rank #2. INGR delivered a positive earnings surprise of 23.9% in the last reported quarter.

The Zacks Consensus Estimate for Ingredion Incorporated’s current financial-year sales and earnings suggests growth of around 5% and 24.7%, respectively, from the year-ago reported numbers.

Nomad Foods NOMD manufactures, markets and distributes a range of frozen food products. It currently has a Zacks Rank #2. NOMD has a trailing four-quarter earnings surprise of 7.7%, on average.

The Zacks Consensus Estimate for Nomad Foods’ current financial-year sales suggests growth of 6.6% from the year-ago reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Sysco Corporation (SYY) : Free Stock Analysis Report

Ingredion Incorporated (INGR) : Free Stock Analysis Report

Post Holdings, Inc. (POST) : Free Stock Analysis Report

Nomad Foods Limited (NOMD) : Free Stock Analysis Report