Reasons You’re Still Living Paycheck to Paycheck

Even if you're earning a good salary, you might still be living paycheck to paycheck. And you're not alone. According to a survey by GOBankingRates, an astonishing 34% of Americans have no savings at all, while another 69% have less than $1,000 socked away for emergencies.

Prepare Now: 23 Tips To Build Your Emergency Fund

Budgeting 101: How To Create a Budget You Can Live With

If you're tired of living paycheck to paycheck, consider taking steps to improve your financial circumstances. Here are 10 reasons your budget is broken, along with strategies to get out of debt and grow your savings.

Last updated: Sept. 15, 2021

You’re Paying the Minimum on Your Debts

When you’re budgeting for the month, it can be tempting to minimize your debt payments to free up extra cash for upcoming expenses. However, what is that money move doing to your finances in the long run? The short answer: It’s making you spend way too much on interest payments, while also harming your credit score.

If you pay the monthly minimum on your credit card purchases, you’re unlikely to pay off what you owe in a timely manner. For example, paying the minimum 2 percent on a bill of $5,000 could cost you thousands of dollars in interest and take you more than 30 years to pay off at an assumed 18.00% APR. Additionally, this move could affect the interest rates you are offered on other loans in the future -- or even prevent you from qualifying for a line of credit at all.

Attempting to improve your credit score or negotiate your interest rate down could save you money in interest payments and reduce the time it takes to pay off your debt. And paying more than the minimum balance would save you money and help you get out of debt faster -- perhaps even by a few years.

Up Next: States Most (and Least) Likely To Live Paycheck to Paycheck

You’re Busy Keeping Up With the Joneses

Your neighbor just bought a new sports car. A former college roommate put a down payment on a palatial four-bedroom home. And your coworker wears designer clothes to the office every day.

It’s easy to see others living an extravagant lifestyle and want the same luxuries for yourself. However, that doesn’t mean you should live like you’re rich before you have the money to back it up.

No matter how successful you are, and how much you have to show for it, there will always be someone out there with a newer gadget, a more tricked-out ride or a slightly bigger house. That’s life. Trying to keep up with the Joneses will only hurt your bank account later on, when you can’t make the auto loan payments for the new car you have sitting at the curb.

Instead of trying to keep up with the Joneses, learn how to live rich on a budget.

Live Within Your Means: 25 Cheapest Luxury Cars You Can Lease

You Fail To Plan For Irregular Expenses

Are you budgeting throughout the year for birthday gifts, potential car maintenance costs, biannual auto insurance bills or any other expense that doesn’t recur monthly? If you’re not planning for these irregular expenses, you’re likely digging yourself into a bigger hole than you realize.

Matt Becker, founder of fee-only financial planning practice Mom and Dad Money, said these expenses can disrupt even the most robust budget if not taken into account.

“The mistake I see all the time is failing to plan for irregular expenses,” he said. “That includes not only the bad stuff like car repairs and home maintenance, but fun things like travel and gifts. You should regularly be putting money away for these kinds of expected but irregular expenses so that when they happen, you’re not left scrambling to find the money -- and they don’t blow a hole in your budget.”

Even if it means adjusting your budget to make room for these expenses, by saving more or dedicating a portion of your savings to these costs, it’ll help you maintain your financial footing each month.

You Fail To Plan, Period

Do you have a budget to begin with? Have you calculated how much money you can allot to food, housing, transportation and personal expenses while still managing to save up a college or emergency fund? If you don't have a financial plan, you really have no way to build up your wealth or make sure you stay out of debt.

“Everything from going over budget to paying a subscription fee for the free trial you forgot to cancel is the result of a failure to plan,” said Stefanie O’Connell, freelance writer and author of "The Broke and Beautiful Life." “Whether it’s planning for retirement or planning to brown bag your lunch for work tomorrow, planning can empower you and your finances.”

It’s one thing to set up a reasonable budget, but if you have no system in place to stick to it, you’re doomed to fail. It’s important to ask yourself what your budget translates to -- $70 per month budgeted for nights out translates to seven cocktails per month at an average of $10 each, or roughly two cocktails per week. Converting dollars into items can help you keep track of what you can afford and what you simply can’t stretch your budget to accommodate.

In her book, "Say Goodbye to Survival Mode," Crystal Paine writes that a budget can be your key to a worry-free financial future.

"Here’s the beautiful thing about a budget: While it’s hard and limiting at first, over time you’ll realize that it’s your means to enjoy life without headaches and worry," she said. "Ultimately, it’s a pathway to freedom. And when you tell your money how to work for you, you can be intentional about how you use it.”

According to Kendal Perez, blogger for Hassle-Free Savings, even planning ahead for your ATM withdrawals can save you a lot of cash over time.

“Withdrawing cash all the time from ATM stations that aren’t affiliated with your bank is eating into your income,” she said. “Avoid this expense by withdrawing cash at the beginning of the month or getting extra cash at checkout when you’re out shopping.”

You Don’t Realize How Handy You Are

When appliances go on the fritz, many people call handymen to repair them. However, in today’s digital age, how-to videos and tutorials are available on nearly every topic you could imagine -- and handyman costs aren’t cheap, averaging about $390, according to HomeAdvisor.

