Reasons to Add Veeva Systems (VEEV) Stock to Your Portfolio

Veeva Systems Inc. VEEV has been gaining from its strong product portfolio. The optimism led by a solid first-quarter fiscal 2024 performance and strong product adoption are expected to contribute further. Stiff competition and forex volatility persist.

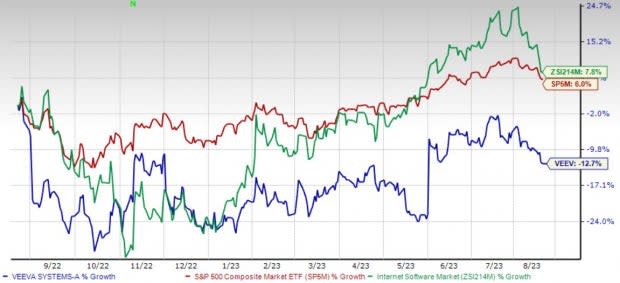

Over the past year, this Zacks Rank #2 (Buy) stock has lost 12.7% against 7.9% growth of the industry and a 6% rise of the S&P 500 composite.

The renowned provider of cloud-based software applications and data solutions for the life sciences industry has a market capitalization of $29.96 billion. The company projects 20.3% growth for the next five years and expects to maintain its strong performance. It has delivered an earnings surprise of 8.3% for the past four quarters, on average.

Image Source: Zacks Investment Research

Let’s delve deeper.

Strong Product Portfolio: We are optimistic about Veeva Systems’ unique solutions, which include Veeva Vault, Veeva CRM (customer relationship management), Veeva Network and Veeva OpenData. In June, the company announced the expansion of its business consulting services to help life sciences organizations achieve greater speed and efficiency across the product development lifecycle.

In May, Veeva Systems announced the availability of Veeva Link MedTech.

Product Adoption: We are upbeat about Veeva Systems registering a robust adoption for its products over the past few months. In July, the company announced that Merck KGaA, Darmstadt, Germany, is using Veeva Vault MedInquiry as its global medical information management system.

In May, Veeva Systems announced that Lotus Clinical Research expanded its partnership with Veeva Systems and broadened its adoption of Veeva Vault Clinical Suite to strengthen its service delivery and efficiency.

Strong Q1 Results: Veeva Systems’ solid first-quarter fiscal 2024 results buoy optimism. The company saw an uptick in the overall top line and robust performances by both segments. The company continued to benefit from its flagship Vault platform. Veeva Systems’ continued strength in its Commercial Solutions, with new small-sized to mid-sized customer additions and expansions in Veeva Commercial Cloud, were also seen.

Downsides

Forex Volatility: Veeva Systems derives a major share of its revenues from international operations. Some of its international agreements provide payment denominated in local currencies and the majority of its local costs are also denominated in local currencies. Fluctuations in the value of the U.S. dollar versus foreign currencies may impact its operating results when converted into U.S. dollars.

Stiff Competition: Veeva Systems operates in a highly competitive market. In new sales cycles within the company’s largest product categories, it competes with other cloud-based solutions from providers that make applications for the life sciences industry. The company’s Commercial Cloud and Veeva Vault application suites also compete to replace client-server-based legacy solutions offered by large companies and other smaller application providers.

Estimate Trend

Veeva Systems is witnessing a positive estimate revision trend for fiscal 2024. In the past 90 days, the Zacks Consensus Estimate for its earnings has moved 5.8% north to $4.57.

The Zacks Consensus Estimate for the company’s second-quarter fiscal 2024 revenues is pegged at $581.8 million, suggesting an 8.9% improvement from the year-ago quarter’s reported number.

Other Key Picks

A few other top-ranked stocks in the broader medical space are Patterson Companies, Inc. PDCO, HealthEquity, Inc. HQY and McKesson Corporation MCK.

Patterson Companies, sporting a Zacks Rank #1 (Strong Buy) at present, has an estimated long-term growth rate of 9.2%. PDCO’s earnings surpassed estimates in three of the trailing four quarters and missed once, with an average surprise of 4.5%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Patterson Companies has gained 17.1% compared with the industry’s 11% rise over the past year.

HealthEquity, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 22%. HQY’s earnings surpassed estimates in three of the trailing four quarters and missed once, with an average of 9.1%.

HealthEquity has gained 8.8% against the industry’s 15.7% decline over the past year.

McKesson, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 10.7%. MCK’s earnings surpassed estimates in three of the trailing four quarters and missed once, the average surprise being 8.1%.

McKesson has gained 14.2% compared with the industry’s 11% rise over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

McKesson Corporation (MCK) : Free Stock Analysis Report

Patterson Companies, Inc. (PDCO) : Free Stock Analysis Report

Veeva Systems Inc. (VEEV) : Free Stock Analysis Report

HealthEquity, Inc. (HQY) : Free Stock Analysis Report