Progress Software (PRGS): Modestly Undervalued or Justly Priced? A Comprehensive Analysis

Progress Software Corp (NASDAQ:PRGS) experienced a daily loss of -2.98% and a three-month loss of -0.66%. Despite this, the company's Earnings Per Share (EPS) stands at 1.84. This analysis aims to answer the question: is Progress Software's stock modestly undervalued? The following comprehensive valuation analysis will explore this in detail.

A Snapshot of Progress Software Corp (NASDAQ:PRGS)

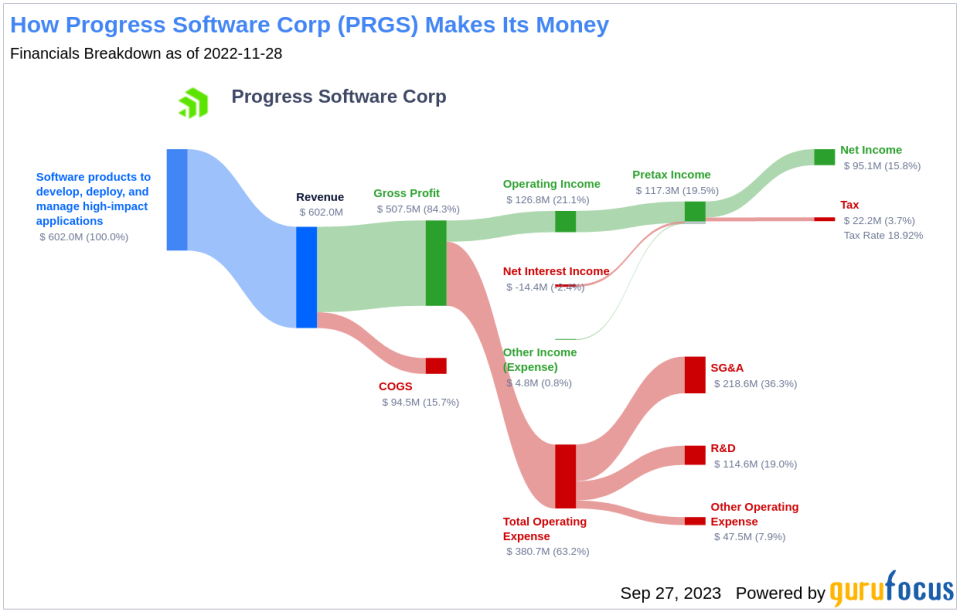

Progress Software Corporation is a prominent provider of cloud-based security solutions to a broad range of industries. The company's product portfolio includes OpenEdge, Chef, Developer Tools, Kemp LoadMaster, MOVEit, DataDirect, WhatsUp Gold, Sitefinity, Flowmon, and Corticon. With a majority of its revenue generated in the United States, Progress Software also has a significant presence in Canada, the Middle East, Africa (EMEA), Latin America, and Asia Pacific.

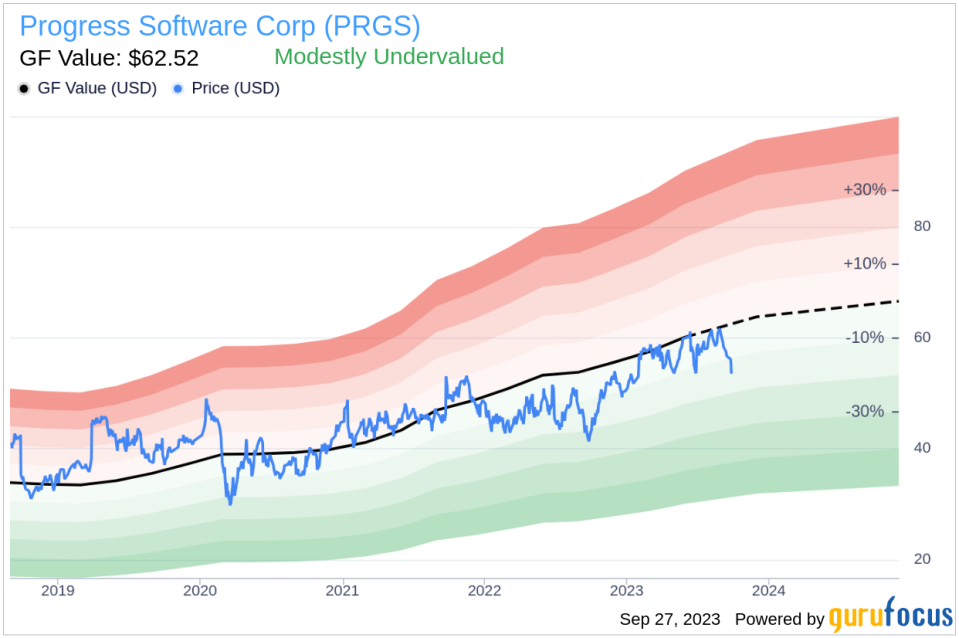

Currently, Progress Software's stock is trading at $53.72, which is below its GF Value of $62.52. This discrepancy opens up an intriguing discussion on the company's intrinsic value.

Understanding the GF Value of Progress Software (NASDAQ:PRGS)

The GF Value is a unique measure of a stock's intrinsic value, calculated based on historical trading multiples, a GuruFocus adjustment factor derived from the company's past performance and growth, and future business performance estimates. The GF Value Line represents the ideal fair trading value of the stock.

According to the GF Value, Progress Software's stock appears to be modestly undervalued. This conclusion is based on historical multiples, an internal adjustment factor based on the company's past growth, and analyst estimates of future business performance. If the stock price is significantly above the GF Value Line, it is overvalued and may yield poor future returns. Conversely, if it is significantly below the GF Value Line, the stock may be undervalued and could offer higher future returns.

