It's Probably Less Likely That BIO-key International, Inc.'s (NASDAQ:BKYI) CEO Will See A Huge Pay Rise This Year

The underwhelming share price performance of BIO-key International, Inc. (NASDAQ:BKYI) in the past three years would have disappointed many shareholders. However, what is unusual is that EPS growth has been positive, suggesting that the share price has diverged from fundamentals. These are some of the concerns that shareholders may want to bring up at the next AGM held on 18 June 2021. They could also try to influence management and firm direction through voting on resolutions such as executive remuneration and other company matters. We discuss below why we think shareholders should be cautious of approving a raise for the CEO at the moment.

Check out our latest analysis for BIO-key International

Comparing BIO-key International, Inc.'s CEO Compensation With the industry

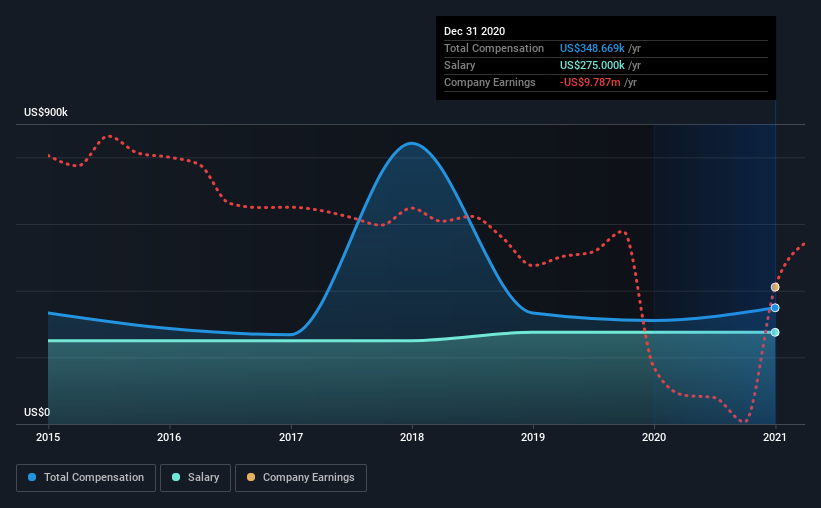

According to our data, BIO-key International, Inc. has a market capitalization of US$32m, and paid its CEO total annual compensation worth US$349k over the year to December 2020. That's a notable increase of 12% on last year. We note that the salary portion, which stands at US$275.0k constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the industry with market capitalizations under US$200m, the reported median total CEO compensation was US$450k. This suggests that BIO-key International remunerates its CEO largely in line with the industry average. What's more, Mike DePasquale holds US$93k worth of shares in the company in their own name.

Component | 2020 | 2019 | Proportion (2020) |

Salary | US$275k | US$275k | 79% |

Other | US$74k | US$36k | 21% |

Total Compensation | US$349k | US$311k | 100% |

On an industry level, roughly 11% of total compensation represents salary and 89% is other remuneration. According to our research, BIO-key International has allocated a higher percentage of pay to salary in comparison to the wider industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at BIO-key International, Inc.'s Growth Numbers

BIO-key International, Inc. has seen its earnings per share (EPS) increase by 12% a year over the past three years. It achieved revenue growth of 88% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. The combination of strong revenue growth with medium-term EPS improvement certainly points to the kind of growth we like to see. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has BIO-key International, Inc. Been A Good Investment?

Few BIO-key International, Inc. shareholders would feel satisfied with the return of -79% over three years. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

The fact that shareholders are sitting on a loss on the value of their shares in the past few years is certainly disconcerting. A huge lag in share price growth when earnings have grown may indicate there could be other issues that are affecting the company at the moment that the market is focused on. If there are some unknown variables that are influencing the stock's price, surely shareholders would have some concerns. These concerns should be addressed at the upcoming AGM, where shareholders can question the board and evaluate if their judgement and decision making is still in line with their expectations.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. That's why we did our research, and identified 4 warning signs for BIO-key International (of which 1 is significant!) that you should know about in order to have a holistic understanding of the stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.