Reasons to Add CurtissWright (CW) to Your Portfolio Right Now

CurtissWright Corp. CW, with its multi-domain precision components, is well-positioned to benefit from the rising demand for nuclear power. The company’s strong international presence, stable financial position and increasing demand due to global tension will boost its performance.

Let’s explore the factors that make this Zacks Rank #2 (Buy) company a strong investment pick at the moment.

Growth Projections & Surprise History

The Zacks Consensus Estimate for CW’s 2023 earnings per share (“EPS”) is pegged at $9.08, up 0.11% in the past 60 days.

The consensus estimate for 2023 sales is pinned at $2.77 billion, indicating a year-over-year improvement of 8.3%.

The stock delivered an average earnings surprise of 4.08% in the last four quarters.

Debt Position

The total debt-to-capital of CW is 35.48%, better than 50.94% registered by the industry. This indicates that the company has less debt than its peers, which is a positive.

CW has a current ratio of 2.11, better than the industry’s average of 1.52. This implies that the company has sufficient financial capability to pay its short-term debt obligations.

Increasing Nuclear Power Adoption & Rising Demand

The pro-nuclear sentiment and need for energy independence worldwide will support Curtiss-Wright’s long-term growth opportunities in the nuclear market. According to the Nuclear Regulatory Commission, nuclear power comprises approximately 20% of all electric power produced in the United States.

The United States, with 92 reactors across 54 nuclear power plants in 28 states, has solid growth opportunities for CW’s vast portfolio of advanced nuclear technologies.

In the second quarter, CurtissWright received orders totaling $842 million. The 8% increase was due to the strong demand for defense electronics, naval defense products and nuclear aftermarket products. The increased fiscal 2024 budget allocation for America’s sea power will further drive strong demand for CW’s nuclear propulsion equipment.

Return on Equity

Return on Equity (“ROE”) indicates how efficiently a company has been utilizing its funds to generate higher returns. Currently, CurtissWright’s ROE is 16.6%, higher than the industry average of 11.2%. This indicates that the company has been utilizing its funds more constructively than its aerospace defense equipment industry peers.

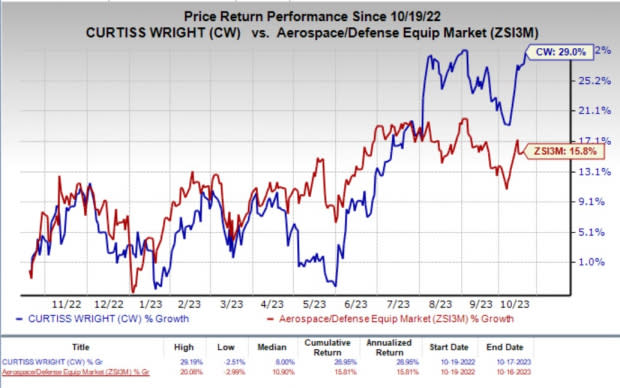

Price Performance

In the past year, shares of CW have rallied 29% compared with the broader industry’s 15.8% growth.

Image Source: Zacks Investment Research

Other Stocks to Consider

A few other top-ranked stocks from the same industry are BAE Systems PLC BAESY, TransDigm Group Inc. TDG and AAR Corp. AIR. BAE Systems sports a Zacks Rank #1 (Strong Buy), and TransDigm and AAR each carry a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

BAESY boasts a long-term earnings growth rate of 14%. The Zacks Consensus Estimate for 2023 sales indicates year-over-year growth of 33.6%.

TDG boasts a long-term earnings growth rate of 25.6%. The Zacks Consensus Estimate for 2023 sales indicates year-over-year growth of 21.1%.

The Zacks Consensus Estimate mark for AIR’s 2023 sales indicates a year-over-year increase of 14.2%. It delivered an average earnings surprise of 6.23% in the past four quarters.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AAR Corp. (AIR) : Free Stock Analysis Report

Transdigm Group Incorporated (TDG) : Free Stock Analysis Report

Bae Systems PLC (BAESY) : Free Stock Analysis Report

Curtiss-Wright Corporation (CW) : Free Stock Analysis Report