Rapid7 (NASDAQ:RPD) Surprises With Q4 Sales But Full-Year Guidance Underwhelms

Cybersecurity software maker Rapid7 (NASDAQ:RPD) reported Q4 FY2023 results topping analysts' expectations , with revenue up 11.3% year on year to $205.3 million. The company expects next quarter's revenue to be around $204 million, in line with analysts' estimates. It made a non-GAAP profit of $0.72 per share, improving from its profit of $0.35 per share in the same quarter last year.

Is now the time to buy Rapid7? Find out by accessing our full research report, it's free.

Rapid7 (RPD) Q4 FY2023 Highlights:

Revenue: $205.3 million vs analyst estimates of $201.4 million (1.9% beat)

EPS (non-GAAP): $0.72 vs analyst estimates of $0.48 (51.6% beat)

Revenue Guidance for Q1 2024 is $204 million at the midpoint, roughly in line with what analysts were expecting

Management's revenue guidance for the upcoming financial year 2024 is $852 million at the midpoint, missing analyst estimates by 2.2% and implying 9.6% growth (vs 13.6% in FY2023)

Free Cash Flow of $60.25 million is up from -$582,000 in the previous quarter

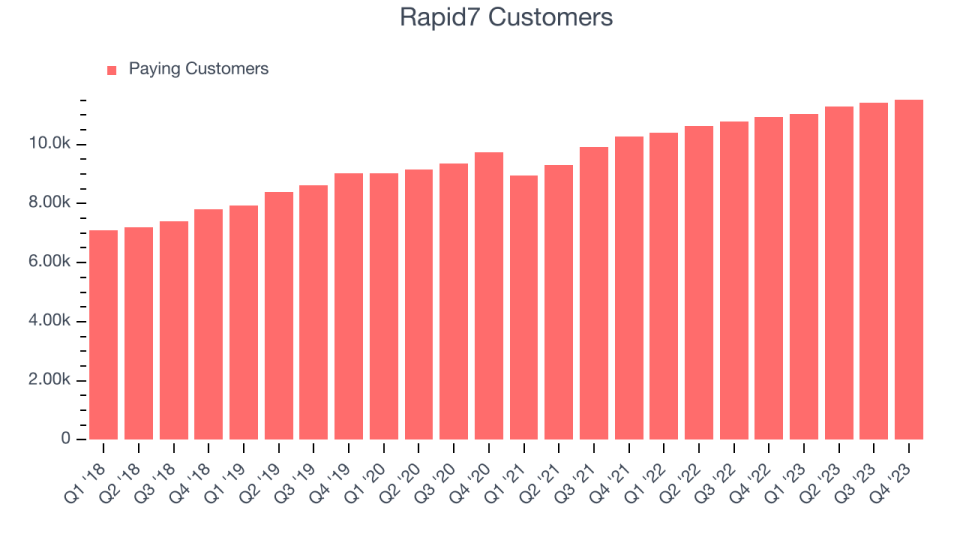

Customers: 11,526, up from 11,412 in the previous quarter

Gross Margin (GAAP): 70.9%, in line with the same quarter last year

Market Capitalization: $3.51 billion

“Rapid7 delivered solid results to end the year, exceeding our guided ranges on ARR, revenue, non-GAAP operating income, and free cash flow. Mainstream enterprise customers continue to choose Rapid7 for the strength of our consolidated security operations platform, our integrated expertise, and our compelling value proposition,” said Corey Thomas, Chairman and CEO of Rapid7.

Founded in 2000 with the idea that network security comes before endpoint security, Rapid7 (NASDAQ:RPD) provides software as a service that helps companies understand where they are exposed to cyber security risks, quickly detect breaches and respond to them.

Vulnerability Management

The demand for cybersecurity is growing as more and more businesses are moving their data and processes into the cloud, which along with a major increase in employees working remotely, has increased their exposure to attacks and malware. Additionally, the growing array of corporate IT systems, applications and internet connected devices has increased the complexity of network security, all of which has substantially increased the demand for software meant to protect data breaches.

Sales Growth

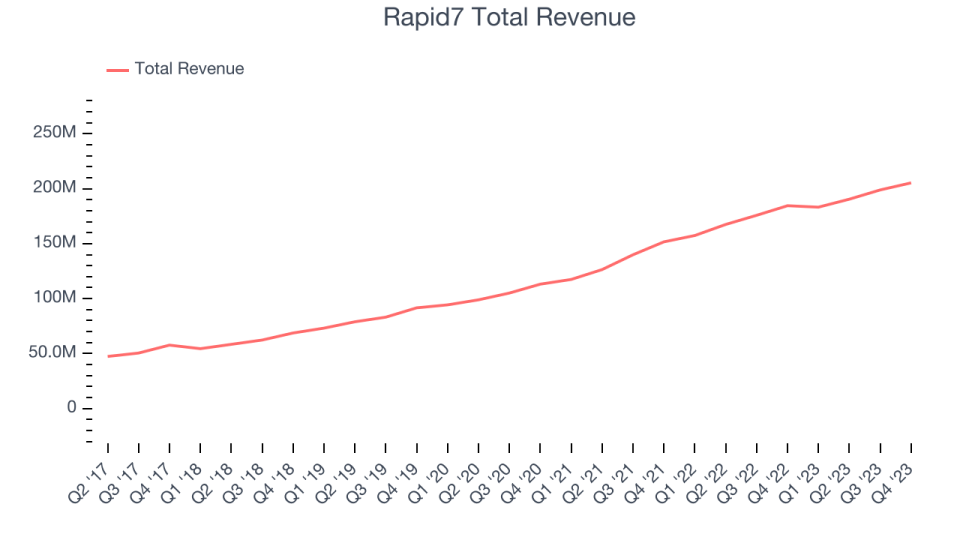

As you can see below, Rapid7's revenue growth has been strong over the last two years, growing from $151.6 million in Q4 FY2021 to $205.3 million this quarter.

This quarter, Rapid7's quarterly revenue was once again up 11.3% year on year. However, its growth did slow down compared to last quarter as the company's revenue increased by just $6.43 million in Q4 compared to $8.42 million in Q3 2023. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter's guidance suggests that Rapid7 is expecting revenue to grow 11.4% year on year to $204 million, slowing down from the 16.4% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $852 million at the midpoint, growing 9.6% year on year compared to the 13.5% increase in FY2023.

It’s not often you find a high-quality company at a significant discount to its historical P/E multiple, but that’s exactly what we found. Click here for your FREE report on this attractive Network Effect stock at a very silly price.

Customer Growth

Rapid7 reported 11,526 customers at the end of the quarter, an increase of 114 from the previous quarter. That's in line with the customer growth we observed last quarter but a bit below what we've typically seen over the last year, suggesting that sales momentum may be slowing a little. Rapid7 updated its customer count methodology in Q1 2021, which is the reason for the related drop in the number of customers.

Key Takeaways from Rapid7's Q4 Results

It was encouraging to see Rapid7 top analysts' revenue expectations this quarter, even if just narrowly. Strong free cash flow was also a good sign. That stood out as a positive in these results. On the other hand, its full-year revenue guidance was below expectations and suggests a slowdown in demand. The company is down 2.6% on the results and currently trades at $55.5 per share.

Rapid7 may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.