Reasons to Add Manitowoc (MTW) Stock to Your Portfolio

The Manitowoc Company MTW has been delivering improved results in the past few quarters, benefiting from improving demand. Its pricing actions also helped negate the impact of higher costs and supply-chain headwinds. The company continues to accelerate its investment in product development and innovation, strengthening its aftermarket business, which will drive growth. Increased spending on infrastructure in the United States is also expected to be a major catalyst.

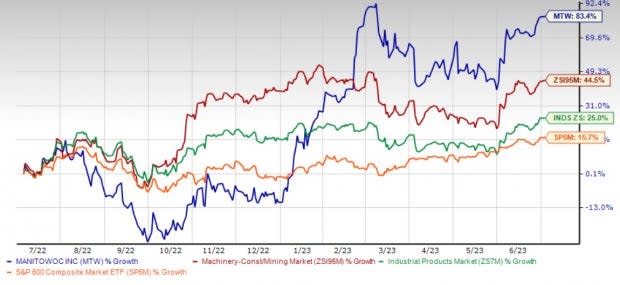

Top Zacks Rank & Upbeat Price Performance

MTW currently sports a Zacks Rank #1 (Strong Buy).

Shares of the company have soared 83.4% in a year’s time compared with the industry’s 44.5% growth. The Zacks Industrial Products sector has gained 25% and the S&P 500 composite has risen 15.7% in the same time frame.

Image Source: Zacks Investment Research

Better-Than-Expected Q1 Earnings

Manitowoc’s adjusted earnings per share (EPS) for the first quarter of 2023 were 46 cents which marked a substantial improvement from the EPS of three cents reported in the year-ago quarter. The company also beat the Zacks Consensus Estimate of five cents by a solid margin of 820%. MTW has an impressive trailing four-quarter earnings surprise of 256.3%, on average.

Upbeat Outlook for 2023

Orders in the first quarter of 2023 increased 9% year over year to $525 million. The backlog at the end of the quarter was $1,076 million, up from $1,033 million reported in the last-year quarter. Backed by this momentum, Manitowoc expects revenues of $2-$2.1 billion for 2023. The company reported revenues of $2.03 billion in 2022. Adjusted EPS is expected between 35 cents and $1.15, compared with $1.06 in 2022.

The Zacks Consensus Estimate for the company’s 2023 revenues is at $2.09 billion, which suggests year-over-year growth of 3%. The same for EPS is at $1.12, indicating 5.7% year-over-year growth.

Estimates Northbound

The Zacks Consensus Estimate for MTW’s earnings for 2023 has moved up 11% over the past 60 days. The consensus mark for 2024 earnings has also seen a northward revision of 10% to $1.35 per share.

Demand Prospects Look Solid

In North America, demand from residential and non-residential construction is driving demand for Manitowoc’s equipment. Due to the U.S. Infrastructure Investment and Jobs Act, the rising investment in roads, bridges, airports and waterways represents a massive opportunity. The company expects demand in the Middle East to be robust in the upcoming quarters. Qatar and Kuwait are also showing signs of growth. This bodes well for Manitowoc. Further, the need to replace the aging crane fleet will support the demand for Manitowoc’s equipment.

Efforts to Grow Aftermarket Sales to Aid Growth

To achieve sustainable growth in both sales and earnings, Manitowoc is now placing greater emphasis on growing non-new machine sales (aftermarket parts, services, rentals, used cranes, and digital solutions). Growing this part of the business will provide it with more annuity-like revenue streams that will help lessen the impact of the crane market cyclicality. This business also carries higher margin rates than new crane sales. Non-new machine revenues were $567 million in the trailing twelve months ended Mar 31, 2023 and Manitowoc further aims to take up this figure to $675 million by 2026.

Investing in Acquisitions, Product Innovation

As of Mar 31, 2023, Manitowoc had a total liquidity of $296 million. The company’s total debt-to-total capital ratio was at 0.41 as of Mar 31, 2023. The total debt-to-total capital ratio has gone down considerably over the years from 0.62 as of 2015. The company remains focused on cash preservation and balance sheet management while funding critical programs for growth.

MTW continues to evaluate acquisition opportunities to accelerate product development programs in its all-terrain product line. Manitowoc’s innovation pipeline remains robust. Focus on innovation will continue to aid it in leading the industry by providing differentiated products that add value to customers.

Other Stocks to Consider

Some other top-ranked stocks in the Industrial Products sector are W.W. Grainger, Inc., GWW, Allegion ALLE and AptarGroup ATR. Each of these stocks carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Grainger’s 2023 EPS is pegged at $35.86, which projects 21% growth from the year-ago reported figure. The estimate has moved up 2% in the past 60 days.

GWW has a trailing four-quarter average earnings surprise of 9.1%. The company’s shares have gained 66% in the last year.

Allegion has an average trailing four-quarter earnings surprise of 12.5%. The Zacks Consensus Estimate for Allegion’s fiscal 2023 earnings has moved up 1% in the past 60 days to $6.63 per share. The consensus mark suggests year-over-year growth of 16.5%.

ALLE has an average trailing four-quarter earnings surprise of 12.5%. Its shares have gained 18% in the past year.

The consensus estimate for AptarGroup’s 2023 EPS is currently at $4.16. The estimate has moved up 3% in the past 60 days. The estimate projects year-over-year growth of 9.8%. ATR has a trailing four-quarter average earnings surprise of 6.4%. AptarGroup’s shares have gained 14% in a year’s time.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Manitowoc Company, Inc. (MTW) : Free Stock Analysis Report

W.W. Grainger, Inc. (GWW) : Free Stock Analysis Report

AptarGroup, Inc. (ATR) : Free Stock Analysis Report

Allegion PLC (ALLE) : Free Stock Analysis Report