Reasons to Retain Waste Management (WM) in Your Portfolio

Waste Management, Inc. WM is currently benefiting from its core operating performance, steady shareholder-friendly measures and solid liquidity.

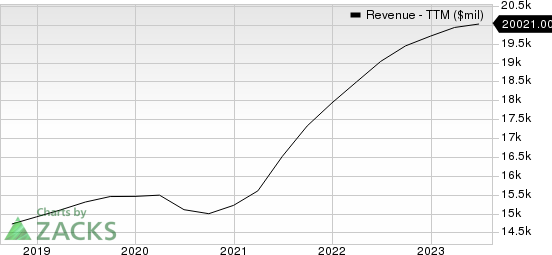

The company’s earnings and revenues for 2023 are expected to grow 6.6% and 3.9%, respectively. WM has a long-term (three to five years) expected earnings growth rate of 9.9%.

Factors Favoring WM

Being a leading provider of comprehensive waste management environmental services, WM is expected to continue benefiting from ongoing trends like increasing environmental concerns, rapid industrialization, increase in population and active government measures to reduce illegal dumping. The company’s top line increased 2% year over year in the second quarter of 2023.

Waste Management, Inc. Revenue (TTM)

Waste Management, Inc. revenue-ttm | Waste Management, Inc. Quote

Waste Management continues to execute core operating initiatives, targeting focused differentiation and continuous improvement and instilling price and cost discipline to achieve better margins. While differentiation through capitalization of extensive assets ensures long-term profitable growth and competitive advantages, cost control, process improvement and enhancements to its digital platform help enhance service quality.

The company has a steady dividend, as well as a share repurchase policy. In 2022, 2021 and 2020, it repurchased shares worth $1.5 billion, $1.4 billion and $402 million, respectively. It paid $1.1 billion, $970 million and $927 million in dividends in 2022, 2021 and 2020, respectively. WM plans to return significant cash to shareholders through healthy dividends and share repurchases in the future as well.

A Risk

WM's current ratio at the end of the second quarter of 2023 was pegged at 0.82, lower than the prior quarter’s 0.87 and the prior-year quarter’s current ratio of 1.07. A decline in the current ratio does not bode well, as it indicates that the company may have problems meeting its short-term obligations.

Zacks Rank and Stocks to Consider

The company currently carries a Zacks Rank #3 (Hold).

Investors interested in the broader Zacks Business Services sector can consider stocks like Verisk Analytics VRSK and ICF International ICFI.

Verisk currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The company has a trailing four-quarter earnings surprise of 9.9% on average. VRSK shares have gained 7.4% in the past three months.

ICF International carries a Zacks Rank #2 and a VGM Score of A. The company has a trailing four-quarter earnings surprise of 7% on average. ICFI shares have gained 13.6% in the past three months.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Waste Management, Inc. (WM) : Free Stock Analysis Report

ICF International, Inc. (ICFI) : Free Stock Analysis Report

Verisk Analytics, Inc. (VRSK) : Free Stock Analysis Report