“People mistakenly believe that all repairs require hiring a professional to do the job, or worse, that it’s easier or cheaper to buy new stuff when they break,” said Jody Lamb, a public relations pro who has worked with RepairClinic. “Today, there are expertly produced how-to websites and videos available online that make it easy for novice and inexperienced do-it-yourselfers to fix stuff on their own and extend the life of their appliances and equipment.”

So, instead of blowing your paycheck on that next repair, go the DIY route for basic services.

You Spend Impulsively

You decide to go to the mall to window shop, see something you like and immediately purchase it without looking around for a more affordable alternative, or for a discount. Granted, couponing can get extreme, and shopping around can eventually eat away at your savings if you’re spending more on gas. However, buying items on the spot can make living paycheck to paycheck inevitable.

Patience is a virtue of the wallet, as most retail companies put the items they carry on sale eventually. It might be last season’s style, but the savings could be huge if you wait on those seemingly must-have purchases. In fact, you might even realize that you don’t really need or want that item in the first place.

According to author and small-business coach Julia Kline, a wish list can help you reduce their spending and stretch your paychecks for the items you truly want.

“I often have clients who thought they couldn’t afford a new TV, but by simply curtailing their impulsive, unnecessary spending for a month, they found that they had plenty of money for the TV, after all,” she said. “And they were more than happy to sacrifice the extra tube of lipstick, the fancy sunglasses and the expensive carry-out in order to make it happen.”

You’re Still Paying For Unused Memberships

Your unused memberships to fitness centers, clubs and organizations can put a sizable dent in your monthly income. This is a potential pitfall of signing up for automatic payments, as it’s easy to lose track of where your money is going and if the amount has changed.

It’s wise to evaluate the subscriptions you have and conduct a cost-benefit analysis to determine whether you should maintain that Netflix account or gym membership. Trim the fat in terms of your subscriptions to the magazines you never read or the Amazon Prime membership you’re not using, and free up some cash to pay down debt or finance unexpected bills.

You Avoid Your Bank Account and Credit Card Statements

The worst thing you can do is deny the reality of your financial situation. Many people avoid looking at their bank accounts and credit card statements out of fear. This is a disservice, though, as you can’t tackle your financial situation or properly budget if you don’t know how you’re faring with your money.

There are additional risks associated with not checking your statements regularly. For example, you could be charged for expenses you didn't incur, letting your accounts remain compromised without your knowledge.

Reviewing your credit card statements can help you see if you’re spending more than you earn, as can reviewing your checking account balance to make sure all of your paychecks are deposited properly and that you’re remaining in the black. Checking up on your statements can also help you adjust your budget to be more realistic to your expenses.

Read: 26 Cities Where Paycheck Are Surprisingly Low

You Fail To Think Like an Investor

Rather than just budgeting for needs and wants, investors take as much money as possible and invest it in their financial futures, making the money work for them. It’s easy to let your money sit idle in a low-interest savings account -- but what would an investor do?

You’ve probably heard of the stock market, money market accounts, retirement accounts and laddered certificates of deposit, but are you actively using these products and investments to grow your wealth? Saving for the future by putting some money away in a mutual fund can create financial stability for the long term, while simultaneously helping you curb the bad money habit of viewing your income as entirely yours to use as you please.

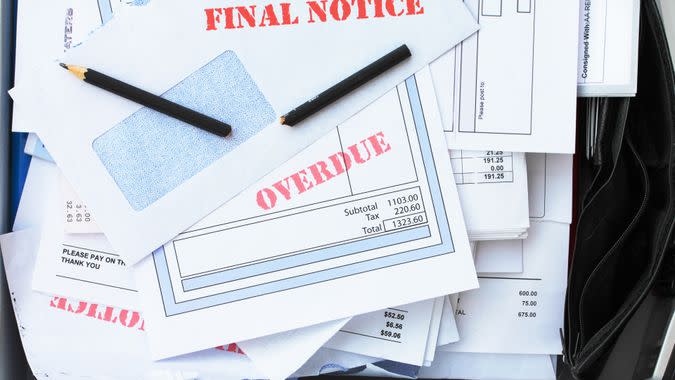

You’re Not Paying Bills on Time

According to a study by the Federal Reserve Bank of Boston, 65 percent of credit card users carry balances from month to month. So, it stands to reason that many of those individuals also neglect to pay other bills on time. Unfortunately, failing to pay bills on schedule can cost you more in the long run.

Not only does paying bills after the due date result in surcharges and fees, but it also affects your credit over the long term. So, you could end up with a higher interest rate on future loans. That means you'll be shelling out more for that car loan or mortgage payment.

For best results, avoid the impulse to hide bills at the bottom of the mail stack. You can also set up automatic payments when possible, so the money comes out of your account well before it's due.

More From GOBankingRates

What Money Topics Do You Want Covered: Ask the Financially Savvy Female

Nominate Your Favorite Small Business To Be Featured on GOBankingRates

This article originally appeared on GOBankingRates.com: Reasons You’re Still Living Paycheck to Paycheck