Q3 Earnings Review: Footwear Retailer Stocks Led by Boot Barn (NYSE:BOOT)

The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how the footwear retailer stocks have fared in Q3, starting with Boot Barn (NYSE:BOOT).

Footwear sales–like their apparel counterparts–are driven by seasons, trends, and innovation more so than absolute need and similarly face the bigger-picture secular trend of e-commerce penetration. Footwear plays a part in societal belonging, personal expression, and occasion, and retailers selling shoes recognize this. Therefore, they aim to balance selection, competitive prices, and the latest trends to attract consumers. Unlike their apparel counterparts, footwear retailers most sell popular third-party brands (as opposed to their own exclusive brands), which could mean less exclusivity of product but more nimbleness to pivot to what’s hot.

The 4 footwear retailer stocks we track reported a weak Q3; on average, revenues missed analyst consensus estimates by 1.8% while next quarter's revenue guidance was 3% below consensus. Valuation multiples for growth stocks have reverted to their historical means after reaching highs in early 2021, and while some of the footwear retailer stocks have fared somewhat better than others, they have not been spared, with share prices declining 7% on average since the previous earnings results.

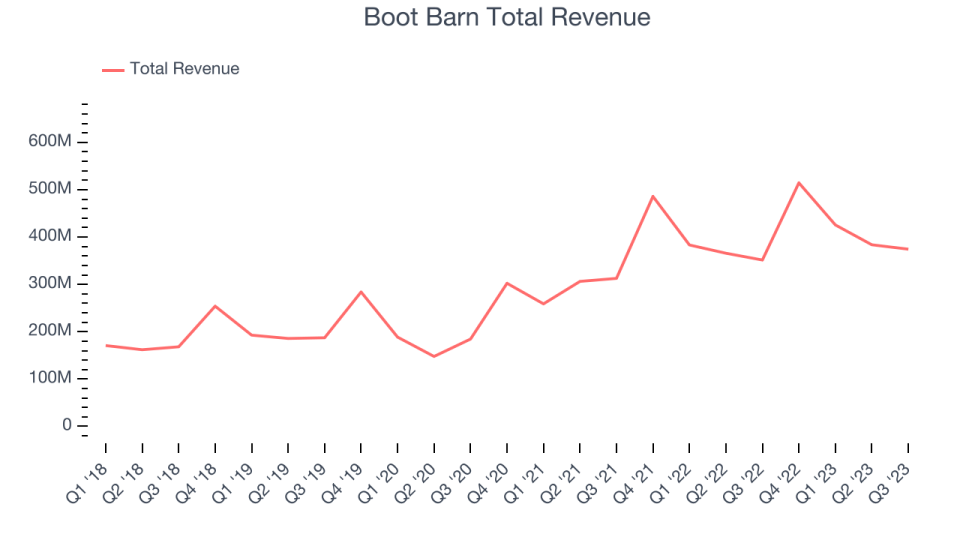

Best Q3: Boot Barn (NYSE:BOOT)

With a strong store presence in Texas, California, Florida, and Oklahoma, Boot Barn (NYSE:BOOT) is a western-inspired apparel and footwear retailer.

Boot Barn reported revenues of $374.5 million, up 6.5% year on year, falling short of analyst expectations by 0.7%. It was a weaker quarter for the company, with underwhelming earnings guidance for the next quarter and revenue guidance for next quarter missing analysts' expectations.

Jim Conroy, President and Chief Executive Officer, commented “I am pleased with our second quarter results which included solid sales growth, merchandise margin expansion and earnings achievement which was at the high end of our guidance range. We opened 10 new stores in the quarter and continue to be encouraged by the new store performance across the country. Exclusive brand penetration expanded more than 600 basis points as our brands are resonating well with the consumer. Our average store sales volume remains at elevated levels with a modest 3.8% decline in retail store same store sales for the quarter.

