Progressive (PGR) Stock Rises 29% YTD: Will the Bull Run Last?

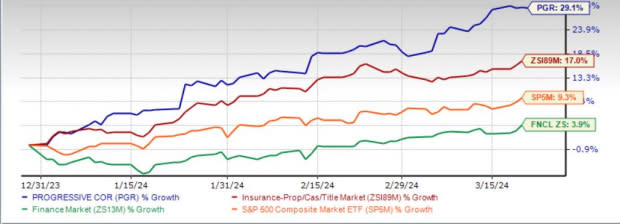

Shares of The Progressive Corporation PGR have rallied 29.1% year to date, outperforming 17%, 3.9% and 9.3% growth of the industry, the Finance sector and the Zacks S&P 500 composite, respectively. With a market capitalization of $120.5 billion, the average volume of shares traded in the last three months was 2.4 million.

A compelling portfolio, leadership position, strength in Vehicle and Property businesses, healthy policies in force, retention and solid capital position continue to drive this largest seller of motorcycle and boat policies. PGR sports a Zacks Rank #1 (Strong Buy) currently.

The Zacks Consensus Estimate for 2024 and 2025 earnings has moved north by 5.4% and 4.1%, respectively, in the past seven days, reflecting analysts’ optimism.

PGR’s trailing 12-month return on equity is 21.3%, ahead of the industry average of 7.3%. Return on equity, a profitability measure, reflects how effectively a company is utilizing its shareholders.

Also, return on invested capital (ROIC) has been increasing over the last few quarters amid capital investment made over the same time frame, reflecting PGR’s efficiency in utilizing funds to generate income. ROIC in the trailing 12 months was 15.1%, better than the industry average of 5.6%.

It has a VGM Score of B. This helps to identify stocks with the most attractive value, growth and momentum. Back-tested results have shown that stocks with a VGM Score of A or B and a Zacks Rank #1 or 2 (Buy) offer better returns.

Image Source: Zacks Investment Research

Can it Retain the Momentum?

The Zacks Consensus Estimate for Progressive’s 2024 earnings is pegged at $9.82 per share, indicating an increase of 60.7% on 15.1% higher revenues of $71.1 billion. The consensus estimate for 2025 earnings is pegged at $11.06 per share, indicating an increase of 12.6% on 2.7% higher revenues of $80.1 billion.

The long-term earnings growth rate is currently pegged at 22.3%, better than the industry average of 12.2%. We expect the 2026 bottom line to increase at a three-year CAGR of 24.9%. Earnings of PGR rose 5.9% in the last five years.

A compelling product portfolio, leadership position, healthy policies in force, better pricing and a solid retention ratio should help PGR generate higher premiums. Its premiums written increased 11% in the last 10 years and surpassed the industry average of 4%. We estimate 2026 net written premiums to increase at a three-year CAGR of 11.3%.

Policy life expectancy (PLE), a measure of customer retention, has improved in the last few years across all business lines. Strategic initiatives to provide consumers with a distinctive new auto insurance option along with competitive pricing should help Progressive deliver solid PLE. The insurer has been focusing on cross-selling homes with auto insurance.

PGR’s combined ratio averaged less than 93% over the last 10 years and compared favorably with the industry average of more than 100%. Prudent underwriting coupled with favorable reserve development should continue to support Progressive in delivering a better combined ratio.

The insurance industry is witnessing accelerated digitalization. In tandem with the industry trend, PGR continues to invest in technology.

Progressive has been paying dividends uninterruptedly since 1971, yielding 0.3%, and has a 25 million share buyback program under its authorization. Notably, its free cash flow conversion has been more than 100% in the last many quarters, reflecting its solid earnings.

Other Stocks to Consider

Some other top-ranked stocks from the same space are Axis Capital Holdings AXS, The Mercury General MCY and Palomar Holdings PLMR, each sporting a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

Axis Capital delivered a trailing four-quarter average earnings surprise of 102.57%. The stock has gained 15.2% year to date.

The Zacks Consensus Estimate for AXS’ 2024 and 2025 earnings indicates an increase of 3.1% and 10.1% from the year-ago levels, respectively. The expected long-term earnings growth rate is 5%. The consensus estimate for 2024 and 2025 earnings has moved up 0.5% and 0.1%, respectively, in the past 30 days.

Mercury General’s earnings surpassed estimates in three of the last four quarters while missing in one. The stock has gained 31% year to date.

The Zacks Consensus Estimate for MCY’s 2024 and 2025 earnings implies a rise of 866.7% and 34.5% from the prior-year levels, respectively.

Palomar delivered a trailing four-quarter average earnings surprise of 11.23%. The stock has gained 48.2% year to date.

The Zacks Consensus Estimate for PLMR’s 2024 and 2025 earnings implies a rise of 16.3% and 18% from the year-earlier figures, respectively. The consensus estimate for PLMR’s 2024 and 2025 earnings has moved up by 1 cent and 2 cents, respectively, in the past seven days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Axis Capital Holdings Limited (AXS) : Free Stock Analysis Report

The Progressive Corporation (PGR) : Free Stock Analysis Report

Mercury General Corporation (MCY) : Free Stock Analysis Report

Palomar Holdings, Inc. (PLMR) : Free Stock Analysis Report