Quanta (PWR) Q3 Earnings Beat Estimates, Margin Up, Stock Rises

Quanta Services Inc. PWR reported better-than-expected results for third-quarter 2023, wherein adjusted earnings and revenues surpassed the Zacks Consensus Estimate. Both metrics were up on a year-over-year basis.

The company continues to experience high demand for its infrastructure solutions that support energy transition initiatives and increase reliability, safety and efficiency. Project activity associated with renewable generation has been going strong and is expected to continue throughout the year.

Backed by solid performance and a strengthening outlook, particularly from the Electric Power Infrastructure Solutions and Renewable Energy Infrastructure Solutions segments, the company raised its full-year guidance for revenues.

However, shares of this leading national provider of specialty contracting services gained 3% following the release on Nov 2.

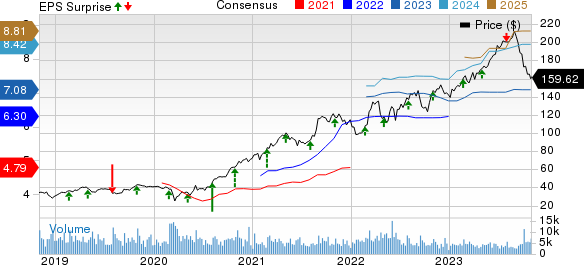

Quanta Services, Inc. Price, Consensus and EPS Surprise

Quanta Services, Inc. price-consensus-eps-surprise-chart | Quanta Services, Inc. Quote

Detailed Discussion

Quanta’s adjusted earnings per share (EPS) of $2.24 beat the consensus estimate of $2.14 by 4.7% and increased 26.6% from the year-ago quarter’s $1.77. The upside was backed by strong demand for its services driven by the customers’ multi-year programs designed to modernize and harden utility infrastructure, increase renewable generation and transmission infrastructure and move toward a reduced-carbon economy.

Total revenues of $5.62 billion surpassed the consensus mark of $5.26 billion by 6.9% and increased 26% year over year.

The operating margin for the quarter expanded 70 basis points (bps) to 7.1% from a year ago. Adjusted EBITDA of $592.5 million improved 26.8% from the year-ago quarter. We projected operating margins to be 7.2% and adjusted EBITDA to be up 21.4%.

The company reported a 12-month backlog of $17.02 billion and a total backlog of $30.1 billion at September 2023-end. This compares favorably with the December 2022-end’s 12-month backlog of $13.79 billion and the total backlog of $24.09 billion. The reported metrics were also up from the year-ago respective figures of $12.43 billion and $20.87 billion. Our model suggested a total backlog of $24.12 billion.

Segment Details

The company reports results under three segments: Electric Power Infrastructure Solutions, Renewable Energy Infrastructure Solutions and Underground Utility and Infrastructure Solutions.

Revenues from Electric Power Infrastructure Solutions totaled $2.49 billion, increasing 9.1% year over year. The upside was primarily backed by growth in spending by utility customers on grid modernization and hardening, as well as revenue growth from acquired businesses.

The operating margin expanded 70 bps to 11.9%. The segment’s 12-month backlog was $8 billion, up from $7.19 billion a year ago. The total backlog of $15.42 billion grew from $12.98 billion reported in the prior-year quarter.

Revenues from Renewable Energy Infrastructure Solutions totaled $1.75 million, up 78.5% year over year. This was driven by increased renewable infrastructure project activity and its customers' ability to move forward with construction activities in the current favorable regulatory environment and through acquisitions.

Operating margins, however, contracted 40 bps to 8.7% from a year ago due to increased costs related to higher levels of resources required to support the expected increase in project activity.

The segment’s 12-month backlog was $5.82 billion, up from $2.38 billion a year ago. The total backlog of $7.92 billion increased from $3.03 billion reported in the year-ago period.

Within the Underground Utility and Infrastructure Solutions segment, revenues rose 15.5% from the prior-year quarter’s levels to $1.38 billion, backed by higher demand from gas utility and industrial customers as well as large pipeline projects in Canada.

The operating margin of 8.9% was up 40 bps from the prior-year quarter. Segment’s 12-month backlog totaled $3.2 billion, up from $2.86 billion a year ago. The total backlog increased to $6.76 billion from $4.86 billion in the prior-year quarter.

Liquidity

As of Sep 30, 2023, Quanta had cash and cash equivalents of $305.4 million, down from $428.5 million at 2022-end. The company’s long-term debt (net of current maturities) amounted to $3.94 billion, up from $3.69 billion as of Dec 31, 2022.

Net cash provided by operating activities was $406.6 million in the third quarter, up from $343.4 million a year ago. The free cash flow for the quarter was $279.8 million versus $255.6 million reported in the year-ago period.

2023 Guidance Lifted

Quanta now expects revenues between $20.1 billion and $20.4 billion versus prior expectations of $19.6 billion and $20 billion.

The company now expects adjusted (non-GAAP) EPS in the range of $7.00-$7.20, compared with the previous projection of $6.90-$7.30. Adjusted EBITDA is now projected to be between $1.91 and $1.95 billion compared with $1.88-$1.97 billion expected earlier.

Quanta’s non-GAAP free cash flow projection is still expected to be $800-$1.00 billion. The company continues to expect net cash attributable to operating activities in the $1.20-$1.40 billion range.

Zacks Rank & Recent Construction Releases

Quanta currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Vulcan Materials Company VMC reported stellar results for the third quarter of 2023, surpassing the Zacks Consensus Estimate for both earnings and revenues.

VMC’s adjusted EPS of $2.29 increased 28.7% from the year-ago level of $1.78. Total revenues of $2,185.8 million increased 4.7% year over year.

Otis Worldwide Corporation OTIS reported impressive results in third-quarter 2023. Its earnings and net sales surpassed the Zacks Consensus Estimate and rose on a year-over-year basis. Its quarterly results reflected 12 consecutive quarters of organic sales growth and solid operating margin expansion, contributing to high-teens adjusted EPS growth.

OTIS reported quarterly EPS of 95 cents, increasing 18.8% from the year-ago quarter’s figure of 80 cents. Net sales of $3.52 billion rose 5.4% on a year-over-year basis.

United Rentals, Inc.’s URI third-quarter 2023 earnings and revenues surpassed the Zacks Consensus Estimate. On a year-over-year basis, earnings and revenues increased courtesy of sustained growth across the business, profitability and returns, underpinned by broad-based activity.

URI’s adjusted EPS of $11.73 increased 26.5% from the prior-year figure of $9.27. Total revenues of $3.77 billion grew 23.4% year over year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR) : Free Stock Analysis Report

Vulcan Materials Company (VMC) : Free Stock Analysis Report

United Rentals, Inc. (URI) : Free Stock Analysis Report

Otis Worldwide Corporation (OTIS) : Free Stock Analysis Report