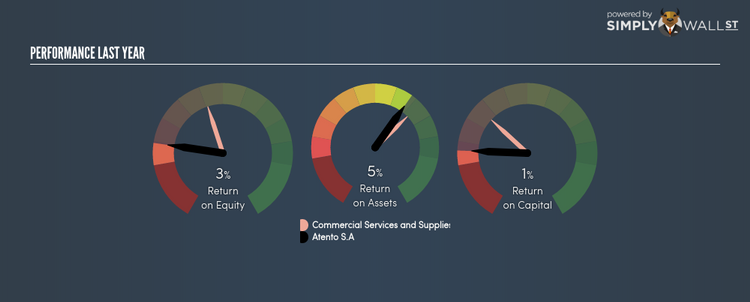

With A Recent ROE Of 2.96%, Can Atento SA (ATTO) Catch Up To Its Industry?

Atento SA (NYSE:ATTO) generated a below-average return on equity of 2.96% in the past 12 months, while its industry returned 13.12%. ATTO’s results could indicate a relatively inefficient operation to its peers, and while this may be the case, it is important to understand what ROE is made up of and how it should be interpreted. Knowing these components could change your view on ATTO’s performance. I will take you through how metrics such as financial leverage impact ROE which may affect the overall sustainability of ATTO’s returns. Check out our latest analysis for Atento S.A

Peeling the layers of ROE – trisecting a company’s profitability

Firstly, Return on Equity, or ROE, is simply the percentage of last years’ earning against the book value of shareholders’ equity. An ROE of 2.96% implies $0.03 returned on every $1 invested. Generally speaking, a higher ROE is preferred; however, there are other factors we must also consider before making any conclusions.

Return on Equity = Net Profit ÷ Shareholders Equity

Returns are usually compared to costs to measure the efficiency of capital. ATTO’s cost of equity is 9.55%. Given a discrepancy of -6.59% between return and cost, this indicated that ATTO may be paying more for its capital than what it’s generating in return. ROE can be split up into three useful ratios: net profit margin, asset turnover, and financial leverage. This is called the Dupont Formula:

Dupont Formula

ROE = profit margin × asset turnover × financial leverage

ROE = (annual net profit ÷ sales) × (sales ÷ assets) × (assets ÷ shareholders’ equity)

ROE = annual net profit ÷ shareholders’ equity

The first component is profit margin, which measures how much of sales is retained after the company pays for all its expenses. Asset turnover reveals how much revenue can be generated from ATTO’s asset base. And finally, financial leverage is simply how much of assets are funded by equity, which exhibits how sustainable ATTO’s capital structure is. Since financial leverage can artificially inflate ROE, we need to look at how much debt ATTO currently has. At 123.86%, ATTO’s debt-to-equity ratio appears balanced and indicates its ROE is generated from its capacity to increase profit without a large debt burden.

What this means for you:

Are you a shareholder? ATTO’s below-industry ROE is disappointing, furthermore, its returns were not even high enough to cover its own cost of equity. Since its existing ROE is not fuelled by unsustainable debt, investors shouldn’t give up as ATTO still has capacity to improve shareholder returns by borrowing to invest in new projects in the future. If you’re looking for new ideas for high-returning stocks, you should take a look at our free platform to see the list of stocks with Return on Equity over 20%.

Are you a potential investor? If you are considering investing in ATTO, looking at ROE on its own is not enough to make a well-informed decision. I recommend you do additional fundamental analysis by looking through our most recent infographic report on Atento S.A to help you make a more informed investment decision.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.