ProPetro Holding (PUMP): A Closer Look at Its Undervalued Status

ProPetro Holding Corp (NYSE:PUMP) recently recorded a daily gain of 5.13%, marking a 31.43% gain over the past three months. The company's Earnings Per Share (EPS) stands at 0.82. Given these figures, the question arises: Is the stock modestly undervalued? This article delves into an in-depth valuation analysis of ProPetro Holding (NYSE:PUMP). Let's explore.

Company Overview

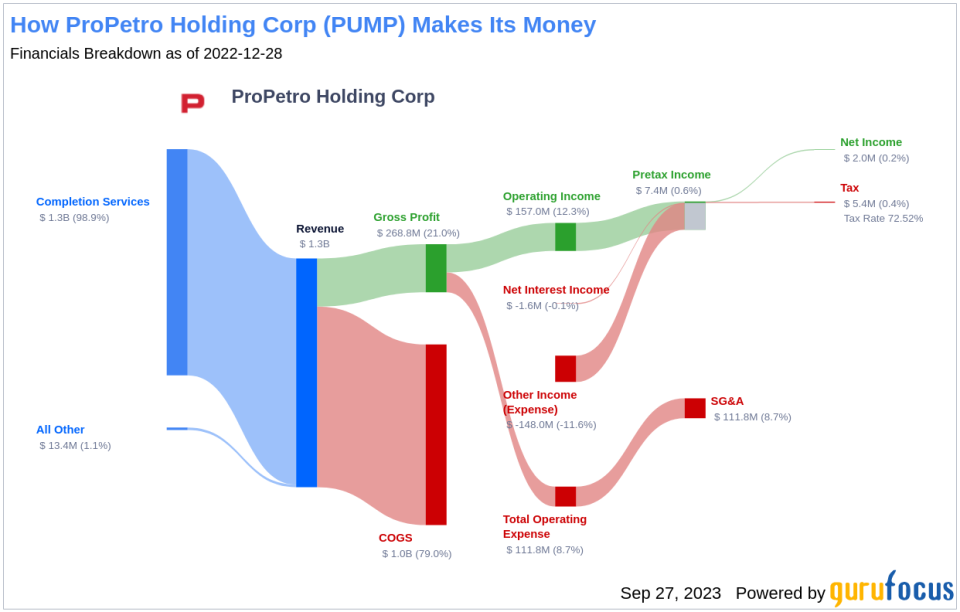

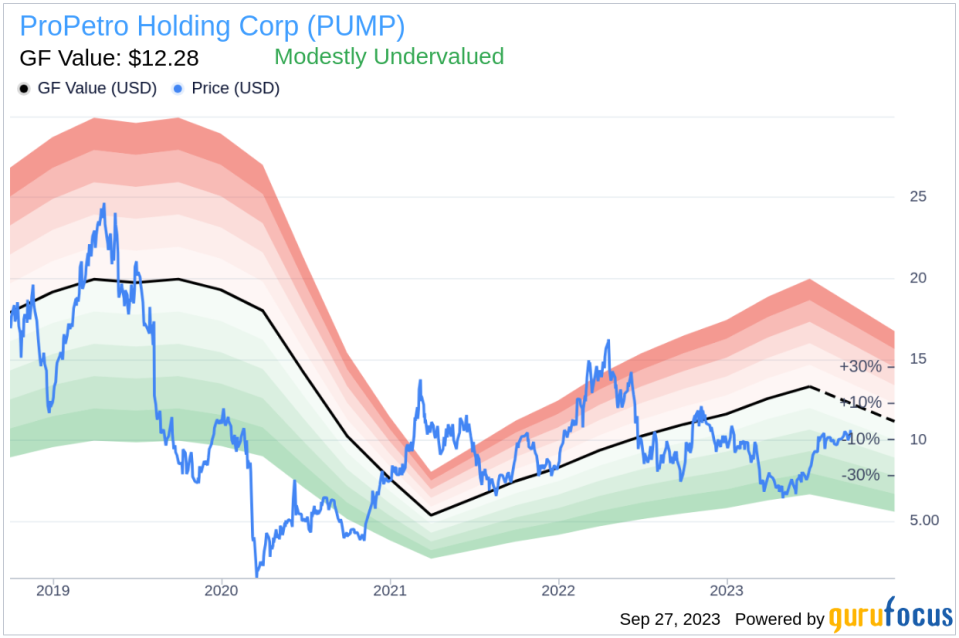

ProPetro Holding Corp is a Texas-based oilfield services company providing hydraulic fracturing, wireline, and other complementary services to oil and gas companies. It primarily focuses on the exploration and production of North American unconventional oil and natural gas resources, particularly in the Permian Basin. With a current stock price of $10.65 per share and a market cap of $1.20 billion, ProPetro Holding's GF Value stands at $12.28, suggesting that the stock could be modestly undervalued.