Given that Progress Software's stock is currently undervalued, it is likely that the long-term return of its stock will be higher than its business growth.

Link: These companies may deliver higher future returns at reduced risk.

Assessing the Financial Strength of Progress Software

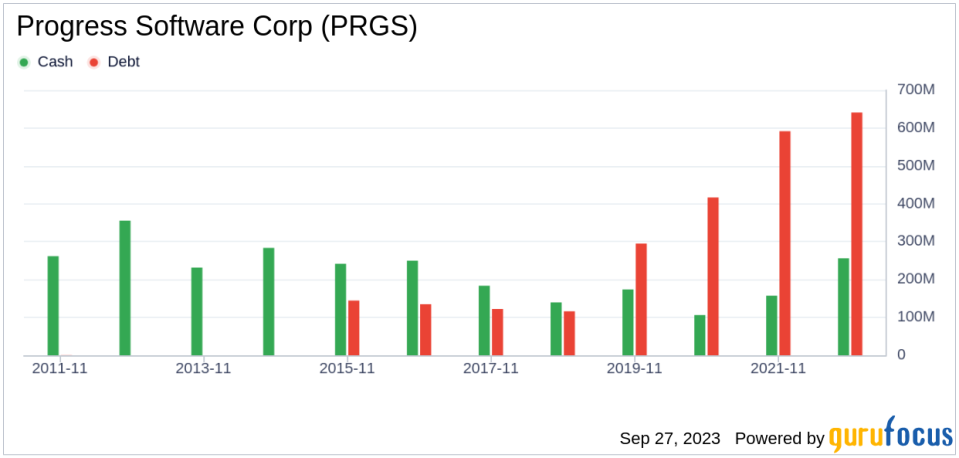

Investing in companies with low financial strength could lead to permanent capital loss. Therefore, it's crucial to carefully review a company's financial strength before deciding to buy shares. A good initial perspective on the company's financial strength can be gained by looking at the cash-to-debt ratio and interest coverage.

Progress Software has a cash-to-debt ratio of 0.15, which ranks worse than 88.52% of 2752 companies in the Software industry. Based on this, GuruFocus ranks Progress Software's financial strength as 4 out of 10, suggesting a poor balance sheet.

Profitability and Growth of Progress Software

Companies that have been consistently profitable over the long term offer less risk for investors. Higher profit margins usually suggest a better investment compared to a company with lower profit margins. Progress Software has been profitable 8 times over the past 10 years. Over the past twelve months, the company had a revenue of $650.80 million and Earnings Per Share (EPS) of $1.84. Its operating margin is 20.41%, which ranks better than 89.44% of 2785 companies in the Software industry. Overall, the profitability of Progress Software is ranked 8 out of 10, indicating strong profitability.

Growth is an important factor in the valuation of a company. GuruFocus research has found that growth is closely correlated with the long-term performance of a company's stock. The faster a company is growing, the more likely it is to be creating value for shareholders, especially if the growth is profitable. The 3-year average annual revenue growth rate of Progress Software is 14.3%, which ranks better than 64.13% of 2414 companies in the Software industry. The 3-year average EBITDA growth rate is 30.8%, which ranks better than 78.38% of 2007 companies in the Software industry.

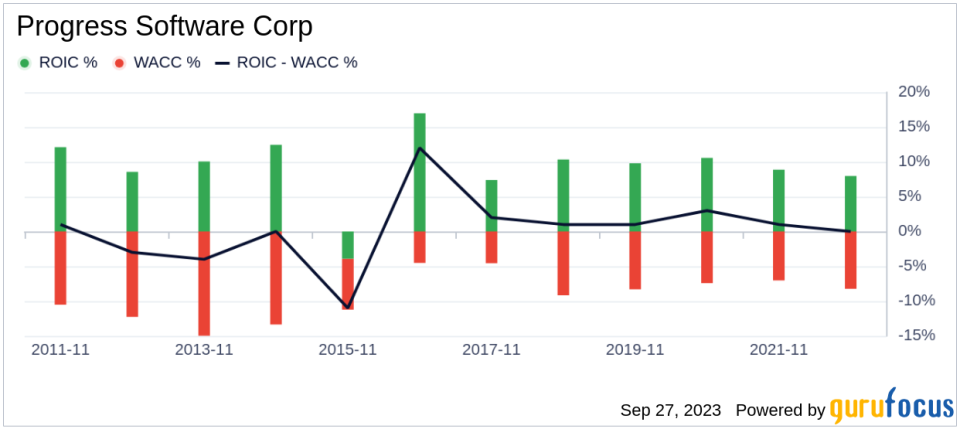

ROIC vs WACC: Evaluating Profitability

Another way to evaluate a company's profitability is to compare its return on invested capital (ROIC) to its weighted cost of capital (WACC). ROIC measures how well a company generates cash flow relative to the capital it has invested in its business. The WACC is the rate that a company is expected to pay on average to all its security holders to finance its assets. If the ROIC is higher than the WACC, it indicates that the company is creating value for shareholders. Over the past 12 months, Progress Software's ROIC was 7.8, while its WACC came in at 7.26.

Conclusion

In conclusion, the stock of Progress Software (NASDAQ:PRGS) is believed to be modestly undervalued. The company's financial condition is poor, but its profitability is strong. Its growth ranks better than 78.38% of 2007 companies in the Software industry. To learn more about Progress Software stock, you can check out its 30-Year Financials here.

To find out the high-quality companies that may deliver above-average returns, please check out the GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.