Post (NYSE:POST) Surprises With Q1 Sales

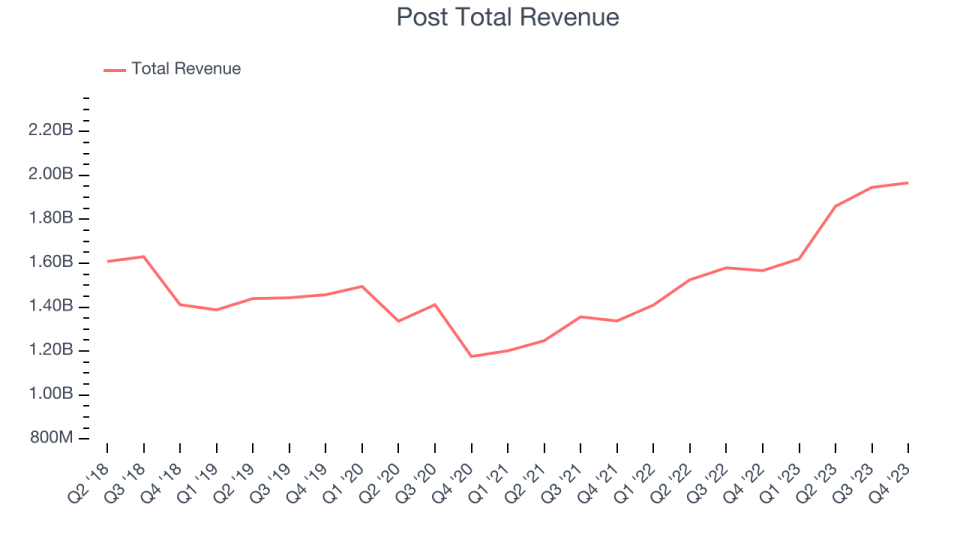

Packaged foods company Post (NYSE:POST) reported Q1 FY2024 results beating Wall Street analysts' expectations , with revenue up 25.5% year on year to $1.97 billion. It made a non-GAAP profit of $1.69 per share, improving from its profit of $1.08 per share in the same quarter last year.

Is now the time to buy Post? Find out by accessing our full research report, it's free.

Post (POST) Q1 FY2024 Highlights:

Revenue: $1.97 billion vs analyst estimates of $1.92 billion (2.4% beat)

EPS (non-GAAP): $1.69 vs analyst estimates of $1.10 (53.4% beat)

Free Cash Flow of $174.4 million, similar to the previous quarter

Gross Margin (GAAP): 29.1%, up from 26.5% in the same quarter last year

Sales Volumes were down 3.6% year on year

Market Capitalization: $5.62 billion

Founded in 1895, Post (NYSE:POST) is a packaged food company known for its namesake breakfast cereal as well as protein bars, shakes, and other healthier-for-you snacks.

Packaged Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods, prepared meals, or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences.The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Sales Growth

Post is one of the larger consumer staples companies and benefits from a well-known brand, giving it customer mindshare and influence over purchasing decisions.

As you can see below, the company's annualized revenue growth rate of 9% over the last three years was decent for a consumer staples business.

This quarter, Post reported remarkable year-on-year revenue growth of 25.5%, and its $1.97 billion in revenue topped Wall Street estimates by 2.4%. Looking ahead, Wall Street expects sales to grow 9.3% over the next 12 months, a deceleration from this quarter.

It’s not often you find a high-quality company at a significant discount to its historical P/E multiple, but that’s exactly what we found. Click here for your FREE report on this attractive Network Effect stock at a very silly price.

Key Takeaways from Post's Q1 Results

We were impressed by how significantly Post blew past analysts' gross margin, operating profit, EBITDA, and EPS expectations this quarter. Its revenue growth also topped estimates, driven by strong top-line performance in its Post Consumer segment ($989 million of revenue vs consensus estimates of $905 million), which consists of ready-to-eat (“RTE”) cereal, pet food, and peanut butter. The company also raised its full-year 2024 EBITDA guidance to $1,315 million at the midpoint and announced a new $400 million share repurchase authorization, putting a stamp on a fantastic "beat-and-raise" quarter. Shareholders should be satisfied. The stock is up 4.8% after reporting and currently trades at $98.33 per share.

Post may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.