Understanding GF Value

The GF Value is a proprietary valuation model that estimates a stock's intrinsic value. The GF Value Line gives an overview of the fair value at which the stock should ideally be traded. It is calculated based on historical trading multiples, a GuruFocus adjustment factor based on past performance and growth, and future business performance estimates. If the stock price is significantly above the GF Value Line, it is overvalued, and its future return is likely to be poor. Conversely, if it is significantly below the GF Value Line, its future return will likely be higher.

Considering these factors, ProPetro Holding (NYSE:PUMP) appears to be modestly undervalued. This suggests that the long-term return of its stock is likely to be higher than its business growth.

Financial Strength

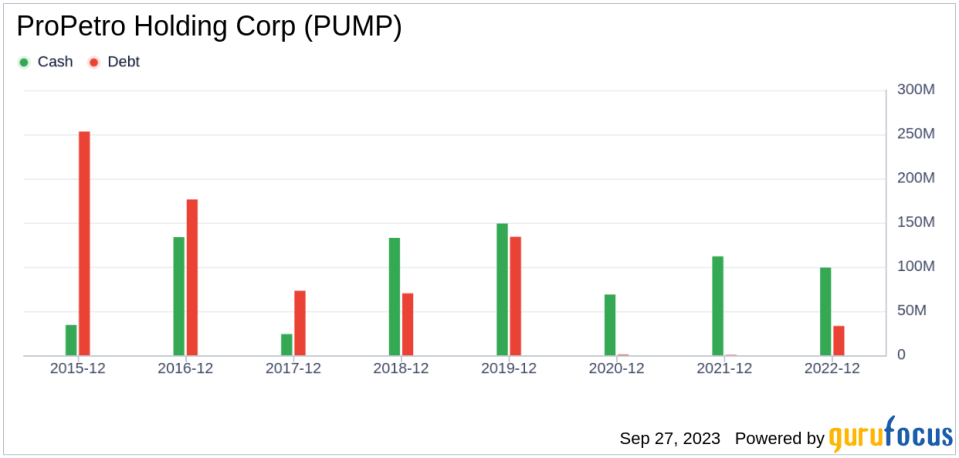

Investing in companies with poor financial strength poses a higher risk of permanent capital loss. It's crucial to review a company's financial strength before deciding to buy its stock. ProPetro Holding's cash-to-debt ratio stands at 1.04, better than 59.19% of companies in the Oil & Gas industry. The company's overall financial strength is ranked 8 out of 10 by GuruFocus, indicating strong financial health.

Profitability and Growth

Investing in profitable companies usually carries less risk. ProPetro Holding has been profitable for 4 out of the past 10 years. With an operating margin of 13.93%, better than 60.16% of companies in the Oil & Gas industry, the company's profitability is ranked as fair by GuruFocus.

However, the growth of a company plays a crucial role in its valuation. ProPetro Holding's 3-year average annual revenue growth is -15.4%, ranking worse than 87.12% of companies in the Oil & Gas industry. The 3-year average EBITDA growth rate is -28.6%, ranking worse than 89.63% of companies in the industry.

ROIC vs. WACC

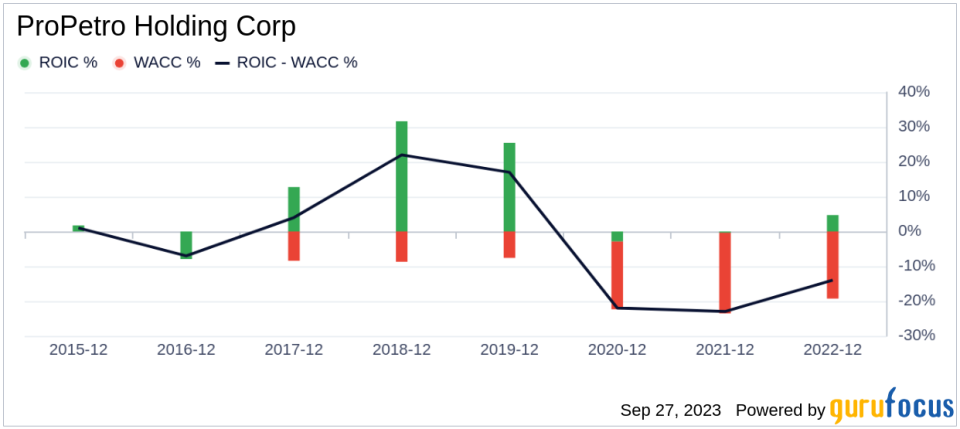

Comparing a company's Return on Invested Capital (ROIC) to the Weighted Average Cost of Capital (WACC) is another way to determine its profitability. When the ROIC is higher than the WACC, it implies the company is creating value for shareholders. ProPetro Holding's ROIC stands at 16.85, and its WACC is 13.7, indicating a positive value creation.

Conclusion

In conclusion, ProPetro Holding Corp (NYSE:PUMP) shows signs of being modestly undervalued. The company's strong financial condition and fair profitability, despite its slower growth compared to other companies in the Oil & Gas industry, make it a potentially interesting prospect for investors. For more information on ProPetro Holding's financials, you can check out its 30-Year Financials here.

To explore high-quality companies that may deliver above-average returns, check out the GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.