Boot Barn achieved the fastest revenue growth but had the weakest full-year guidance update of the whole group. The stock is up 7.4% since the results and currently trades at $74.41.

Is now the time to buy Boot Barn? Access our full analysis of the earnings results here, it's free.

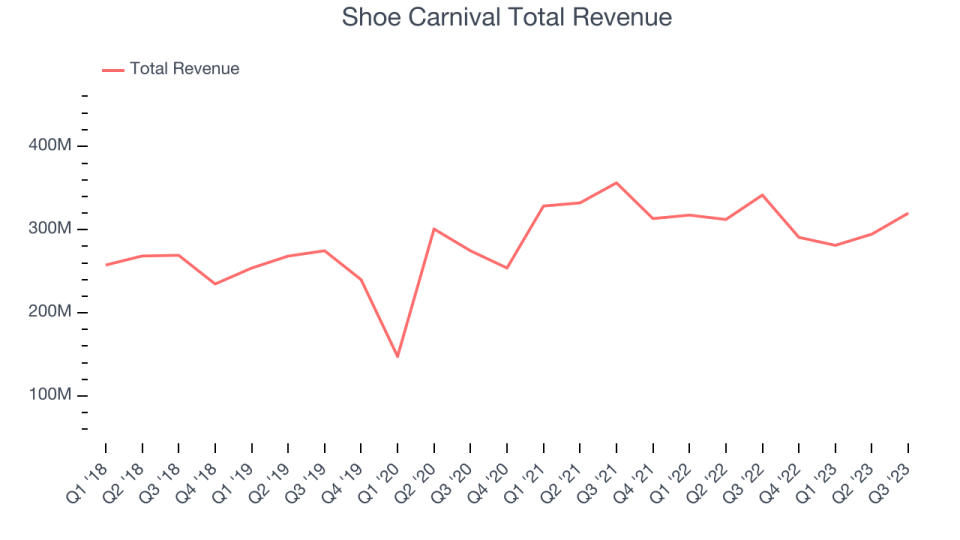

Shoe Carnival (NASDAQ:SCVL)

Known for its playful atmosphere that features carnival elements, Shoe Carnival (NASDAQ:SCVL) is a retailer that sells footwear from mainstream brands for the entire family.

Shoe Carnival reported revenues of $319.9 million, down 6.4% year on year, falling short of analyst expectations by 0.4%. It was a weak quarter for the company, with underwhelming earnings guidance for the full year and a miss of analysts' earnings estimates.

Shoe Carnival pulled off the biggest analyst estimates beat and highest full-year guidance raise among its peers. The stock is up 14.8% since the results and currently trades at $27.77.

Is now the time to buy Shoe Carnival? Access our full analysis of the earnings results here, it's free.

Weakest Q3: Designer Brands (NYSE:DBI)

Founded in 1969 as a shoe importer and distributor, Designer Brands (NYSE:DBI) is an American discount retailer focused on footwear and accessories.

Designer Brands reported revenues of $786.3 million, down 9.1% year on year, falling short of analyst expectations by 4.4%. It was a weak quarter for the company, with underwhelming earnings guidance for the full year. Its revenue missed Wall Street's estimates, driven by a huge same-store sales decrease which greatly underperformed expectations.

Designer Brands had the weakest performance against analyst estimates and slowest revenue growth in the group. The stock is down 29.9% since the results and currently trades at $8.98.

Read our full analysis of Designer Brands's results here.

Genesco (NYSE:GCO)

Spanning a broad range of styles, brands, and prices, Genesco (NYSE:GCO) sells footwear, apparel, and accessories through multiple brands and banners.

Genesco reported revenues of $579.3 million, down 4.1% year on year, falling short of analyst expectations by 1.6%. It was a weak quarter for the company, with a miss of analysts' Same-store sales, revenue, and EPS estimates.

The stock is down 20.4% since the results and currently trades at $29.77.

Read our full, actionable report on Genesco here, it's free.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned