Power Integrations (NASDAQ:POWI) Reports Weak Q3, Stock Drops 14.9%

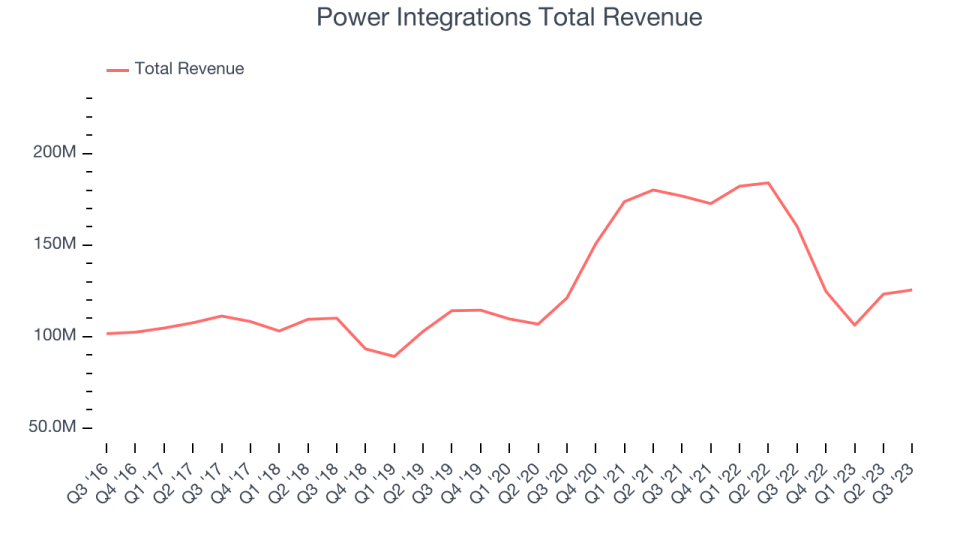

Semiconductor designer Power Integrations (NASDAQ:POWI) fell short of analysts' expectations in Q3 FY2023, with revenue down 21.7% year on year to $125.5 million. Next quarter's revenue guidance of $90 million fell short, coming in 35% below analysts' estimates. Turning to EPS, Power Integrations made a non-GAAP profit of $0.46 per share, down from its profit of $0.80 per share in the same quarter last year.

Is now the time to buy Power Integrations? Find out by accessing our full research report, it's free.

Power Integrations (POWI) Q3 FY2023 Highlights:

Revenue: $125.5 million vs analyst estimates of $130.4 million (3.7% miss)

EPS (non-GAAP): $0.46 vs analyst expectations of $0.47 (2.9% miss)

Revenue Guidance for Q4 2023 is $90 million at the midpoint, below analyst estimates of $138.4 million

Free Cash Flow of $19.2 million, up from $3.1 million in the previous quarter

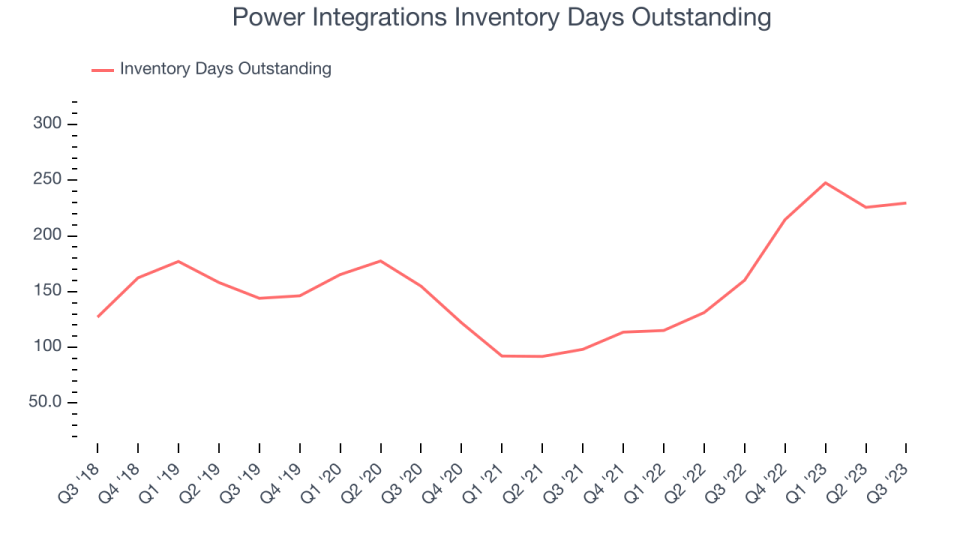

Inventory Days Outstanding: 230, up from 226 in the previous quarter

Gross Margin (GAAP): 52.5%, down from 57.4% in the same quarter last year

A leading supplier of parts for electronics such as home appliances, Power Integrations (NASDAQ:POWI) is a semiconductor designer and developer specializing in products used for high-voltage power conversion.

Analog Semiconductors

Demand for analog chips is generally linked to the overall level of economic growth, as analog chips serve as the building blocks of most electronic goods and equipment. Unlike digital chip designers, analog chip makers tend to produce the majority of their own chips, as analog chip production does not require expensive leading edge nodes. Less dependent on major secular growth drivers, analog product cycles are much longer, often 5-7 years.

Sales Growth

Power Integrations's revenue growth over the last three years has been unimpressive, averaging 7.7% annually. This quarter, its revenue declined from $160.2 million in the same quarter last year to $125.5 million. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

Power Integrations had a difficult quarter as revenue dropped 21.7% year on year, missing analysts' estimates by 3.7%. This could mean that the current downcycle is deepening.

Before the results analysts were expecting that Power Integrations may be headed for an upturn. Although the company is guiding for a year-on-year revenue decline of 27.9% next quarter, analysts were expecting revenue to grow 20.9% over the next 12 months.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business' capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Power Integrations's DIO came in at 230, which is 73 days above its five-year average, suggesting that the company's inventory has grown to higher levels than we've seen in the past.

Key Takeaways from Power Integrations's Q3 Results

With a market capitalization of $4.3 billion, Power Integrations is among smaller companies, but its $356.6 million cash balance and positive free cash flow over the last 12 months give us confidence that it has the resources needed to pursue a high-growth business strategy.

We struggled to find many strong positives in these results. Its revenue guidance for next quarter underwhelmed and its revenue missed Wall Street's estimates. Overall, this was a mediocre quarter for Power Integrations. The company is down 14.9% on the results and currently trades at $63.99 per share.

Power Integrations may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.