Reasons Why Investors Should Retain Automatic Data (ADP) Stock

Automatic Data Processing, Inc. ADP has an impressive earning surprise history, beating the Zacks Consensus Estimate of earnings in all four trailing quarters with an average surprise of 2.6%.

ADP holds a dominant position in the Human Capital Management (HCM) market which is further strengthened by strategic acquisitions. However, rising expenses have pressured the company’s bottom line.

Factors in Favour

Automatic Data’s three-tier business strategy helps it to maintain and grow as an HCM service provider. The company has been growing on the back of innovative and mission-critical HCM solutions that include a complete suite of cloud-based HCM and HR Outsourcing solutions.

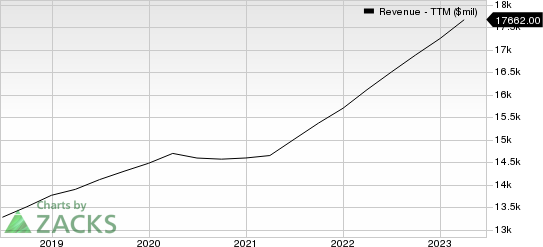

Automatic Data Processing, Inc. Revenue (TTM)

Automatic Data Processing, Inc. revenue-ttm | Automatic Data Processing, Inc. Quote

The company is reaping the benefits of its highly recurring business model which allows it to earn good margins and lowers its capital expenditure. The cash-generating ability acts as a growth catalyst. The demand environment is boding well for the company, with robust new business and solid performance in employer service.

The company has been active on the acquisition front strengthening its customer base and expanding its presence in the international market. Acquisitions like Celergo, WorkMarket, Global Cash Card and The Marcus Buckingham Company are indicators of the same.

Some Risks

ABM Industries is having high expenses on the back of continuous investments in transformational initiatives and year-over-year increases in acquisitions. In fiscal 2022, ADP’s total expenses of $12.8 billion increased 10% year over year. Total expenses increased 2% year over year in 2021, 3% year over year in fiscal 2020.

During the last twelve months, ADP has plunged 7.9%, compared with its industry’s 2% decline.

Zacks Rank and Stocks to Consider

ADP currently carries a Zacks Rank #3 (Hold).

Investors interested in the broader Zacks Business Services can consider the following stocks

Green Dot GDOT: For second-quarter 2023, the Zacks Consensus Estimate of Green Dot’s revenues suggests a decline of 4.5% year over year to $339.2 million and the same for earnings indicates a 59.5% plunge to 30 cents per share. The company has an impressive earning surprise history, beating the consensus mark in all four trailing quarters, the average surprise being 37.3%.

GDOT has a Value score of A and currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 (Strong Buy) Rank stocks here.

Maximus MMS: For second-quarter 2023, the Zacks Consensus Estimate of Maximus’ revenues suggests an increase of 6.9% year over year to $1.2 billion and the same for earnings indicates a 46.2% rise to $1.14 per share. The company has an impressive earning surprise history, beating the consensus mark in three instances and missing on one instance, the average surprise being 9.6%.

MMS has a VGM score of A along with a Zacks Rank of 1.

Rollins ROL: For second-quarter 2023, the Zacks Consensus Estimate of Rollins’ revenues suggests growth of 12.6% year over year to $803.6 million and the same for earnings indicates a 15% increase to 23 cents per share. The company has an impressive earning surprise history, beating the consensus mark in three of the four trailing quarters and missing on one instance, the average surprise being 5.53%.

ROL currently carries a Zacks Rank of 2.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Automatic Data Processing, Inc. (ADP) : Free Stock Analysis Report

Green Dot Corporation (GDOT) : Free Stock Analysis Report

Rollins, Inc. (ROL) : Free Stock Analysis Report

Maximus, Inc. (MMS) : Free Stock Analysis Report